Medicare Annual Enrollment Period (AEP): Dates, Rules, and What You Can Change

: Dates, Rules, and What You Can Change")

-

August 7, 2025

Written by Robert Vaughan, R.Ph., MBA

Medicare Broker Licensed in CA, AZ, ID, NM, NV & TX

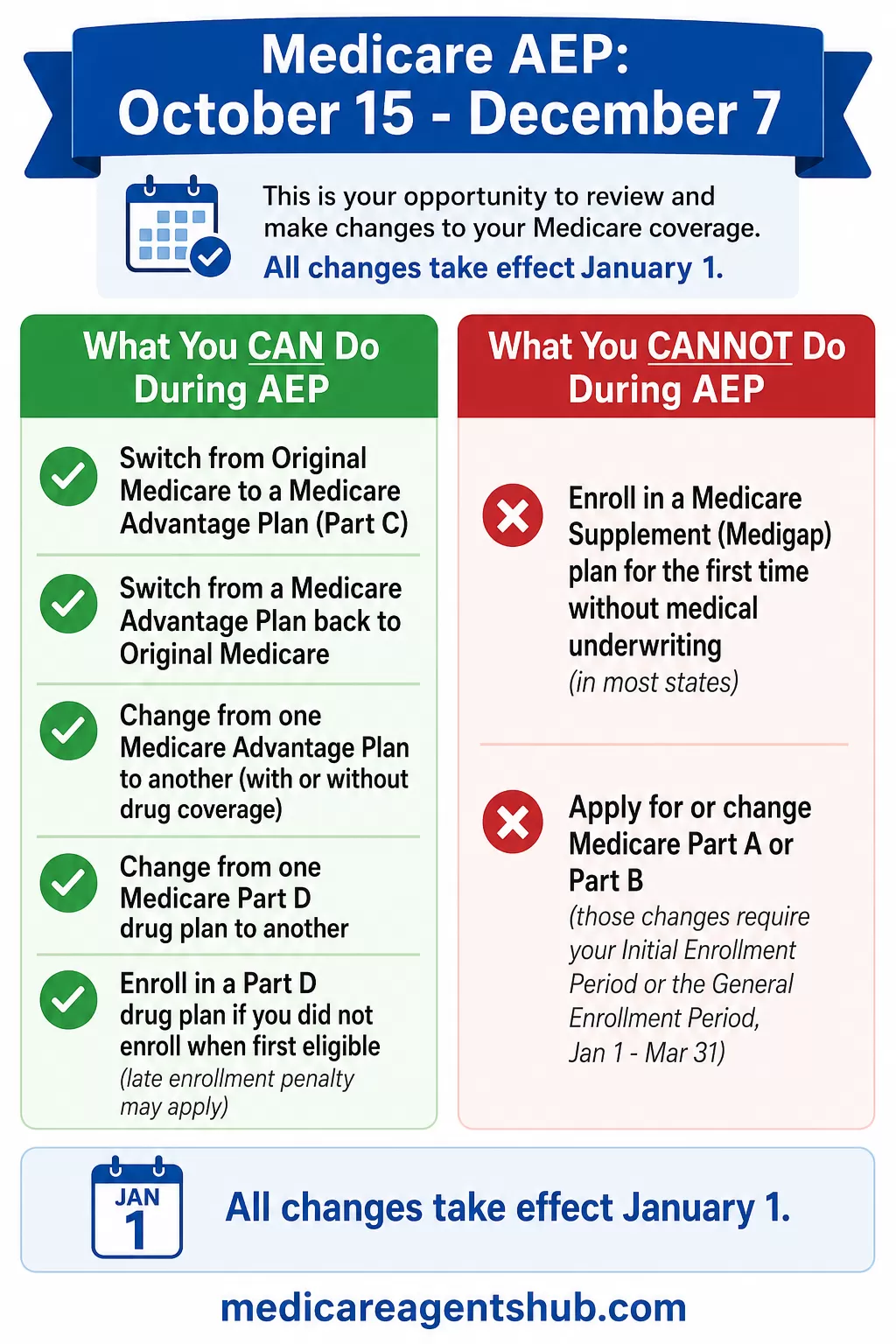

Every year, Medicare beneficiaries can review and make changes to their Medicare coverage during the Annual Enrollment Period (AEP), which runs from October 15 through December 7. This is a critical time to assess your current coverage, understand any upcoming changes to your plan, and work with a Medicare advisor to decide whether a different plan might better suit your needs.

What Is the Medicare Annual Enrollment Period (AEP)?

The Annual Enrollment Period, often referred to as AEP or the Medicare Open Enrollment Period, is a designated timeframe during which individuals with Medicare can make certain changes to their health and drug plans. The changes you make during this time will take effect on January 1 of the following year.

