The Truth About "Free" Medicare Advantage Plans, According to Experts

-

Last Updated July 21, 2026

Are Medicare Advantage Plans Really “Free”? Agents Across the Country Weigh In

Medicare Advantage plans often come with flashy promises like "$0 premiums" and “no-cost coverage”, but are they really free? To find out, Medicare Agents Hub asked licensed insurance professionals across the country to weigh in, and their answers uncovered the truth behind the marketing: there are real costs, and they don’t always show up in the fine print.

While the phrase “$0 premium” might catch the eye in a TV commercial or postcard ad, agents made it clear: that doesn’t mean no cost. Here’s what emerged from the responses, grouped into the most common themes professionals emphasized.

Key Takeaways

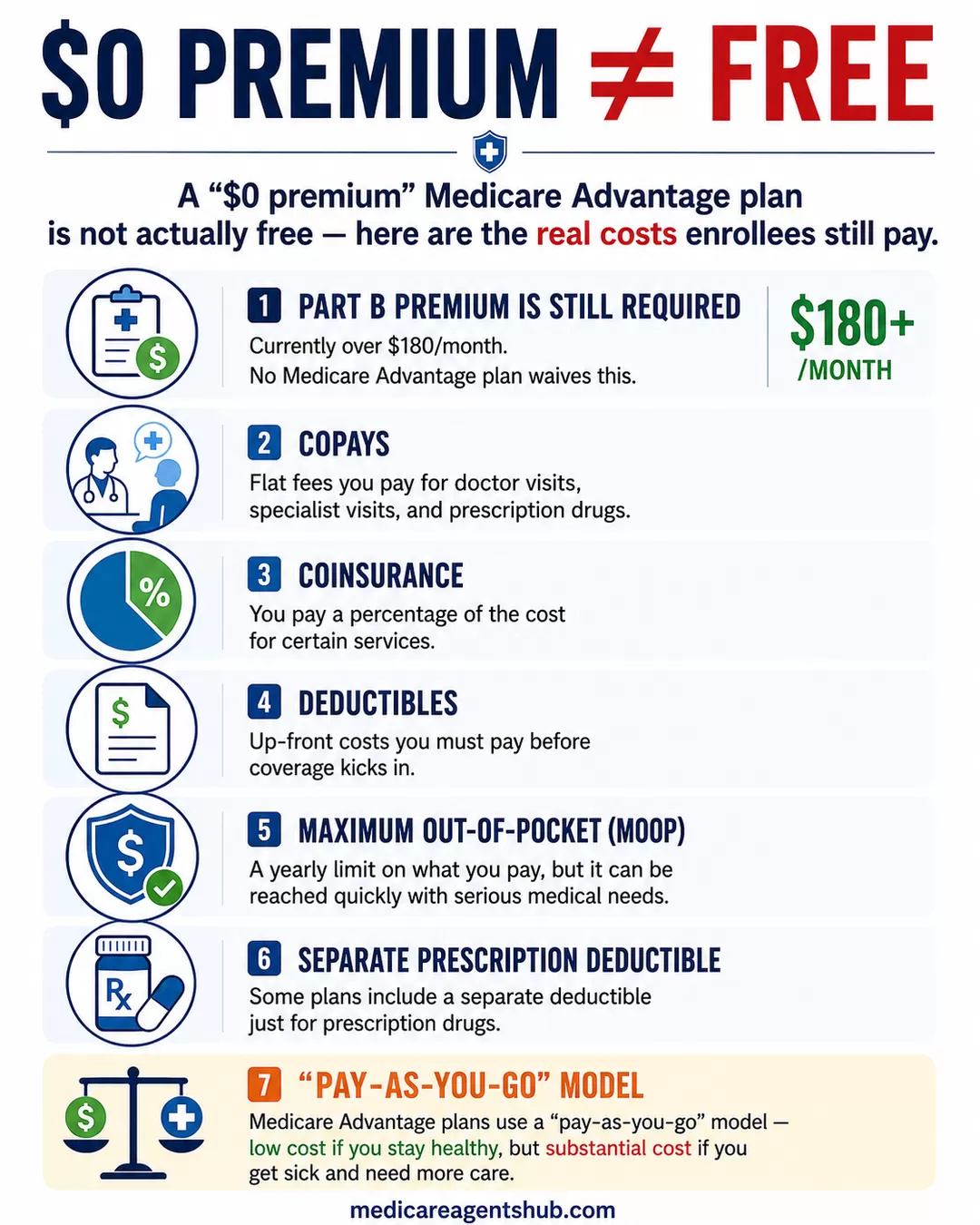

- Not truly free: You still pay your monthly Medicare Part B premium.

- Pay-as-you-go: $0 premium plans usually come with copays, coinsurance, and deductibles when you use services.

- Someone is paying: "Free" plans are heavily funded by federal (taxpayer) subsidies to private insurers.

- Extras are marketing: Grocery cards, gym memberships, and OTC benefits shouldn't drive the decision — medical coverage should.

- Location matters: Plan availability, costs, and networks vary by county and zip code.

Why Are Some Medicare Advantage Plans Free? The Reality Behind “$0 Premium”

A central theme that surfaced again and again was the distinction between a $0 premium and actual free healthcare. Multiple agents explained that many Medicare Advantage plans advertise no monthly premium because private insurance companies are paid by Medicare to coordinate beneficiaries’ care. That federal funding allows them to waive a monthly fee in some plans, but that doesn’t mean members are off the hook financially.

Every respondent emphasized that to even qualify for a Medicare Advantage plan, beneficiaries must be enrolled in Medicare Part B, which comes with a standard 2026 monthly premium unless reduced through income-based assistance. That cost alone means no Medicare Advantage plan is truly “free.”

Beyond that, the availability of zero-premium plans varies by geography. Some enrollees may have access to plans with added benefits, including features that apply a credit toward their Part B premium. Others may not. Ultimately, what’s available depends heavily on the enrollee’s county or zip code.

