Medicare Coverage for Skilled Nursing and Rehab: The 100-Day Rule After a Hospital Stay

-

Last Updated July 22, 2026

Medicare can help pay for skilled nursing facility (SNF) care and short-term rehab, but only under specific conditions. Many people assume Medicare will cover long-term nursing home care, but that’s not true. The coverage is limited to 100 days per benefit period, and understanding when it applies and when it doesn’t can save you from unexpected bills worth thousands of dollars.

This article breaks down exactly how Medicare covers skilled nursing and rehab after a hospital stay, who qualifies, how long the coverage lasts, and what costs you can expect.

What Is Skilled Nursing (and Rehab) Care Under Medicare?

Skilled nursing care refers to medically necessary services provided by licensed health professionals, such as registered nurses, physical therapists, or occupational therapists. These services must be ordered by a doctor and are typically required after a hospitalization due to surgery, injury, or a serious illness.

Skilled care includes things like wound treatment, IV therapy, and short-term rehab (physical, occupational, and speech therapy) delivered in a clinical setting. When people search for “rehab after a hospital stay,” this is usually what they’re describing — care in a Medicare-certified skilled nursing facility. This is not the same as custodial care, which includes assistance with daily activities like bathing, eating, or dressing. Custodial care is not covered by Medicare.

What happens to my Medicare coverage if I enter a skilled nursing facility for rehab but then need long-term care?

