The Best Way to Apply for Medicare with a Plan G Supplement

-

Last Updated July 22, 2026

Written by Charise Karjala

Medicare Broker Licensed in CA, AZ, CO, PA & WA

Are you turning 65 or getting ready to retire? Navigating Medicare can feel overwhelming at first, but don’t worry, you’re not alone. One of the most important decisions you’ll make is choosing the right supplemental coverage, and Medigap Plan G has quickly become the top choice for many.

In this post, we’ll walk you through how to apply for Medicare with a Plan G supplement, why Plan G is considered the most comprehensive Medigap option, and why it’s especially valuable if you get care at private hospitals like Eisenhower Health, Cedars-Sinai, or Hoag.

First, What’s a Medigap Plan?

Original Medicare (Parts A and B) covers a lot, but not everything. There are gaps like deductibles, coinsurance, and copayments that you’re responsible for. That’s where Medigap (Medicare Supplement Insurance) comes in.

Medigap plans are offered by private insurance companies and labeled with letters: Plan A, B, G, N, etc. Each plan letter offers the same benefits, no matter which company sells it. The difference? Premiums, service, and company perks.

Why Plan G Is the Star of the Show

If you’re newly eligible for Medicare, Plan G is the most comprehensive Medigap plan available. See also our guide to the pros and cons of Medicare Supplement insurance. It covers almost every out-of-pocket cost Original Medicare doesn’t, including:

✅ Medicare Part A deductible

✅ Part B coinsurance and copayments

✅ Part B excess charges

✅ Skilled nursing facility coinsurance

✅ Blood (first 3 pints)

✅ Foreign travel emergency coverage

✅ And more!

The only thing it doesn’t cover is the annual Part B deductible (the amount is set each year by CMS — see the current figure on Medicare.gov). After that’s paid, Plan G covers the rest, 100%.

Which Medicare Supplement plan (Medigap) offers the best value for most seniors, and why?

Part B Excess Charges: Why They Matter

Now here’s where Plan G really shines: Part B excess charges.

Not all doctors accept Medicare’s "approved amount" for services. Some can legally charge up to 15% more. That extra cost is known as a Part B excess charge, and it’s NOT covered by Original Medicare or many Medigap plans (like Plan N, for example).

If you plan to visit private hospitals like Eisenhower Health, Cedars-Sinai, or Hoag, you’re more likely to run into these excess charges because many specialists there do not accept Medicare assignment. Without Plan G, you could be stuck with surprise bills.

👉 Plan G covers those excess charges in full, giving you the freedom to see top-tier providers without the fear of unexpected costs.

When to Apply: Don’t Miss This Window

The best time to enroll in Plan G is during your Medigap Open Enrollment Period. That’s a 6-month window that begins the month you’re:

🎂 65 or older, AND

📋 Enrolled in Medicare Part B

During this time, you have guaranteed issue rights, meaning you can get any Medigap plan (including Plan G) with no health questions asked. Insurance companies can’t deny you or charge you more because of health conditions.

If you wait and apply later, you might have to go through medical underwriting. Understanding Medicare enrollment periods is critical, which could lead to higher rates, or even denial of coverage.

I missed my Medigap window by a few months and now no one will cover me without underwriting. Why isn't this rule more well known?

So for those of you coming into Medicare, please don't listen to your friends, because they may or may not have accurate information. Call Medicare, call Social Security, call HICAP. There's an office in your state, or call a broker. Those of us who work with five or more companies, especially the big reputable ones—not the little ones—and who work in multiple states can answer that question quickly and efficiently for you. We can provide guidance, timelines, and budgets to work with. This is one of the most important decisions you will make in your life, and it shouldn't be left to a cocktail party or a poolside conversation.

I'm sorry to hear that this individual missed their Medigap window. If they were my client, I would certainly be looking for options to have a different election period where they might get a chance to move into a Medigap policy. But to miss that is a big miss, and that's unfortunate. The information's out there.

How to Apply for Medicare with a Plan G Supplement

Here’s a simple step-by-step breakdown:

- Enroll in Original Medicare

- You can do this online at SSA.gov, over the phone, or at your local Social Security office.

- Most people are automatically enrolled in Part A, but you’ll need to manually enroll in Part B if you’re not yet drawing Social Security.

- Compare Plan G Options

- Medigap Plan G is the same across all insurers, but prices and perks vary.

- Work with a licensed, independent Medicare agent (like me!) to compare rates from top carriers in your area.

- Choose Your Insurance Company

- Once you find the right plan, you can complete the application online, by phone, or with your agent.

- Some companies offer discounts for couples or electronic payments.

- Pick Your Part D Drug Plan

- Don’t forget: Medigap plans don’t include prescription drug coverage.

- You’ll want to enroll in a standalone Medicare Part D plan to avoid penalties and get help with medication costs.