Still, the consensus was clear: the term “free” doesn’t accurately reflect the full picture. The $0 premium might reduce one type of cost, but the system behind Medicare Advantage plans is built on federal subsidies, and those subsidies come from taxpayers. The enrollees may not always see a bill, but someone is paying the cost.

Are Medicare Advantage plans really "free," or is that just clever marketing?

Medicare Advantage plans are often marketed as "free," but this can be misleading. Here's a breakdown to clarify:1. **Monthly Premiums**: While some Medicare Advantage plans have low or even $0 monthly premiums, you may still be responsible for other costs, such as copayments, deductibles, and coinsurance.

2. **Medicare Part B Premium**: Even if the Advantage plan itself is free, you still need to pay your Medicare Part B premium, which is typically deducted from your Social Security benefits.

3. **Out-of-Pocket Costs**: Many plans have out-of-pocket expenses that can add up, especially if you require frequent medical care or services.

4. **Network Restrictions**: Many Advantage plans have specific networks of providers, and going out of network can result in higher costs or no coverage at all.

5. **Limitations on Coverage**: While these plans often include additional benefits (like dental or vision), they may not cover everything that traditional Medicare does, which can lead to unexpected costs.

So, while some aspects of Medicare Advantage plans can appear "free," it's essential to carefully review the details and understand all potential costs involved before enrolling. It’s always a good idea to compare plans and consider your healthcare needs.

Common Costs and Hidden Fees in Medicare Advantage Plans

Another near-universal message from the agents was that significant costs can and do exist, especially once someone actually starts using their plan. Zero premium or not, Medicare Advantage plans typically require copays for services, coinsurance, and deductibles before coverage kicks in.

The details vary by plan, but respondents laid out a consistent set of expectations. Members can expect to pay flat fees for doctor visits or prescriptions (copays), a percentage of certain services (coinsurance), and possibly up-front costs (deductibles). Many plans also include a maximum out-of-pocket (MOOP) amount, essentially a yearly ceiling on how much someone could be required to spend. Depending on their health, a person might barely reach that ceiling, or they might hit it quickly.

