Understanding Medicare Choices at Age 65

As a Medicare agent, one of the most common questions I get is “I’m turning 65, do I have to enroll in Medicare?” And the answer is: Yes, No and Maybe.

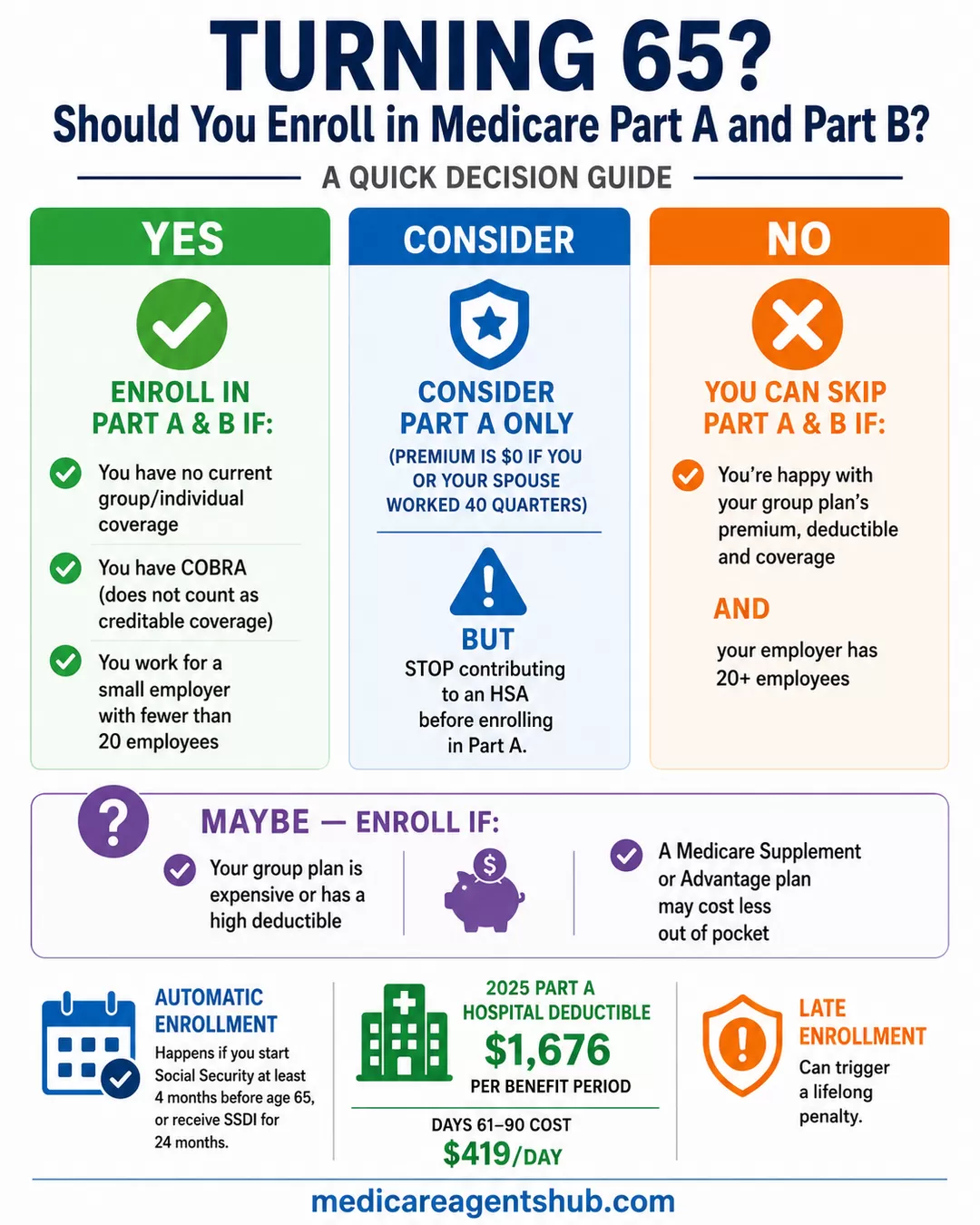

Do I Have to Enroll in Medicare at 65?

Yes

If you don’t have any current group or individual health insurance, you should sign up for both Part A (Hospital Insurance) and Part B (Medical Insurance) when you are first eligible, usually at age 65. If you sign up later, you may have to pay a penalty. You should also sign up for A and B if you have COBRA coverage when you turn 65. COBRA doesn’t extend the length of time you have to sign up for Medicare, and it isn’t considered Creditable Coverage.

You should also consider signing up at age 65 if you work for a small employer with less than 20 employees on the payroll. Check with your HR department to see how your health plan coordinates with Medicare, they may require you to drop the group plan and make Medicare your primary coverage.

You could also consider just signing up for Part A only when you turn 65. If you or your spouse have worked 40 quarters, your premium for Part A is $0. This could lower your out of pocket costs if you are hospitalized or need extensive skilled nursing care, as Medicare will pay second to your group plan in group of 20 or more employees.