How do I know if a Medigap policy is right for me, and what's the best time to buy one?

I use an algorithm to determine if the Medicare supplement policy is appropriate for my given client.If you’d like additional assistance with this reliable method of determining whether a Medicare supplemental policy appropriate, please contact me. Charise Karjala

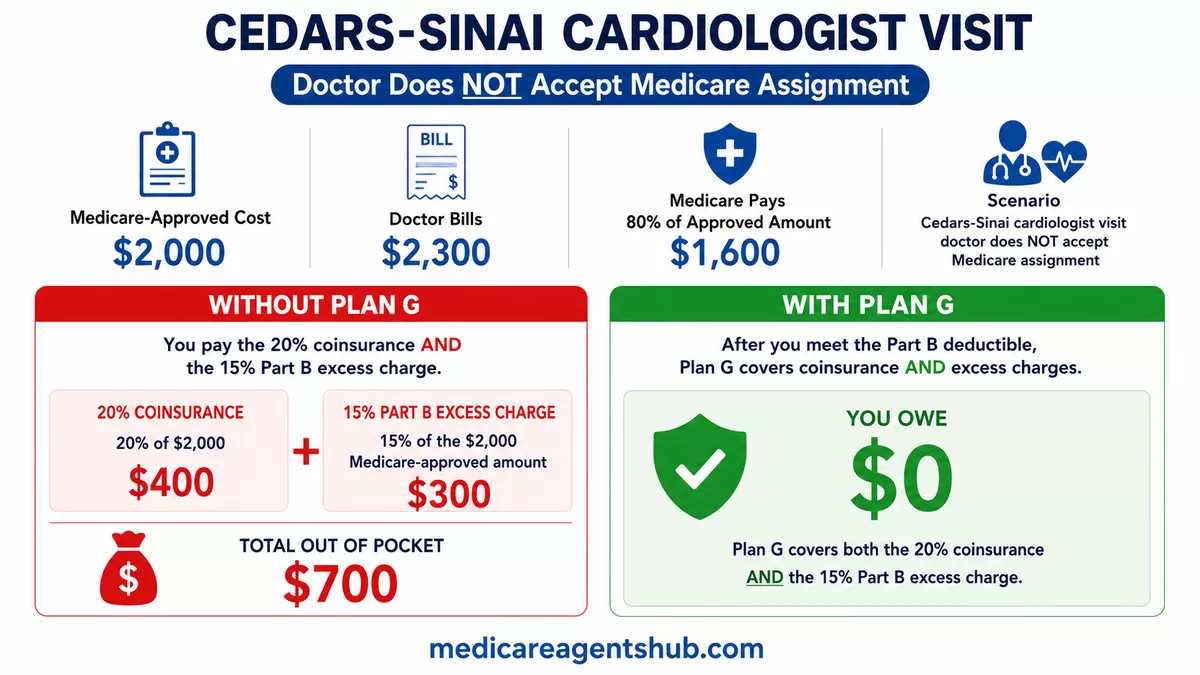

Real-World Example: Visiting Cedars-Sinai Without Plan G

Let’s say you see a top cardiologist at Cedars-Sinai, and they don’t accept Medicare assignment. They perform a procedure with a Medicare-approved cost of $2,000 but bill $2,300.

Medicare covers 80% of the approved amount ($1,600), and without Plan G, you’d be on the hook for:

- The remaining 20% coinsurance: $400

- The excess charge (15%): $300

💸 That’s $700 out of pocket, just for one procedure.

With Plan G, that entire amount (after your Part B deductible is met) would be fully covered.

Bottom Line: Plan G = Peace of Mind

If you want freedom to choose your doctors, confidence that you won’t be hit with surprise bills, and strong protection at high-end hospitals like Eisenhower, Cedars-Sinai, and Hoag, Plan G is hands-down the best Medigap choice. That said, it is not the right fit for everyone. Depending on your health, budget, and how often you see doctors, Plan N, Plan K, or even High-Deductible G might actually save you more.

It’s ideal for:

✅ People who value flexibility

✅ Those with frequent specialist visits

✅ Anyone who wants predictable health care costs in retirement

Ready to Get Started? I Can Help.

Applying for Medicare and choosing the right supplement plan doesn’t have to be confusing. As a licensed, experienced agent, I’ll help you compare your options, enroll on time, and get the maximum value from your Medicare coverage.

📞 Call, email, or schedule a free consultation. Virtual and in-person appointments available.

Need Help with Medicare? Reach out to a licensed independent Medicare agent today to get personalized, unbiased guidance and answers to your most pressing questions. It could be the most valuable healthcare decision you make all year.

About the Author: Charise Karjala is a Medicare broker licensed in CA, AZ, CO, PA and WA with over 13 years of experience.