Trade-Offs That Come with Medicare Advantage

-

Last Updated July 22, 2026

While Medicare Advantage plans are known for bundling benefits and offering cost-effective options for many seniors, they aren't without trade-offs. When asked about the biggest disadvantage of Medicare Advantage, brokers across the country pointed to recurring concerns from their clients. Though experiences vary depending on geography, health needs, and plan design, several clear themes emerged from the insights shared by licensed agents. These include issues like provider access, delays in care approval, high out-of-pocket risks, and more. Here is a breakdown of the most commonly reported concerns, drawn from agent responses on the topic.

Limited Provider Networks

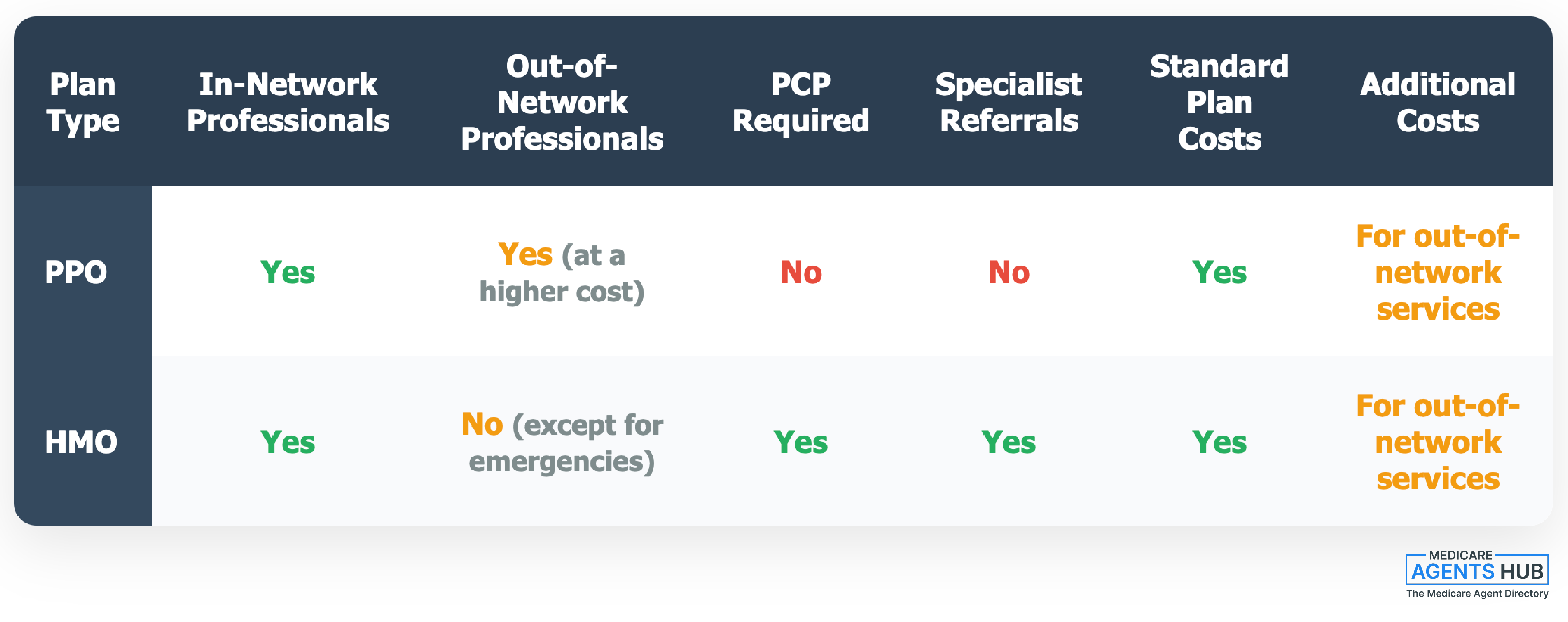

One of the most widely mentioned disadvantages was the issue of network limitations. Many Medicare Advantage plans require enrollees to use specific doctors and hospitals that are part of the plan’s contracted network. This can present challenges, especially for individuals who travel frequently, have preferred specialists, or move between states.