The deductible for a hospital stay in 2026 is $1,736 per benefit period. (A benefit period starts at the time you are admitted to inpatient hospital care and ends when you have not received any inpatient care for at least 60 days. You could have several benefit periods during a calendar year.) Part A covers the first 60 inpatient days during a benefits period, and then pays all but a daily copayment of $434 from days 61-90.

BUT, if you have a HSA (Health Savings Account, not the same as a Flex Spending Account) you must stop contributing to the account prior to enrolling in Medicare A.

You are automatically enrolled in Medicare if you begin receiving Social Security benefits at least four months before you turn 65, or if you receive Social Security disability benefits for at least 24 months.

No

You don’t have to sign up for Part A and B when you turn 65 if you are happy with the premium, deductible and coverage of your group plan. If you work for a company with 20 or more employees on the payroll, Medicare is usually optional. Employees often have younger spouses or dependents who would lose coverage if they dropped their group plan, so this is another consideration.

Maybe

You should sign up for Part A and Part B when you turn 65 if your group plan is expensive or has a high deductible, and paying the Part B premium might be cheaper. When combined with a Supplement or Advantage plan, medical out of pocket costs are sometimes significantly lower than a group plan.

A licensed, local agent can evaluate your situation and help you make the right decision.

What benefits are there to working with a Medicare Agent near me vs remote/virtual?

A local agent knows which policies are a good fit for your local area. Sometimes people want a Supplement plan that includes wellness benefits such as a gym membership, and an agent will be aware of which policies cover popular local facilities. A local agent will also keep in touch with you prior to annual enrollment to see if there are any changes that need to be made on your policy. An agent might also help you with setting up an online Social Security account, with applying for Medicare A and/or B, and setting up Medicare billing. Best of all, it costs nothing for you to work with a local Medicare agent!What Medicare DOESN’T Cover

So once you’ve made the decision to make Medicare your primary health care provider, you need to know what it does and doesn’t cover. For most people, Medicare combined with a Supplement, Prescription Drug Plan or an Advantage plan covers almost everything they need. However, there are some notable things Medicare does NOT cover.

Routine Physical Exams

This is probably the biggest surprise for someone coming off a group plan. Medicare does not cover routine physical exams like you are used to. The first year on Medicare you should have a “Welcome to Medicare exam,” where your doctor will discuss the various tests you can have. After that you can have a free “Annual Wellness Visit”, which is not a comprehensive physical, but will include lifestyle factor interviews and assessments, a fall risk evaluation, height, weight and blood pressure measurements, screening for dementia and depression and a medical and family history update.

Lab Work

This is another area that can cause an unexpected bill, when your doctor sends you to the lab for blood work to run a variety of tests “just to see”. Medicare will pay for medically necessary tests, so if your doctor is concerned about your cholesterol or your Vitamin D level, those tests are covered.

Eye Exams

Original Medicare doesn’t cover eye exams for prescribing, fitting or changing eyeglasses. However, a visit to an Ophthalmologist is considered a specialty doctor visit, whereas a visit to an Optometrist will not be covered.

Long Term Care

There is coverage for skilled nursing care under Medicare Part A, but Medicare does not cover nursing home care, custodial care when it’s the only type of care needed, or non-medical long-term care. However, Medicare does cover some home health and skilled nursing facility care after a hospital stay. You might qualify for long-term care through Medicaid, or you can purchase private long-term care insurance. There are also some annuities that provide payment for long-term care without having to medically qualify.

Concierge Care

Medicare doesn’t cover membership fees for concierge care, also called retainer-based medicine or boutique medicine, where you pay a membership fee to be accepted into the practice.

Weight Loss Drugs

Medicare is barred from paying for weight loss drugs, unless they’re used to treat conditions like diabetes or to manage an increased risk of heart disease. However, there are proposals to expand Medicare and Medicaid coverage for obesity drugs as treatment for a “chronic disease” rather than as weight loss medications.

Common Extra Benefits in Advantage Plans

Chiropractic (Medicare does not cover “maintenance therapy”, but will cover certain services to treat headaches, back and neck pain and sciatica. They will also not cover other services or tests that a chiropractor may order, such as X-rays, massage therapy and acupuncture.)

Other services not covered by Medicare include:

- Cosmetic Surgery

- Massage Therapy

- Care Outside the US

- Non-Emergency Transportation

- Fertility Drugs

- Hair Growth Drugs

- Erectile Dysfunction Drugs

You can learn what medical procedures Medicare will cover by going to Medicare.gov/coverage or checking the Medicare and You handbook.

Are Medicare Advantage plans really "free," or is that just clever marketing?

Many Medicare Advantage plans have $0 premium. It is helpful to have a local agent who can explain the differences in the various policies and their premiums.Michelle Schaefer is a local insurance agent specializing in helping people make decisions about their Medicare plans. She is a resident of Edmond, OK with 30 years of insurance experience AND a card-carrying Medicare client.