The Medicare Mail and TV Ad Blitz: What Agents Tell Seniors to Throw Out, Hang Up On, and Actually Trust

-

June 25, 2026

If you're turning 65 or already on Medicare, you've probably noticed: your mailbox is stuffed, your phone won't stop ringing, and every commercial break features someone promising you a grocery card, free dental, or money back in your Social Security check. You're not imagining it, and you're not alone. It's one of the most common complaints agents on Medicare Agents Hub hear from the people they work with.

Fact-check note: Medicare marketing rules change over time. This article was reviewed against Medicare.gov and current CMS Medicare Advantage and Part D marketing regulations, including rules on unsolicited contact, Scope of Appointment, plan marketing materials, and required plan documents.

Why Your Mailbox Exploded (and Who's Behind It)

The moment you approach 65, your name lands on eligibility lists that insurance companies, agencies, and marketing organizations use to target you. Agents describe it the same way their clients do: overwhelming, confusing, and nonstop.

But not all of that mail is junk, and not all of it is legitimate. The first step is learning to tell the difference.

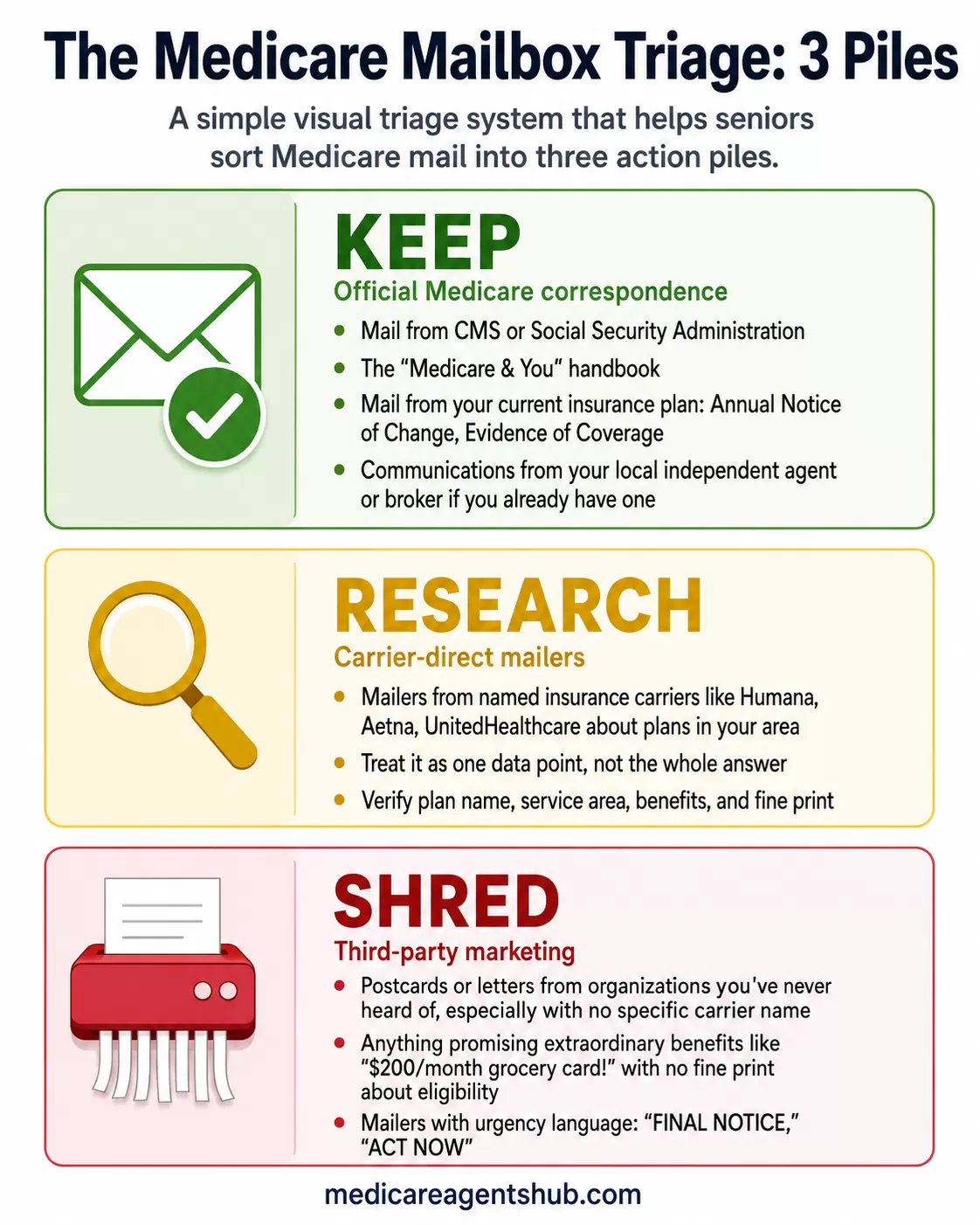

The Three Piles: Keep, Research, Shred

Keep (official Medicare correspondence):

- Anything from the Centers for Medicare & Medicaid Services (CMS) or the Social Security Administration

- Your "Medicare & You" handbook

- Mail from your current insurance plan (Annual Notice of Change, Evidence of Coverage)

- Communications from your local independent agent or broker if you already have one

Research (carrier-direct mailers):

- Mailers from named insurance carriers (Humana, Aetna, UnitedHealthcare, etc.) about plans in your area

- Mailers from named Medicare Advantage or Part D organizations are more likely to be regulated plan marketing materials, but you should still verify the plan name, service area, benefits, and fine print before relying on them. They also only show you that carrier's plans, not the full picture

- Treat these as one data point, not the whole answer

Shred (third-party marketing):

- Postcards or letters from organizations you've never heard of, especially those with no specific carrier name

- Anything promising extraordinary benefits ("$200/month grocery card!") with no fine print about eligibility

- Mailers with urgency language ("FINAL NOTICE," "ACT NOW") designed to make you panic

I'm turning 65 next month and the amount of Medicare mail I'm getting is overwhelming. How do I sort through all this?

Most of the information is an attempt to entice you to make a call by promising a lot of $0 costs to you for a lot of different benefits.It's true that there are a lot of $0 cost benefits available, but not all on one plan. Every plan has a certain amount of benefits for $0 cost depending on each plan's own actuarial analysis of costs.

Generally, more $0 or low cost benefits are more available to folks who qualify, because of lower incomes, for extra help or who qualify for Medicaid.