The structure of these networks varies between HMO and PPO plans, but both can limit flexibility compared to Original Medicare. If a provider leaves the network, enrollees may find themselves needing to switch doctors or pay higher out-of-pocket costs to continue seeing their preferred providers. This issue is compounded by the fact that networks can change annually, requiring beneficiaries to verify each year that their doctors are still included. It's a frustration shared by physicians as well - many have their own concerns about why doctors don't like Medicare Advantage and how network restrictions affect patient care.

In more restrictive plans, like HMOs, participants may need a referral from a primary care provider before seeing a specialist. This setup, while manageable for some, can be frustrating for those used to choosing any Medicare-approved provider without restrictions. The possibility of having to coordinate care entirely within a narrow group of providers was repeatedly flagged as a drawback.

Worried About Keeping Your Doctor?

An independent Medicare agent can check your doctors, specialists, and hospitals against every Medicare Advantage plan available in your area — at no cost to you.

Can I keep seeing my current doctors if I switch to a Medicare Advantage plan, or do I have to find new ones?

Short answer: maybe — but you have to check first.With a Medicare Advantage plan, everything hinges on the network. Before enrolling, a good independent Medicare broker should help you confirm two critical things up front:

• Are your prescription drugs covered?

• Are the doctors you trust in the plan’s network?

Depending on how many doctors you see — and which health systems they’re associated with — that may or may not work out. There are no perfect Medicare plans, but there are solid ones. That said, if your “must-keep” list of doctors is long, asking a Medicare Advantage plan to accommodate all of them can be a tall order.

If network access is a concern, a PPO may be an option if one is available in your area. PPOs offer more flexibility but usually come with higher costs when you go outside the network. All else being equal, most beneficiaries do best with an HMO that has a large, well-established provider network.

The bottom line: don’t assume — verify. Checking your doctors before you enroll can save you a lot of frustration later.

Prior Authorization Delays on Complex Care

Another major concern shared by several professionals was the requirement for prior authorizations. These are approvals that must be obtained from the insurance provider before certain treatments, procedures, or medications are covered. While intended to control costs and ensure medical necessity, prior authorization requirements often introduce delays in care, and brokers say the friction shows up most on complex care cases: cancer treatment, cardiac procedures, advanced imaging, and specialty medications.

These delays can be particularly problematic for individuals facing time-sensitive medical issues. Waiting for approval can be stressful and may result in postponed diagnostics or treatment. In some cases, procedures that would be covered under Original Medicare without pre-approval require multiple steps and administrative hurdles under a Medicare Advantage plan.

The need for prior authorization was cited not just as a technical inconvenience but as a barrier that could affect the timeliness and quality of care. When dealing with serious or complex health conditions, even a short delay may feel like a long time, and that uncertainty is a source of frustration for many.

Risk of High Out-of-Pocket Costs

Several professionals noted that one of the most overlooked drawbacks of Medicare Advantage is the potential for high out-of-pocket costs, especially in the event of serious illness or ongoing treatment. While Medicare Advantage plans often advertise low or $0 premiums, the real financial exposure comes through cost-sharing (copayments, coinsurance, and deductibles) which can add up quickly.

Some beneficiaries reportedly enter these plans without a full understanding of their Maximum Out-of-Pocket (MOOP) limits. If a serious condition arises, such as cancer, heart disease, or a stroke, it’s possible to hit that cap within a single year. The shock of encountering large, unexpected expenses becomes a pain point for those who may have believed they were fully covered.

In contrast to Medigap policies that provide more predictable coverage, Medicare Advantage shifts the cost burden onto the user in the form of "pay-as-you-go" structures. While these may be cost-effective for individuals with minimal medical needs, those requiring frequent or complex care might find the financial responsibility burdensome. The possibility of needing to pay thousands in a year, even while enrolled in a plan, is something that many beneficiaries don’t fully anticipate until they’re faced with it.