Several agents described this as a “pay-as-you-go” model: you might pay very little if you stay healthy, but serious medical needs can lead to substantial costs. Compared to Medicare Supplement plans, which often have more predictable pricing structures, Advantage plans can feel riskier.

These costs vary not just by plan type, such as HMO or PPO, but also by location. A plan in one area could offer very different terms than the same insurer’s plan in another region. Some Advantage plans also include separate deductibles for prescriptions, which further complicates the pricing picture.

Ultimately, the agents emphasized that zero premium is only one part of the cost equation. Anyone considering a Medicare Advantage plan must review the full Summary of Benefits to understand what they'll be responsible for when they need care.

I picked a Medicare Advantage plan based on the low premium, but now I'm facing high copays. Did I make a mistake?

Not necessarily. I think you must look at, what is the chance I am going to have ongoing health issues? Are you going to have to pay these co-pays every year? And also, even if you do, Will these copays equal more than the monthly premium, I would have paid for a Medicare supplement and a standalone PDP plan? You may consider buying a hospital indemnity plan. These policies help with out-of-pocket copays and still cost less than Medicare supplements. You can use them in conjunction with your Medicare Advantage plan.The “Pay-As-You-Go” Model and Financial Risk

One of the more striking patterns in the responses was how many agents described Medicare Advantage plans as a “pay-as-you-go” healthcare model. Unlike traditional Medicare paired with a Supplement plan, where members often pay higher premiums but have more predictable coverage, Advantage plans may look cheaper on the surface but can carry higher financial risk down the line.

The agents warned that these plans may appear appealing to someone in good health, since costs like copays and deductibles are only triggered when services are used. For someone who rarely visits the doctor, the out-of-pocket costs might remain low. But health can be unpredictable, and the agents noted that when medical needs increase, so do the expenses.

Several responses emphasized the unpredictability built into Advantage plans. Copays for specialist visits, hospital stays, or diagnostic tests can add up quickly. While plans do have an annual cap, the maximum out-of-pocket limit, those caps can still represent thousands of dollars. The agents collectively stressed that it’s impossible to know in advance what healthcare issues may arise during the year, and that reality should factor into the decision-making process.

They also pointed out that some plans come with both health and prescription deductibles, further complicating the cost landscape. These upfront amounts must be paid before certain benefits even kick in, adding another layer of potential financial strain.

Ultimately, the consensus was that while Medicare Advantage plans might save money in a “good year,” the financial risks in a “bad year” shouldn’t be underestimated. It’s not just about whether a plan has a premium. It’s about whether someone is financially prepared for variable, usage-based costs.

What is the biggest disadvantage of Medicare Advantage?

The biggest disadvantage to a Medicare Advantage plan is the limited network of doctors and hospitals and care access. If you choose to see a doctor or visit a hospital, out of network expenses can be very expensive and the plan may not cover out of network expenses at all. Medicare advantage plans may only allow you to use certain durable medical equipment within the plan.Sometimes, plans may require that you get a referral or prior authorization. For example, the HMO plans may require that you see the primary care physician who is the gatekeeper to get a referral to see a specialist.

Medicare Advantage plans are typically restricted to the local area. If you travel, it is important to consider that you may not be able to see a doctor or specialist unless it is an emergency situation.

Medicare Advantage costs can be unpredictable. You will want to check all of the details of the plan to include copays, coinsurance and deductibles as well as the maximum out of pocket amount for the calendar year. Medicare beneficiaries who choose a Medicare Advantage plan need to consider utilization which factors into the unpredictability of costs.

Extra Benefits: A Powerful (but Sometimes Misleading) Draw

Another reason Medicare Advantage plans continue to grow in popularity is their extra perks, and nearly every agent who responded mentioned them. These additional benefits often include dental, vision, hearing, fitness memberships, over-the-counter (OTC) allowances, and even healthy food and grocery card benefits — though many grocery-related perks were scaled back or eliminated at the start of 2026. For many consumers, these offerings make Advantage plans seem like an obvious choice.

