How Annuities Play a Role in Medicare Planning

-

July 30, 2025

When preparing for retirement, many people focus on Social Security, 401(k)s, and IRAs. There's another financial tool that plays a growing role in the conversation: annuities. While annuities are not part of Medicare itself and don't affect your eligibility to enroll, they can have a direct impact on what you pay for your Medicare coverage, especially when it comes to premiums, out-of-pocket costs, and how you qualify for related programs like Medicaid.

Understanding how annuities interact with Medicare can help retirees make smarter financial decisions and avoid unexpected costs.

What Are Annuities?

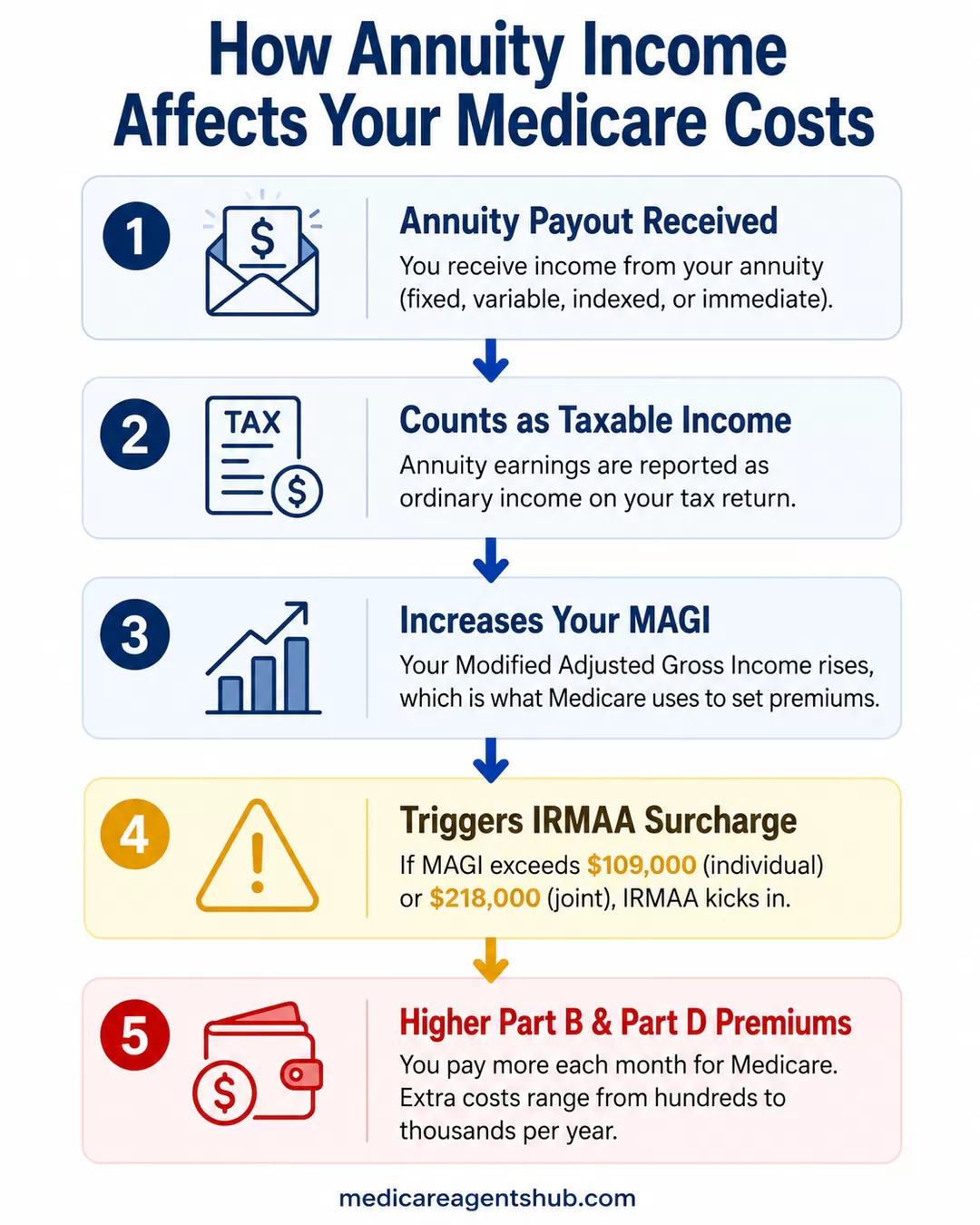

An annuity is a financial product sold by insurance companies. It provides a stream of income, either for a set period or for life, in exchange for a lump sum or a series of payments. Annuities are often used to create a predictable source of income in retirement.

There are different types of annuities; fixed, variable, indexed, and immediate, each with its own rules and benefits. Some annuities allow your money to grow tax-deferred, while others are designed to start paying out income immediately.

What role do annuities play in retirement planning?

In our practice, we view annuities as serving three primary roles in retirement planning: storage, growth, and income. All three can be accomplished using fixed annuities, depending on the client’s needs and stage of retirement.In the storage role, funds are placed into a fixed annuity that earns a predetermined rate of interest. These products are often used as a conservative alternative to traditional savings vehicles. In many cases, the interest rate can exceed what is typically available through bank CDs or bonds, while also providing principal protection. Many annuity contracts also allow for limited withdrawals each year, giving retirees access to funds if needed.

A growth annuity—often a Fixed Indexed Annuity (FIA)—offers the potential for market-linked returns while protecting the principal. These products are tied to a market index, allowing the account to participate in a portion of market gains. However, because they are designed with downside protection, the contract owner will not lose principal due to market declines. This makes them appealing to individuals who want growth potential but are uncomfortable with market risk.