What is the biggest disadvantage of the Medicare Advantage plans?

The biggest disadvantage to Medicare Advantage plans are the copays, coinsurance and networks. While most Advantage plans are low or no premium, the out of pocket expenses can really add up. A lengthy hospital stay with a surgery can cause a major financial hardship for Medicare beneficiaries.Control by Insurance Companies

Another consistent concern raised was the fact that Medicare Advantage plans are managed by private insurance companies rather than by Medicare itself. This arrangement introduces a layer of corporate policy-making that can influence how care is accessed, which treatments are approved, and what coverage decisions are made.

Some professionals noted that decisions around care are no longer made purely based on clinical need, but may also reflect what the insurance company is willing to approve or reimburse. This creates situations where enrollees are subject to rules and restrictions that wouldn’t exist under Original Medicare, such as prior authorizations or limited networks.

Because these companies effectively administer the plan, beneficiaries may feel like they're navigating a more complex system, where access to care is filtered through a for-profit entity. This difference in control was cited as a philosophical and practical disadvantage, especially when it impacts speed, flexibility, or fairness in decision-making related to patient care. It's also one of the things Medicare agents wish they could change about the system entirely.

Difficulty Switching Back to Medicare Supplement Plans

A less commonly discussed but highly significant issue involves the ability, or rather the lack thereof, to return to a Medicare Supplement plan after being enrolled in Medicare Advantage. In many cases, if someone decides to leave their Medicare Advantage plan after the first year, they may face health underwriting when applying for a Supplement plan. This means that individuals with conditions such as cancer, stroke, heart disease, or chronic respiratory illness might be denied coverage. Outside of a narrow set of guaranteed-issue rights, Medicare.gov confirms the specific windows in which insurers must sell you a Medigap policy regardless of health.

Several responses highlighted this as a potentially irreversible decision point. Once someone develops a serious health issue while on a Medicare Advantage plan, it can become nearly impossible to transition back to a Supplement plan that offers more expansive, flexible coverage without network restrictions. In this way, Medicare Advantage can lock some beneficiaries into a structure that may no longer meet their evolving health needs, with no viable route back to broader coverage.

This risk isn't always fully explained during initial enrollment, which can lead to surprise and regret down the line. It underscores the importance of understanding not just the short-term advantages of a plan, but also its long-term implications, particularly as health status changes with age. For a detailed walkthrough of the enrollment windows, rules, and strategies for making the transition, read our guide on switching from Medicare Advantage back to Original Medicare.

Why do some people regret choosing a Medicare Advantage plan over Original Medicare?

Some people regret choosing Medicare Advantage because they run into limits with doctors or hospitals, or they’re surprised by the copays and authorizations required for care. It often looks cheaper upfront, but the restrictions and out-of-pocket costs can make Original Medicare with a supplement a better fit for some.Geographic Limitations and Travel Concerns

Travel-related limitations came up in several responses, especially from those who work with clients who move between states or spend part of the year in another region. Medicare Advantage plans often do not provide consistent coverage outside of a beneficiary’s home service area. If someone travels frequently or splits time between different states, they may find their access to care restricted when away from their plan’s coverage zone.

Even within the United States, seeing out-of-network providers while traveling can lead to higher costs or outright denials of coverage. It's worth being precise here: Medicare Advantage plans are required to cover emergency and urgent care nationwide, so a heart attack or broken bone on a road trip will be treated. But routine and follow-up care (a check-in with a specialist, physical therapy, non-urgent imaging) is usually limited to the plan's network and service area, which is where snowbirds and frequent travelers most often run into trouble.

For beneficiaries who value flexibility and want reliable access to care across state lines, this geographic limitation was cited as a real disadvantage. While Original Medicare allows people to visit any provider who accepts Medicare nationwide, Medicare Advantage typically does not, and that contrast was a repeated theme among the professional insights.