But the agents urged caution. While these extras are real, they can also distract from the core costs of medical care. Some described the added benefits as a marketing hook, an enticing front-end incentive that draws attention away from the plan’s less predictable backend expenses. The availability and scope of these benefits can vary greatly by plan and location, and not all of them are as comprehensive as they may seem at first glance.

In some cases, these benefits are only lightly used or are bundled in a way that doesn’t suit every enrollee’s needs. Agents advised consumers to weigh these perks against the fundamental medical coverage, since flashy extras don’t offset high copays, prior authorization requirements, or restrictive networks when more serious care is needed.

Several professionals also pointed out that advertising for Medicare Advantage plans is tightly regulated and must be approved by Medicare. That said, even legitimate advertising can feel misleading if consumers don’t take the time to look past the glossy brochures and compare the fine print. In fact, misleading MA marketing is just one of several systemic issues agents wish they could change about how Medicare works today.

In summary, while the extra benefits offered by Medicare Advantage plans can add value, agents emphasized that they shouldn’t be the main reason someone selects a plan. The foundation of any Medicare decision should be affordability, access to care, and protection from unexpected costs, with bonus perks seen as just that: bonuses, not the base.

Who’s Really Paying? Behind the Marketing and Government Cost Structure

When Medicare Agents Hub gathered insights on whether Medicare Advantage plans are truly “free,” several professionals raised a key point: if consumers aren’t paying up front, someone else is footing the bill. And that someone is the federal government—and by extension, taxpayers.

Multiple agents made it clear that while Medicare Advantage plans often cost $0 in monthly premiums for the enrollee, they aren’t without cost to the system. Private insurance companies are reimbursed by Medicare to take over beneficiaries’ care, and that cost structure adds up. In fact, Advantage plans were described as costing the government more than traditional Medicare. In some estimates, by over 20% — a gap consistently flagged in the MedPAC March 2025 Report to Congress.

There are several reasons for this higher cost. For one, the commission structure for Advantage plans tends to be higher than for Medicare Supplement plans, which drives marketing and sales efforts toward the Advantage market. Advertising and outreach campaigns are more aggressive, and more expensive. Some respondents also pointed to lobbying efforts by Advantage plan providers that have resulted in additional payments for managing higher-risk enrollees. These bonus payments are often based on an enrollee’s health profile, regardless of whether they actually consume more care.

All of this means that while a Medicare Advantage enrollee may see “$0” on a premium line, the cost is very real—just distributed differently. The bottom line from the agents: calling these plans “free” is a mischaracterization. They are heavily subsidized, and those subsidies are built into the overall cost of the Medicare system.

How can insurance companies afford to offer Advantage plans with $0 monthly premiums?

$0 premium Medicare Advantage plans can exist because they are funded differently than many people assume — they are heavily supported by federal payments.Here’s how insurers make it work:

1. Federal funding (capitation payments)

Medicare pays private insurance companies a fixed amount each month for every enrolled beneficiary. If the insurer manages care efficiently, it can use those funds to offset or eliminate the plan premium.

2. Cost-sharing structure

Even with a $0 premium, members still pay copays, coinsurance, and deductibles when they use services. This shifts part of the cost from fixed premiums to pay-as-you-go healthcare usage.

3. Network management

Most Advantage plans use provider networks and negotiated rates to control expenses, similar to employer health plans.

4. Star Ratings bonus payments

Plans that achieve high quality scores from Medicare can receive bonus funding — often used to enhance benefits or keep premiums low.

5. Supplemental benefits attract healthier members

Extras like dental, vision, and fitness help broaden the risk pool. When healthier individuals enroll, overall claims costs can decline.

Comparing Plans and Navigating Local Differences

Another theme that surfaced throughout the responses was the importance of regional variation and personalized plan comparison. Medicare Advantage is not a one-size-fits-all solution. Plans differ widely not only between insurance providers, but even from one county or zip code to another. What might be an excellent plan for one person could be completely unsuitable for someone else just a few miles away.