(Medicaid is what we used to refer to as "welfare".)

To sort through the information, look for advertisements which talk about finding the right plan for your specific situation, not the plans promising a lot of $0.

Look for someone more interested in answering your questions, helping you feel comfortable, making sure you can keep your doctor and get the care you need.

Look for someone who will work for you at your speed, not someone pushing you to buy.

It's you who is important, not me.

The Celebrity TV Commercial Problem

Joe Namath. William Shatner. Jimmie Walker. If you've watched television between October and December, you've seen celebrities telling you that you're missing out on Medicare benefits. Agents have strong feelings about these commercials, and most of those feelings aren't positive.

The core issue agents raise is not that celebrities appear in the ads. It's what the ads leave out. Benefits advertised on national television vary by state, county, and even ZIP code. A plan offering a $200 monthly food allowance in one county may not exist at all in yours. The commercials almost never make that clear.

Don't you think Medicare should ban all those celebrity Medicare Advantage commercials?

My concern isn't with "Who" they bring in to assist with the advertising, but the lack of full disclosure they present in those commercials.The MA commercials are always pressing on the "free" items, and the benefits they tell you they can give you, but aren't disclosing that by taking those plans, you have boxed yourself into their Network, which will not have the highest quality doctor, specialists, or hospitals, based upon the amount and the payment time from the carrier versus Original Medicare. These plans most likely will not travel with you as they do not have a National PPO plan to cover you outside of your county region. They have limitations, and even though they may tell you about limited or no co-pays or low deductibles, they don't acknowledge that to offer the highest plans that you will pay for them - they're not free!

If individual control of your health is important to you, or if picking the doctor you want anywhere in the country is important to you, then what you really need to compare is the "free" plan to the "free" choice you have instead when taking Original Medicare and a Supplement.

What CMS rules actually say (regulatory fact): CMS approves Medicare Advantage plan marketing materials and has tightened guidelines in recent years, including restrictions on how supplemental benefits are presented in advertising. Celebrity endorsements are not banned, but the content of the ads must comply with CMS marketing rules. CMS has authority over Medicare Advantage and Part D marketing and can require corrections or take enforcement action, but consumers should still verify benefits in official plan documents rather than relying on ads alone. Whether those rules go far enough is where agent opinion starts.

