Why High-Income Retirees Are Opting Out of Medicare Advantage Plans

-

Last Updated July 23, 2026

Medicare Advantage plans have experienced explosive growth over the past decade, with more than half of all Medicare beneficiaries now enrolled in one. These plans are widely promoted for their low premiums, bundled benefits, and added perks like dental, vision, and fitness coverage. Despite their growing popularity, there's a noticeable trend among high-income retirees: many are intentionally avoiding Medicare Advantage and sticking with Original Medicare combined with a Medigap supplement.

This may seem counterintuitive at first. Why wouldn’t someone with the means to choose any plan go with the one that appears to offer more benefits at a lower monthly cost? The answer, as it turns out, comes down to control, flexibility, and a desire to avoid limitations or surprise costs in the future.

Unrestricted Access to Healthcare Providers

One of the most common reasons high-income retirees avoid Medicare Advantage is the limitation on provider choice. Most MA plans operate within a managed care model (either as HMOs or PPOs) which means members must use a specific network of doctors and hospitals to receive full benefits. For someone who’s used to choosing their own specialists or going to top-tier hospitals, these networks can feel restrictive.

Original Medicare, on the other hand, allows beneficiaries to see any doctor or specialist in the country who accepts Medicare. There are no referrals required, and no concerns about whether a hospital is “in-network.” For affluent retirees who place a premium on provider freedom, that flexibility is a decisive factor.

What's the trade-off between a Medicare Advantage PPO and HMO when it comes to flexibility?

An HMO limits your services to a closed network of physicians and caregivers. HMOs require members to choose one of their in-network primary care physicians to manage your healthcare, and require a referral approval to use other in-network services. HMOs generally do not allow any out-of-network services unless it's an emergency.PPOs are more flexible with their network of services and do not necessarily require a primary caregiver. You can use services outside of their network of treatment services, and you will still be covered. However, PPOs generally have higher prices, deductibles, copays, and coinsurance when you use services outside of their network.

The Travel and Dual-State Lifestyle

Another key consideration is mobility. High-income retirees often split their time between two or more residences or travel extensively throughout the year. Medicare Advantage plans are typically regional, meaning that the benefits and provider networks are tied to a specific service area. While emergency care is usually covered anywhere, routine services, follow-up visits, and specialist access may be limited or require jumping through administrative hoops when outside the home region.

In contrast, Original Medicare paired with a Medigap plan works seamlessly across state lines. Retirees who spend winters in Florida and summers in New York, or take extended trips abroad, tend to prefer a coverage model that won’t interrupt their care due to geography. This kind of nationwide portability is another major reason many well-off retirees stay clear of Advantage plans.

Delays and Prior Authorizations

An increasingly visible drawback of Medicare Advantage is the growing use of prior authorization requirements. These are insurer-imposed rules that force enrollees to get approval before certain tests, procedures, or treatments will be covered. While this is often positioned as a cost-control measure, it can also lead to significant delays in care.

For someone who’s used to concierge-level service or who wants to begin treatment without bureaucratic barriers, these delays can be frustrating. Wealthier retirees often report preferring a system that allows them and their doctors to make decisions directly, without insurer intervention. With Original Medicare and Medigap, there’s no need to wait on prior authorization for most services.

Willingness to Pay for Peace of Mind

Perhaps most important of all is predictability. Medicare Advantage plans, while often inexpensive up front, come with cost-sharing that can add up quickly in a serious medical situation. Copays for hospital stays, diagnostic imaging, and outpatient surgeries can stack into the thousands, and most MA plans carry out-of-pocket maximums that now approach or exceed $9,000 annually for in-network care.

In contrast, Medigap plans, especially Plans G and N, significantly reduce or eliminate these out-of-pocket expenses. Although these plans carry a higher monthly premium, they often result in less financial uncertainty. For high-income retirees, the value isn’t in paying less each month, it’s in knowing they won’t face a large unexpected bill during a major health event.