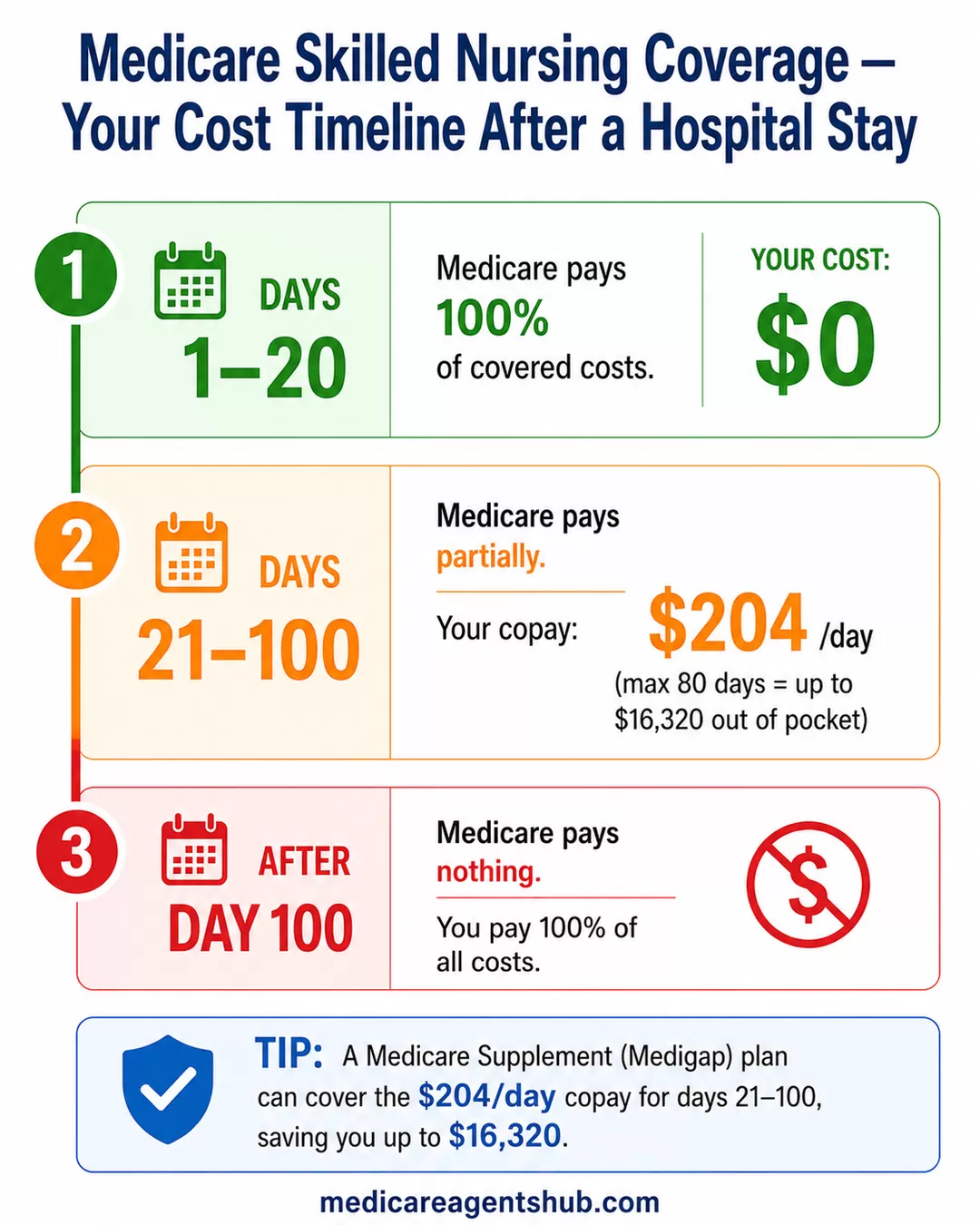

When you enter a skilled nursing facility (SNF) for rehab, Medicare Part A typically covers up to 100 days per benefit period, provided you meet eligibility requirements (e.g., a qualifying 3-day hospital stay, skilled care needs, and admission within 30 days of hospital discharge). Here’s how it breaks down:Days 1–20: Medicare covers the full cost of SNF care (assuming the facility is Medicare-certified and care is medically necessary).

Days 21–100: You pay a daily coinsurance ($204 in 2025), and Medicare covers the rest. Supplemental insurance (like Medigap) may cover this coinsurance.

After 100 days: Medicare Part A stops covering SNF care, regardless of whether you still need rehab or have transitioned to long-term care.

When Medicare Covers Skilled Nursing Facility (SNF) Care

To qualify for Medicare coverage of skilled nursing or rehab care, five conditions must be met (see Medicare.gov’s SNF coverage rules for the official guidance):

1. You Have Medicare Part A

Medicare Part A covers inpatient hospital stays and skilled nursing facility care. You must be enrolled in Part A for coverage to apply.

2. You Had a Qualifying Inpatient Hospital Stay

You must have been admitted as an inpatient for at least three consecutive days (not counting the discharge day). Observation status does not count, even if you stayed overnight in a hospital bed. This distinction trips up a lot of people, so always confirm your admission status with hospital staff before you leave.

I just got Medicare Part A, and I'm worried about hospital stays. How do I know if my overnight stay will be covered fully?

Medicare Part A covers hospital stays only if you are formally admitted as an inpatient, not if you’re under “observation status,” even if you stay overnight. To know if your stay will be covered, ask the hospital staff whether you’re being admitted as an inpatient and for how many days. Even with inpatient coverage, Part A has a deductible per benefit period, so it may not be fully paid unless you have supplemental coverage. A Medigap plan or Medicare Advantage plan can help cover those deductibles and reduce unexpected hospital bills.3. You Enter the SNF Within 30 Days of Hospital Discharge

You need to transfer to the skilled nursing or rehab facility within 30 days after leaving the hospital. In some cases, if it’s medically inappropriate to begin rehab sooner, the timeline can be extended.

4. You Need Skilled Care

Your condition must require daily skilled services that can only be provided in a SNF setting.

5. The Facility Is Medicare-Certified

The SNF must be approved by Medicare, and not all facilities are. You can verify a facility’s certification on Medicare’s Care Compare tool.

How Many Days Does Medicare Pay for Skilled Nursing or Rehab?

When all requirements are met, Medicare Part A will cover the cost of care in a skilled nursing facility. This includes a shared room, meals, skilled nursing services, physical and occupational therapy, speech-language pathology services, medications, and medical supplies needed during the stay.

The coverage does not last indefinitely. Medicare pays the full cost for the first 20 days. From day 21 through day 100, you are responsible for a daily copayment. After 100 days, Medicare coverage ends entirely and you become responsible for all costs. This is what people usually mean when they refer to the Medicare 100-day rule for rehab.

The coverage is time-limited, and is often described as a hidden expense that people don’t think about until it’s too late. Here is the breakdown:

- Days 1–20 — Medicare pays 100%$0 to you

- Days 21–100 — Medicare pays partially$217/day copay

- After Day 100 — Medicare pays $0You pay all costs

Note: These numbers are for Original Medicare in 2026. Medicare Advantage plans may vary.

Do Medicare Days Reset Every Year?

No. Your 100 skilled nursing days do not reset on January 1 or on the anniversary of your enrollment. Medicare hospital and SNF days don’t follow a calendar year. They operate on a benefit period system. A benefit period starts the day you’re admitted as an inpatient and ends after you’ve been out of the hospital or SNF for 60 consecutive days. Once that happens, a new benefit period begins and your coverage days reset — giving you a fresh 100 days of SNF coverage.