What agents say (opinion): The majority of agents on Medicare Agents Hub believe these commercials are misleading, even if they technically meet CMS requirements. Their frustration centers on the gap between what the ad implies ("you qualify for all of this") and what's actually available in a given area. Several agents point out that when seniors call the 800 number on the screen, they reach a national call center, not a local agent who knows their county's plan options.

Why does Medicare allow insurance companies to bombard seniors with confusing mail and TV ads?

Insurance carriers are for-profit companies. Their Medicare Advantage plans make money by spending less on a member's healthcare than the government payments they receive from Medicare. So, the more people they enroll, the more money they make.The Centers for Medicare & Medicaid Services (CMS) has strict restrictions and guidelines on what insurance companies, agencies, and agents/brokers can and cannot advertise.

Unfortunately, many agencies and marketing firms slip in phrases like, "if eligible", and, "qualified members" with their ads. This is especially true when pushing Over the Counter (OTC) cards that can be used to pay for groceries.

I personally have had dozens of calls from seniors asking how they get their $[insert 4-digit number] check? I've had to explain that some ads walk the fine line using phrases that make it seem like people are entitled to big dollar checks, rebates, and even free dental coverage.

Bottom line is the are legal, provided they don't flat out say something that is definitely untrue (which is why they qualify with those phrases like "if eligible" and "qualified members" to enroll as many people as possible.

This is why it's wise to use a licensed health insurance broker who is certified to sell Medicare Advantage plans (like me) instead of going through Medicare.gov or an insurance agency where you talk to an agent in a call center who has quotas to meet.

The Dissenting View on TV Ads

Not every agent wants the commercials banned. A meaningful minority pushes back with two arguments worth hearing:

- CMS does approve these ads. Calling them "illegal" overstates the case. The carriers submit their marketing materials to CMS, and CMS signs off. The ads are regulated, even if many agents believe the regulation isn't strict enough.

- The ads get people thinking about Medicare. Some agents concede that the commercials serve a purpose: they prompt seniors who might otherwise ignore their enrollment window to actually look into their options. Even if the caller gets redirected from a call center to a local agent, at least the conversation started.

Where most agents agree, including the ones who defend the ads' existence, is that you should never enroll in a plan based on a TV commercial alone.

The "Food Card" and "Flex Card" Ads: What They're Really Selling

No single advertising tactic generates more agent frustration than the food card commercials. Agents describe fielding calls from seniors who saw an ad promising $100, $200, or more per month on a debit card for groceries, only to learn they don't qualify.

Here's what agents want you to understand about these ads:

The benefit is real, but the eligibility is narrow. Some Medicare Advantage plans do offer food or grocery allowances. These plans are typically Dual-Eligible Special Needs Plans (D-SNPs) for people who qualify for both Medicare and Medicaid, or Chronic Condition Special Needs Plans (C-SNPs) for people with specific diagnoses. If you do not have Medicaid, a qualifying chronic condition, or another plan-specific eligibility pathway, the headline benefit in the ad may not apply to you.

The ad is a lead generation tool. The purpose of the commercial isn't to enroll you in a specific plan. It's to get you to call a number. Once you call, your information may be sold to multiple agencies and brokers. Several agents describe clients whose phones "never stopped ringing" after responding to a single food card ad.

What's the most misleading Medicare Advantage ad you've seen, and how do you explain the reality to clients?

Oh, that’s easy. It’s the bait and switch ads about food cards, flex cards, grocery cards and free dental implants. The lead vendors putting those ads out there are flat out lying to people.The fact is that not everyone on Medicare is eligible for those cards. If you don’t have a low enough income to qualify for a high level of Medicaid or a certain illness to qualify for a Chronic plan, you aren’t getting a card, at least not the amounts being advertised. If you do get a card but don’t qualify for a high level of Medicaid or a Chronic plan, then I guarantee you that it won’t be a very big one, and you’re giving up something else like dental, vision or hearing, or you are paying higher out of pocket costs in terms of deductibles and copays. There is no such thing as a free lunch.

There is not a single Medicare Advantage Plan offered that will pay for an entire set of Dental Implants. In fact, most plans won’t pay for implants at all, and the few plans that will pay for any implants at all will only pay for one or two per year at the most.