The third role is income. Income annuities are designed to provide guaranteed lifetime income, often covering both spouses. Because the income cannot be outlived, they are sometimes referred to as a personal pension plan. For many retirees, this creates a dependable monthly deposit similar to Social Security. This strategy can be especially valuable for individuals who are concerned about running out of money or who want a predictable income stream to cover essential living expenses.

When used appropriately, annuities can help address several key retirement risks—market volatility, longevity risk, and income stability. By structuring annuities around storage, growth, and income, retirees can create a balanced strategy that protects assets, allows for potential growth, and most importantly provides reliable income.

Medicare and Annuities: Separate Products That Still Interact

Medicare, the federal health insurance program for people 65 and older (and some younger individuals with disabilities), does not offer or manage annuities. However, the income you receive from annuities can directly affect your Medicare costs.

Most notably, annuity income can increase your Modified Adjusted Gross Income (MAGI), which the government uses to determine how much you'll pay for Medicare Part B and Part D premiums.

How Annuity Income Affects Medicare Premiums

Medicare premiums aren't the same for everyone. If your income is above a certain level, you'll be required to pay more through something called the Income-Related Monthly Adjustment Amount (IRMAA).

Here's how it works:

-

The Social Security Administration looks at your tax return from two years prior to determine your current year's Medicare premiums.

-

If your MAGI is above $109,000 for individuals or $218,000 for couples filing jointly in 2026, you'll pay a higher monthly premium for Medicare Part B (doctor visits, outpatient care) and Part D (prescription drugs). The standard Part B premium for 2026 is $202.90 per month.

-

Annuity payouts, depending on the structure, may count as ordinary income and be included in your MAGI.

This means that a person receiving income from a non-qualified annuity could inadvertently cross into a higher IRMAA bracket and face additional Medicare costs. These extra costs can range from a few hundred to a few thousand dollars per year. If you've experienced a life change that caused a temporary income spike, you may be able to appeal the IRMAA surcharge with help from a Medicare advisor.

My income fluctuates significantly year to year from investment distributions. How can I avoid IRMAA surcharges when I have an unusually high-income year?

income spikes from investments can definitely trigger IRMAA if we’re not planning ahead.Since Medicare premiums are based on income from two years prior, what I typically recommend is proactive tax planning. If the high-income year was a one-time event, we can file an appeal with the Social Security Administration to request a reduction.

We also look at strategies like spreading out distributions, managing capital gains, and timing Roth conversions carefully so you stay below the IRMAA thresholds whenever possible.

It really comes down to planning ahead so a temporary income spike doesn’t increase your Medicare premiums unnecessarily.

Using Annuities to Plan for Medicare Costs

Despite the potential downside of increasing your Medicare premiums, annuities can still serve as a valuable tool for covering healthcare expenses in retirement. Many retirees rely on the steady, predictable income from annuities to manage the recurring costs associated with Medicare. This includes monthly premiums for Part B and Part D, Medigap plan premiums, and regular out-of-pocket expenses like deductibles and copays.

For individuals who lack a pension or are concerned about market fluctuations affecting their retirement savings, annuities can provide peace of mind by ensuring that healthcare costs are met consistently. Some people also use this income to help pay for services not covered by Original Medicare, such as dental, vision, and hearing care.

To get the most benefit, it's important to carefully consider the timing and structure of annuity payouts. If payments begin during the period used to calculate IRMAA surcharges, they could push your income over the threshold and trigger higher premiums. You can also explore smart tax planning strategies to lower your Medicare costs. Working with a financial advisor can help align your annuity strategy with your Medicare planning, potentially minimizing tax implications and avoiding unexpected costs.

How can I lower my Medicare Part B premium if my income drops after retirement?

If your income drops after retirement, you may be able to lower your Medicare Part B premium by requesting a review of your income. Medicare uses a prior tax year to set premiums, so if your current income is lower due to a qualifying life event—like retirement—you can file an appeal using Form SSA-44 with the Social Security Administration.If approved, your premium can be adjusted to reflect your current, lower income instead of your past earnings, which can significantly reduce what you pay each month.

Should You Use Annuities in Your Medicare Plan?

Whether annuities make sense in your Medicare planning depends on several personal factors:

-

Your current and expected income levels

-

Your health status and likelihood of needing long-term care

-

Your tax situation

-

Whether you plan to enroll in Medicaid later in life

For some, annuities offer peace of mind and predictable income that can comfortably cover Medicare-related expenses. For others, they may trigger unintended costs, particularly through higher premiums. The key is understanding why Medicare should be part of your broader retirement strategy so you can weigh these trade-offs before committing.

A note on Medicaid planning: If you think you may need Medicaid coverage down the road, talk with an elder law attorney or a Medicaid planning specialist before purchasing an annuity. Medicaid's treatment of annuities is complex, highly state-specific, and only certain Medicaid-compliant annuities avoid being counted as assets.

Balance is Key

Annuities can be a helpful financial tool in retirement, but only if used strategically. Their role in Medicare planning is mostly indirect but significant. While they don't provide healthcare coverage themselves, annuities can affect what you pay for that coverage and how you qualify for related programs like Medicaid.

If you're nearing retirement or already enrolled in Medicare, it's worth speaking to a qualified financial advisor and licensed Medicare broker who understands Medicare rules and how annuity income is treated for tax and premium purposes. With proper planning, annuities can complement your Medicare strategy and help you manage healthcare expenses throughout retirement.