Some respondents noted that even within the same insurer, plan terms, such as copays, coverage networks, and included benefits, can differ by area. That’s why reviewing a plan’s Summary of Benefits is essential. It’s not enough to look at surface-level advertising or assume a plan offers blanket coverage across the country.

Can eligibility for certain Medicare Advantage plans depend on where I live?

Medicare Advantage plans are approved and offered on a county by county basis, meaning the plans available to you depend entirely on where you live. Someone in a major metropolitan area may have dozens of plan options to choose from, while someone in a rural county may have very few or in some cases none at all. This also means that if you move to a different county or state you trigger a Special Enrollment Period and need to find a new plan, because your current Medicare Advantage plan likely will not follow you to your new address. Plan benefits, premiums, and networks can vary significantly from one county to the next even within the same state and with the same carrier. If you are considering relocating, it is worth researching what Medicare Advantage options are available in your destination area before you move so you are not caught off guard by a limited selection or a plan that does not meet your needs.A recurring message was the need for individualized support when comparing plans. Because so many variables come into play (cost-sharing structures, provider networks, extra benefits, eligibility rules), having a knowledgeable source to walk through the differences can be invaluable. Several responses alluded to the role that a licensed agent or broker can play in helping consumers navigate these choices, especially when plans are marketed using simplified or attractive language.

In short, the professionals who weighed in through Medicare Agents Hub agreed: Medicare Advantage plan selection requires careful review and context-specific decision making. What looks affordable may not be, depending on how—and where—you plan to use it.

Final Word: “Free” Is a Misleading Term

After collecting responses from professionals nationwide through Medicare Agents Hub, one conclusion stands out: Medicare Advantage plans are not truly “free.” While the phrase might appear on advertisements and mailers, every agent who contributed agreed: there’s more to the story.

At a glance, $0 monthly premiums make these plans sound enticing. But once someone is enrolled, the financial reality becomes clear: Part B premiums, copays, coinsurance, deductibles, and potential out-of-pocket maximums can all add up quickly. These plans operate on a “use it, pay for it” basis, which means members must be prepared for fluctuating healthcare costs depending on how much care they need.

Some respondents highlighted the marketing power of added benefits (dental, vision, hearing, gym memberships, over-the-counter credits, and more) but warned that those features shouldn’t overshadow the core cost of care. These perks may help sway consumers, but they don’t eliminate copays or reduce financial risk during a serious illness.

Another major takeaway was the role of taxpayer dollars in propping up Advantage plans. These plans don’t operate in a vacuum. They’re part of a system that allocates billions in federal funding to private insurers. That funding structure allows for zero-premium plans but also contributes to higher government spending compared to Original Medicare.

My neighbor says I'm crazy for paying for a Medigap plan when Medicare Advantage is "free." What should I tell him?

Anyone near Medicare age understands that "free" products oftentimes have the highest price tag.It is true that there is an abundance of "free" Medicare Advantage (MA) plans. It is also true that many of these plans have deductibles, co-pays, co-insurance, and other out-of-pocket costs creating financial stress on patients.

Unfortunately, most MA policyholders do not understand the full range of these costs until they need ongoing medical care.

The true cost of health plans are not only calculated in the premium, but is also calculated in the flexibility to quickly access specialized care when we need it the most.

I have experienced numerous situations in my 41 years as a Medicare specialist in which a patient requiring specialized care had limited options because of the limitations offered by a "free" Medicare Advantage plan.

I have never had a Medicare supplement client covered by original Medicare denied access to a specialist.

Finally, agents underscored the importance of informed decision-making. The best Medicare Advantage plan is not necessarily the one with the flashiest benefits or lowest premium. It’s the one that fits an individual’s health needs, budget, location, and expectations. Reviewing the Summary of Benefits and consulting with an experienced professional can make the difference between a good decision and an expensive surprise.

So, is “free” just clever marketing? Based on these insights: yes. While Medicare Advantage plans can offer value, they should never be mistaken for a no-cost solution. The costs are real—just sometimes hidden behind the promise of zero-dollar premiums.