I beg my clients to not call the numbers on those ads. First, they’re going to called 30 times a day from 8 AM to 8 PM every single day if they do, and if they answer those calls they’re likely to have their plan switched without their permission to something that may not cover their doctors or their prescriptions or not fit their needs in some other way.

Medicare just flat out isn’t doing enough to reign in the bad actors in the industry.

What you're giving up matters more than what you're getting. Even in cases where a food card benefit exists, the plan it's attached to may come with trade-offs that outweigh the card's value: smaller provider networks, higher copays for specialists, prior authorization requirements, or a maximum out-of-pocket that could cost thousands during a hospital stay.

I got a call from a "Medicare agent" promising me free groceries and I almost fell for it. Why is this kind of marketing allowed?

It’s unfortunate but there are a few loopholes in Medicare marketing guidelines that allow agents to discuss benefits associated with “DSNP’s” (Dual Special needs plans) on cold calls. These types of plans require that you have both Medicare and Medicaid, if you have both of these then there may be a DSNP plan available in your area that includes a”healthy food and produce” benefit that gives you a monthly allowance towards OTC items and groceries. Unfortunately I think a commonly used tactic is the “bait and switch”. Agents/brokers have to be a little more transparent if you were to physically meet them and go over your plan options. Be a good practice To ask these individuals “how are these benefits available to me” or simply just hang up. This sure isn’t a way to conduct good business but some brokers do engage in this.Robocalls and Unsolicited Phone Calls: The Hang-Up Rule

If your phone rings and someone you didn't contact starts talking about your Medicare benefits, agents have one piece of advice that comes up over and over: hang up.

What CMS rules actually say (regulatory fact): A Medicare plan representative or agent generally can't cold-call you out of the blue to sell a Medicare Advantage or Part D plan unless you gave permission, initiated contact, or already have a permitted relationship with the plan or agent. Third-Party Marketing Organizations (TPMOs) are also bound by these rules. CMS has a formal complaint process for violations.

Why agents say "just hang up" (and don't even say "no"):

Multiple agents warn that engaging with unsolicited callers carries risk. Scammers may record your voice, confirm your number is active, or use AI voice tools in future scams. The safest move with an unsolicited Medicare call is not to engage: hang up, then verify independently if you think the call might have been legitimate.

What's the best way for seniors to protect themselves from Medicare-related scams?

The Senior Medicare Patrol (SMP)—a national volunteer-led program—recommends a three-step approach: Protect, Detect, and Report.1. Protect: Guard Your Information

Treat your Medicare number like a credit card or your Social Security number.

The "No-Call" Rule: Medicare will never call you uninvited to ask for your Medicare number or Social Security number. If someone calls claiming to be from Medicare to offer you a "new plastic card" or "2026 benefits update," hang up immediately.

The Mail First Rule: Official Medicare communications almost always arrive by U.S. Mail first.

Avoid "Free" Offers: Be skeptical of anyone offering free medical equipment (like knee braces), genetic testing, or "wellness packages" in exchange for your Medicare number. These are often "kickback" schemes to bill Medicare for services you don't need.

2. Detect: Review Your Statements

Scammers often rely on the fact that many people don't read their paperwork.

Check your MSN/EOB: Every three months, you receive a Medicare Summary Notice (MSN) or an Explanation of Benefits (EOB) from your Advantage plan.

Look for "Phantom Billing": Look for charges for doctor visits you didn't attend, medical supplies you never received, or dates of service when you were at home.

Keep a Health Calendar: Jot down your doctor appointments and tests so you can easily cross-reference them with your statements later.

3. Report: Use Trusted Resources

If you suspect you’ve been targeted or see a suspicious charge, don't wait.

Call 1-800-MEDICARE: This is the primary line for reporting suspicious activity.

Contact your local SMP: The Senior Medicare Patrol (SMP) provides free, confidential help to seniors to help identify and report fraud.

Slam the Scam: If you receive a call from someone posing as a Social Security or Medicare official, you can also report it to the SSA Office of the Inspector General.

Where the calls actually come from: Most agents are quick to point out that the robocalls and aggressive phone tactics are not coming from local licensed agents. They come from overseas call centers, unlicensed lead vendors, and third-party marketing organizations that have found ways around CMS rules. Several agents express frustration that these bad actors make the entire industry look untrustworthy.