What You Can Change During AEP (October 15 to December 7)

During the Annual Enrollment Period, Medicare beneficiaries have several options:

- Switch from Original Medicare to a Medicare Advantage Plan (Part C):

If you have Original Medicare (Part A and Part B), you can choose to enroll in a Medicare Advantage plan, which often includes additional benefits like vision, dental, hearing, and prescription drug coverage. - Switch from a Medicare Advantage Plan back to Original Medicare:

You can drop your Medicare Advantage plan and return to Original Medicare. If you do this, you may also enroll in a stand-alone Medicare Part D plan for prescription drugs and may want to consider a Medicare Supplement (Medigap) plan—though acceptance into a Medigap plan may be subject to medical underwriting in most states. - Change from one Medicare Advantage Plan to another:

This includes switching from a plan with drug coverage to one without, or vice versa. If you feel like you chose the wrong Medicare plan during AEP, this is also your window to correct course. - Change from one Medicare Part D prescription drug plan to another:

If you have Original Medicare and a stand-alone Part D plan, you can change to a different Part D plan that may offer lower premiums, a better formulary, or improved pharmacy networks. - Enroll in a Medicare Part D prescription drug plan if you did not enroll when first eligible:

(Note: A late enrollment penalty may apply if you did not have creditable drug coverage.)

What is the main benefit of Medicare Part D?

Medicare does not provide any prescription coverage. It is extremely important that you have either a stand-alone Part D prescription plan or drug coverage included in your Medicare Advantage Plan when you make the transition into Medicare. Even if you are not currently taking medicines, you are required to have creditable Part D coverage or you could start accruing a lifelong penalty.What You Cannot Do During AEP

While AEP provides many options, there are limitations:

- You cannot enroll in a Medicare Supplement (Medigap) plan for the first time without going through medical underwriting (in most states). The best time to enroll in a Medigap plan without health questions is during your Medigap Open Enrollment Period, which begins when you are 65 or older and enrolled in Medicare Part B and last for six (6) months from your Part B effective date.

- You cannot apply for or change your Medicare Part A or Part B during AEP. Changes to Original Medicare must be done during your Initial Enrollment Period (when you first become eligible) or during the General Enrollment Period (January 1–March 31) if you missed your initial opportunity.

Why the Annual Notice of Change (ANOC) Letter Matters

Before AEP begins, your current Medicare Advantage or Part D plan will send you an Annual Notice of Change (ANOC) letter, typically by September 30. This document outlines any changes to your plan that will go into effect on January 1, including:

- Monthly premiums

- Deductibles

- Co-pays or coinsurance

- Drug formularies (the list of covered medications)

- Pharmacy networks

- Extra benefits (vision, hearing, fitness programs, etc.)

It is essential to review this letter carefully. Even if you are satisfied with your current coverage, plan changes could mean higher costs or reduced benefits. The ANOC helps you determine whether your plan will still meet your needs in the coming year.

For example, if your medication is removed from your plan’s formulary or a preferred pharmacy is no longer in-network, it could significantly impact your out-of-pocket costs. Being informed allows you to make timely changes during AEP to avoid surprises in January.

Tips for Preparing for the December 7 AEP Deadline

- Review Your Current Coverage:

Look at your plan’s premiums, benefits, provider network, and out-of-pocket costs. - Compare Available Plans in Your Area:

Use the Medicare Plan Finder at Medicare.gov or consult with a licensed independent Medicare health insurance broker to compare plans based on your medications, providers, and personal preferences. - Act Early:

Do not wait until the last minute. Give yourself time to make thoughtful decisions and ensure you meet the December 7 deadline. - Seek Help If Needed:

Medicare is complex, and it is okay to ask for help. Independent Medicare brokers, State Health Insurance Assistance Programs (SHIP), and Medicare.gov are great resources.

Final Thoughts

The Medicare Annual Enrollment Period is your yearly opportunity to take control of your health coverage. By understanding what changes you can make and carefully reviewing your Annual Notice of Change (ANOC) letter, you can ensure your coverage continues to meet your health and financial needs in the upcoming year.

If you do not have an independent Medicare broker working for you, the Annual Enrollment Period (AEP) is a wonderful opportunity to start working with one. Remember, the consultation is FREE, and you will NOT pay higher premiums if you collaborate with a broker. Independent Medicare brokers work for you, NOT the insurance companies!

Being proactive during AEP can save you money, improve your access to care, and give you peace of mind knowing you are enrolled in a plan that is right for your specific needs. And if you do miss the AEP deadline, don't panic—learn about what you can still change during Medicare Advantage Open Enrollment.

About the Author: Robert Vaughan is a Medicare Health Plan specialist licensed in CA, NV, AZ, NM, and TX with over 35 years of healthcare and insurance experience. He is the founder of Robert Vaughan Insurance Solutions based in Oakdale, CA.