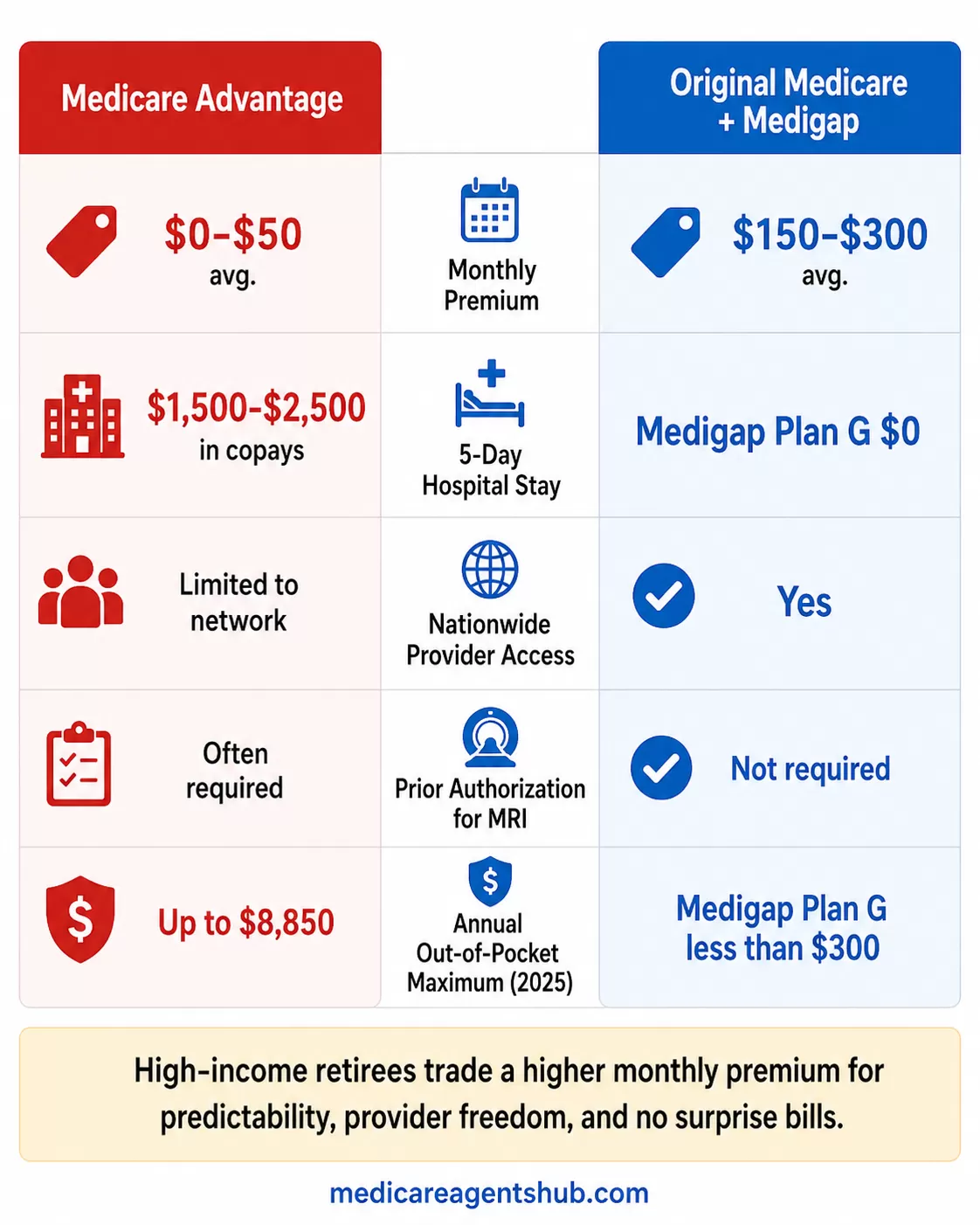

To illustrate this difference, consider the simple comparison below:

|

Scenario |

Medicare Advantage (MA) |

Original Medicare + Medigap |

|

Monthly Premium |

$0–$50 (avg.) |

$150–$300 (avg.) |

|

Hospital Stay (5 days) |

$1,500–$2,500 in copays |

$0 with Plan G |

|

Nationwide Provider Access |

Limited to network |

Yes |

|

Prior Authorization for MRI |

Often required |

Not required |

|

Annual Out-of-Pocket Maximum |

Approaches $9,000+ (in-network) |

Less than $300 (Plan G) |

While the chart above is a simplified view, it reflects the cost trade-offs many retirees are weighing. Those with limited means may tolerate a higher out-of-pocket risk to save on premiums. But for those with financial flexibility, eliminating risk is often worth the monthly cost.

Preferred Access to Specialists and Hospitals

Some of the nation’s most sought-after healthcare providers, including renowned cancer centers, heart hospitals, and university systems, do not accept Medicare Advantage plans or only work with a select few. Participation varies plan by plan, so it’s worth confirming with both the insurer and the hospital’s billing office before enrolling. This can be a serious limitation for retirees who want the freedom to seek top-tier care without being told their plan won’t cover it.

Original Medicare is almost universally accepted among U.S. healthcare providers. When paired with a Medigap plan, patients can usually get care anywhere they choose. For those who have spent decades building wealth and prioritizing high-quality care, being told they “can’t go” to a specific provider due to plan restrictions is a non-starter.

A Decision Made with Expert Guidance

Finally, many high-income retirees make their Medicare decisions with the help of financial advisors or dedicated Medicare brokers. These professionals take a holistic view of long-term care costs, estate planning, and lifestyle expectations. Platforms like MedicareAgentsHub.com offer tools and connections to experienced agents who understand these complex needs and can help guide clients toward plans that prioritize access, flexibility, and predictability over short-term savings.

Whether a retiree is looking to ensure seamless care across multiple states or wants to avoid the uncertainty of a $7,000 bill during a medical emergency, the Original Medicare + Medigap route is often the answer.

Choosing Peace of Mind Over Managed Care

Medicare Advantage plans continue to serve a growing population well, especially those looking for affordability and simplicity. For high-income retirees who have different priorities when it comes to healthcare, these plans often feel too restrictive. They’d rather pay more upfront to get peace of mind, fewer limitations, and the ability to seek care where and when they want. For those already enrolled in Advantage and considering a change, understanding the process of switching back to Original Medicare — including the Medigap underwriting trap, where insurers in most states can deny coverage or charge higher rates based on your health once your initial enrollment window closes — is a critical first step.

If you're exploring your options or advising clients on theirs, resources like MedicareAgentsHub.com can be an invaluable starting point for navigating these decisions with confidence.