How to Protect Your Phone

| Step | What to Do |

|---|---|

| 1. Register | Add your number to the National Do Not Call Registry at donotcall.gov |

| 2. Don't engage | If you didn't initiate the call, don't answer questions, don't confirm your name, don't say "yes" |

| 3. Never share your Medicare number | Medicare will never call you to ask for your Medicare Beneficiary Identifier (MBI) or Social Security number |

| 4. Report it | File complaints with 1-800-MEDICARE (1-800-633-4227) or your State Health Insurance Assistance Program (SHIP) |

| 5. Work with a local agent | Find a licensed agent in your area so you have a trusted contact and don't need to rely on inbound calls |

How to Verify What You're Seeing and Hearing

Whether it's a mailer, a TV ad, or a phone call, agents recommend the same verification steps before you act on any Medicare marketing:

Check Medicare.gov directly. The Medicare.gov Plan Finder lets you look up every Medicare Advantage and Part D plan available in your ZIP code. Start there, then confirm the benefit in the plan's Summary of Benefits, Evidence of Coverage, or by calling the plan directly. If the ad claim does not appear in the official plan documents, do not rely on the ad. (For a walkthrough of how to pick the right agent to help you compare, we've got a separate guide.)

Read the Summary of Benefits and Evidence of Coverage. Every Medicare Advantage plan is required to provide these documents. The Summary of Benefits is the quick version; the Evidence of Coverage is the full legal document. Both are available on Medicare.gov or from the carrier directly. Don't rely on a commercial or mailer when the official documents exist.

Ask your agent to review it. Multiple agents describe a service most seniors don't realize they can request: bring your stack of mail to your agent and go through it together. Agents call this a "mailbox sort" or a teaching moment, and they use it to separate legitimate plan information from marketing noise.

How can I verify if a Medicare Advantage plan's advertised benefits are legit?

Start by going directly to Medicare.gov and using their plan finder tool to look up the specific plan. Everything a Medicare Advantage plan offers has to be filed with CMS, so the official details will be there including premiums, copays, drug coverage, and extra benefits. Compare what you see on Medicare.gov with what the plan is advertising. You can also request the plan's Summary of Benefits and Evidence of Coverage documents, which spell out exactly what's covered and what's not. If something sounds too good to be true, like free groceries or extensive dental with no catches, dig into the fine print because those benefits often have limits, eligibility requirements, or only apply in certain situations. And if an agent is pushing a plan hard without answering your questions directly, that's a red flag. You can also call 1-800-MEDICARE to ask about a specific plan or report misleading advertising.Why Agents Say the Real Problem Isn't the Ads Themselves

When asked whether CMS should impose stricter regulations on Medicare Advantage marketing, agents land in different camps, but most circle back to the same deeper problem: the ads work because seniors don't have enough baseline education about how Medicare actually works.

Agents who have watched clients sign up for "$0 premium" plans without understanding copays, networks, or prior authorization describe a pattern: the advertising isn't technically lying, but it's counting on the viewer not knowing enough to ask the right follow-up questions.

This is why the single most repeated piece of advice across all 300+ answers isn't about any specific ad or mailer. It's this: work with an independent, licensed Medicare agent or broker who represents multiple carriers. Not a call center. Not a captive agent who can only show you one company's plans. An independent broker who can compare options across carriers and has no incentive to steer you toward one plan over another.

Are Medicare Advantage plans really "free," or is that just clever marketing?

You've heard that "there's no such thing as a free lunch." Well, the same is true of Medicare Advantage plans.While it's true that there are Medicare Advantage plans that cost $0 in premium, they are not 'free' for a variety of reasons:

1. In order to qualify for a Medicare Advantage plan, you must have both Medicare Part A and Medicare Part B. There is a premium for Part B that must be paid every month.

2. You accept the terms and conditions of the Medicare Advantage plan that you choose, and that includes copayments and an out-of-pocket maximum for the services you receive. The fees you pay could add-up to thousands of dollars each year. While Medicare Advantage plans must be at least as good as Original Medicare, there will certainly be a cost to receiving medical care under Medicare Advantage.

3. Your Medicare Advantage plan is being paid by Medicare. Because they have taken-over responsibility for your medical needs, Medicare pays them a portion of what they expected to pay for your claims. The Medicare Advantage plan then decides how to spend that money in benefits. As the Medicare budget changes every year, so does the Medicare Advantage plan. It is important to review the changes in your Medicare Advantage plan every year.