Miscommunication or Lack of Clarity During Enrollment

A number of professionals pointed out that some disadvantages stem not from the plan design itself, but from the way these plans are explained (or not explained) to prospective enrollees. In some cases, beneficiaries reported feeling confused or misinformed about key aspects of their coverage after enrollment, particularly around out-of-pocket costs and network restrictions.

Some professionals highlighted instances where important information such as the Maximum Out-of-Pocket limit or the limits of provider networks was either downplayed or not mentioned at all during the sales process. This lack of transparency can lead to frustration when enrollees later discover that their doctor is not in-network, or that a service they assumed was covered actually requires prior approval or additional costs.

The problem isn’t always intentional misrepresentation, but often a result of fast-paced or high-volume sales environments where full plan details are not clearly conveyed. Regardless of the cause, the result is the same: beneficiaries may enter a plan without fully understanding how it works, and only realize the downsides when they need care.

Less of a Disadvantage for Some Individuals

While the focus of this article is on the disadvantages of Medicare Advantage, it’s worth noting that several professionals expressed relatively positive views, or at least qualified the disadvantages based on context. A few noted that when structured as a PPO, rather than an HMO, many of the common drawbacks such as restrictive networks or referral requirements are reduced.

For healthy individuals with low medical usage, Medicare Advantage’s pay-as-you-go model may be quite manageable. A Medicare Advantage plan often works well when the enrollee:

- Is generally healthy and uses relatively little care in a typical year

- Lives year-round in one area and doesn’t travel for months at a time

- Already sees doctors and hospitals that are in the plan’s network

- Wants a low or $0 premium and is comfortable paying copays as care is used

- Values bundled extras like dental, vision, hearing, or a prescription drug plan built in

The bundled additional benefits, such as dental, vision, or transportation services, were seen as positives that can outweigh some of the structural concerns, depending on a person’s specific needs and expectations. That said, not all of these extras deliver the value they promise; take a closer look at the most overhyped Medicare Advantage benefits before letting them drive your decision. Grocery and food card benefits, for instance, were a major draw for many plans — but most were eliminated at the start of 2026 after CMS implemented new restrictions on how they could be offered.

However, these acknowledgments did not negate the issues raised in earlier sections. Instead, they framed them as more situational: for the right person with the right plan, the disadvantages might not feel particularly limiting. The key takeaway is that whether or not a Medicare Advantage plan becomes problematic often depends on how well it aligns with the individual’s health profile, travel habits, and provider preferences.

The Bottom Line on Medicare Advantage Disadvantages

The insights shared by professionals paint a clear and detailed picture of the most frequently encountered disadvantages of Medicare Advantage plans. While these plans offer low premiums and attractive extras, they also come with trade-offs that may impact care access, costs, and flexibility.

Recurring concerns include limited provider networks, the need for prior authorizations, exposure to high out-of-pocket expenses, and control of care by private insurance companies rather than Medicare itself. Additionally, the risk of being unable to return to a Medicare Supplement plan due to health changes adds a layer of long-term uncertainty that many don’t anticipate during enrollment. For those who travel often, geographic limitations can also pose challenges, and the way plans are communicated upfront sometimes leaves beneficiaries unaware of important restrictions or potential financial exposures.

Still, there are situations where the disadvantages are less pronounced, particularly for individuals who remain healthy, don’t travel frequently, and are enrolled in PPO-style plans that offer more flexibility. Ultimately, choosing a Medicare Advantage plan requires a thoughtful look at current and future health needs, as well as a full understanding of what the plan does and doesn’t cover.

By highlighting these disadvantages through real-world observations from licensed professionals, this article aims to support a more informed enrollment experience. The better someone understands their plan going in, the fewer surprises they’re likely to face down the road.

Before You Enroll, Get a Second Opinion

A licensed independent agent can walk through your doctors, prescriptions, expected out-of-pocket costs, and travel plans against every Medicare Advantage option in your area — and flag the trade-offs that would actually affect you. It's free, and there's no obligation to enroll.