A quick note on lifetime reserve days: Medicare’s 60 lifetime reserve days apply to inpatient hospital stays only. They do not extend skilled nursing facility coverage beyond the 100-day limit. Once you hit day 100 in a SNF, you’re responsible for all costs until a new benefit period begins.

Do my Medicare hospital days reset every year?

They reset every benefit period. Medicare benefit periods under part A starts upon becoming an inpatient in the hospital and ends when you have been out of the hospital or skilled nursing facility for 60 days in a row.You also have extra lifetime days to use if you run out of days that Medicare will cover. These 60 lifetime days can only be used one time in your life.

Medicare advantage and Medigap plans are figured differently and provide you with more days.

How a Medicare Supplement Can Help

If you’re on Original Medicare, a Medicare Supplement (Medigap) plan can significantly reduce your skilled nursing costs. Most Medigap plans, including the popular Plan G and Plan N, cover the $217/day coinsurance for days 21 through 100. That’s a potential savings of $17,360 over an 80-day stay in a single benefit period.

Keep in mind that Medigap helps cover the copay within Medicare’s 100-day window. It does not extend SNF coverage past day 100.

Without a supplement, you’re on the hook for the full copay amount each day. For someone recovering from hip replacement surgery or a stroke, an 80-day SNF or rehab stay is not uncommon.

Common Reasons People Lose Coverage

There are several situations that can cause Medicare to stop covering skilled nursing care.

The most common is when a patient’s condition improves enough that daily skilled care is no longer medically necessary. Medicare will determine that continued skilled care isn’t justified and will discontinue payment.

Coverage also ends automatically after 100 days in a benefit period. There is no extension or exception to this limit under Original Medicare.

If a patient voluntarily leaves the facility for an extended period or begins receiving only custodial care, Medicare will stop covering the stay. The same applies if a patient refuses treatment or fails to follow the care plan outlined by their healthcare provider.

If a patient had surgery with more than a 3 day stay in the hospital and needed to recover from the surgery before starting rehab, can the rehab stay be delayed by up to 90 days pending recovery?

Yes with a couple of caveats. Medicare will pay for inpatient rehab in a skilled nursing as long as the rehab stay is preceded by a 3 day stay in a hospital. This is called the "Medicare 3-day rule." And it is true that beginning the rehab stay can be delayed by up to 90 days after the hospital stay, pending recovery from the surgery. However, if the delay is longer than 30 days, it must be medically inappropriate to begin rehab sooner to remain covered. Also, the above rules apply to Original Medicare. If someone is enrolled in a Medicare Advantage plan, they will have to follow the guidelines set forth by their particular plan. Medicare Advantage members are not subject to the 3-day rule, but their plan will still have to approve any inpatient rehab stay based on medical necessity.What About Medicare Advantage Plans?

If you’re enrolled in a Medicare Advantage plan instead of Original Medicare, your skilled nursing facility benefits may look different. Medicare Advantage is required to offer the same core benefits as Original Medicare, but the plan may impose additional rules.

Prior authorization is a big one. Many Advantage plans require approval before entering a facility. Copay amounts and coverage timelines can also differ from the standard Medicare structure. Some MA plans waive the 3-day inpatient rule; others still require a qualifying hospital stay based on their own policies. Always confirm with your specific plan.

Another key difference is provider networks. Medicare Advantage plans often have a limited list of approved skilled nursing facilities, and receiving care outside that network could result in higher costs or denied coverage.

Review your plan details carefully and confirm coverage with your insurer before a skilled nursing admission, not after.

Tips to Protect Yourself

-

Get documentation: Ensure your hospital stay qualifies as "inpatient" and not just "under observation." Ask the hospital staff directly about your admission status.

-

Ask the facility: Confirm the nursing facility is Medicare-certified before you transfer.

-

Track your days: Keep count of how many days you’ve used in a benefit period so you’re not surprised by the copay kicking in on day 21.

-

Consider a supplement: A Medigap plan can cover the SNF copay gap and protect you from large out-of-pocket costs.

-

Talk to an agent: A licensed Medicare advisor can help you understand your coverage or compare Medigap options to reduce costs.

Final Thoughts

Medicare does provide skilled nursing and short-term rehab coverage, but only under narrow conditions and for a limited time — up to 100 days per benefit period. Understanding the rules before you need the care makes all the difference. If you’re unsure about your eligibility or want to compare plans that offer better post-hospital coverage, consider speaking with a licensed Medicare agent who can walk you through your options.