4. You may end-up benefiting from Medicare Advantage by paying a little more for your medical claims, while receiving "extra" benefits like dental, vision, hearing, fitness, prescription drug and over-the-counter drug benefits at little to no cost. But in a year where you have a lot of expensive medical treatment, you could pay a lot more out of your pocket.

Editor's note: Medicare Advantage plans must cover nearly all Part A and Part B benefits, but that does not mean every Medicare Advantage plan is better than Original Medicare for every person. Networks, drug coverage, prior authorization, out-of-pocket costs, and provider access all vary by plan and should be reviewed carefully. Agent opinions expressed above are their own and do not represent a recommendation from Medicare Agents Hub.

The Scope-of-Appointment Rule You Should Know About

Regulatory fact: Before a personal marketing appointment about Medicare Advantage or Part D plans, the agent or broker must document a Scope of Appointment (SOA) showing which plan types you agreed to discuss. For in-person personal marketing appointments, the SOA must be in writing. This form protects you by keeping the conversation focused on what you actually want to learn about. If someone starts pitching you a specific plan during a personal appointment without documenting an SOA first, that's a red flag worth paying attention to.

The Bottom Line from 300 Agents

The mail will keep coming. The commercials won't stop. Your phone will ring during dinner. Agents know this because they hear about it from every client who walks through the door.

What they want you to take away from all of it:

- Your mailbox is not your enrollment guide. Sort it into three piles (keep, research, shred) and don't let urgency language pressure you into calling a number you don't recognize.

- Celebrity commercials are advertisements, not recommendations. The benefits shown may not exist in your county, and the number on screen connects to a call center, not a local expert.

- Food card and flex card ads target a narrow audience. If you don't have Medicaid, a qualifying chronic condition, or another plan-specific eligibility pathway, the headline benefit in the ad may not apply to you.

- Hang up on unsolicited calls. A Medicare agent or plan representative generally can't cold-call you unless you gave permission or have an existing relationship. If someone calls you out of the blue about Medicare, that's a red flag.

- Verify everything on Medicare.gov. Start with the Plan Finder, then confirm in the plan's official documents. If the ad claim isn't in the documents, don't rely on the ad.

- Find a local, independent agent. An agent who represents multiple carriers and sits across the table from you will always give you a more complete picture than a TV commercial or a 1-800 number. You can search for one here.

What are the reasons why I should work with a Medicare agent?

Working with a Medicare agent can be especially helpful because Medicare is complex and the “best” plan really depends on your doctors, medications, and budget. Here are the key reasons people choose to work with one:1. Medicare is complicated

Medicare isn’t just one plan. You have:

Original Medicare (Parts A & B)

Medicare Advantage (Part C)

Prescription Drug Plans (Part D)

Medigap (Supplement) plans

An agent helps explain the differences in plain language and avoids costly mistakes.

2. Personalized plan matching

A good Medicare agent:

Checks your doctors and hospitals for network coverage

Reviews your prescriptions to lower drug costs

Compares premiums, deductibles, copays, and max out-of-pocket costs

This ensures the plan actually fits your healthcare needs—not just the cheapest premium.

3. Access to multiple insurance companies

Independent Medicare agents (like you 😊) can compare many carriers at once, not just one company’s plans, giving clients more options and better value.

4. Help avoiding penalties

Agents help people:

Enroll on time

Avoid late enrollment penalties for Part B and Part D

Understand Special Enrollment Periods when life changes happen

5. Ongoing support after enrollment

A Medicare agent doesn’t disappear after enrollment. They help with:

Plan changes during Annual Enrollment

Claims and billing issues

Prescription changes

Appeals and coverage questions

6. No extra cost to the client

Medicare agents are paid by the insurance companies—not the consumer—so clients get expert help at no additional cost.

7. Advocacy and peace of mind

If something goes wrong, your agent can:

Call the insurance company on your behalf

Explain denial letters

Help you switch plans if your needs change

This is especially valuable for seniors and caregivers who feel overwhelmed.

8. Local knowledge

Local agents understand:

Regional hospital systems

Local plan strengths and weaknesses

State-specific Medicare rules

That insight can make

Agents may not represent every plan in your area. You can also contact Medicare.gov, 1-800-MEDICARE (1-800-633-4227), or your local SHIP for information on all available options.

If you've already been approached by someone who raised red flags, trust your instincts. And if you're weighing whether a free Medicare seminar is worth your time, that's a different channel with its own set of questions to ask.