Appealing IRMAA Premium Increases? Here’s How a Medicare Advisor Can Help

-

August 14, 2025

For many Medicare beneficiaries, the annual premium bill can be an unpleasant surprise. This is especially true for those subject to the Income-Related Monthly Adjustment Amount (IRMAA), an extra surcharge applied to Medicare Part B and Part D premiums for higher-income individuals. While IRMAA is based on your income from two years prior, life doesn’t always move in a straight line; retirement, job loss, or other life changes can cause your income to drop dramatically. When that happens, you have the right to appeal and request a lower premium.

Appealing an IRMAA adjustment can be a straightforward process if you know what to do. However, for many people, it’s confusing, time-consuming, and stressful. That’s where the guidance of a knowledgeable Medicare advisor (sometimes called a Medicare broker or Medicare agent) can make a real difference.

Understanding IRMAA and Why Premiums Increase

IRMAA is a surcharge added to Medicare premiums if your income exceeds a set threshold. The Social Security Administration (SSA) determines this based on your modified adjusted gross income (MAGI) from your IRS tax return two years earlier.

For example, if you’re paying Medicare premiums in 2026, your IRMAA calculation is based on your 2024 income. If that 2024 income was unusually high (perhaps due to a one-time event like selling property, taking large retirement account withdrawals, or cashing in investments) you could find yourself paying hundreds of dollars more each month, even if your current income is much lower.

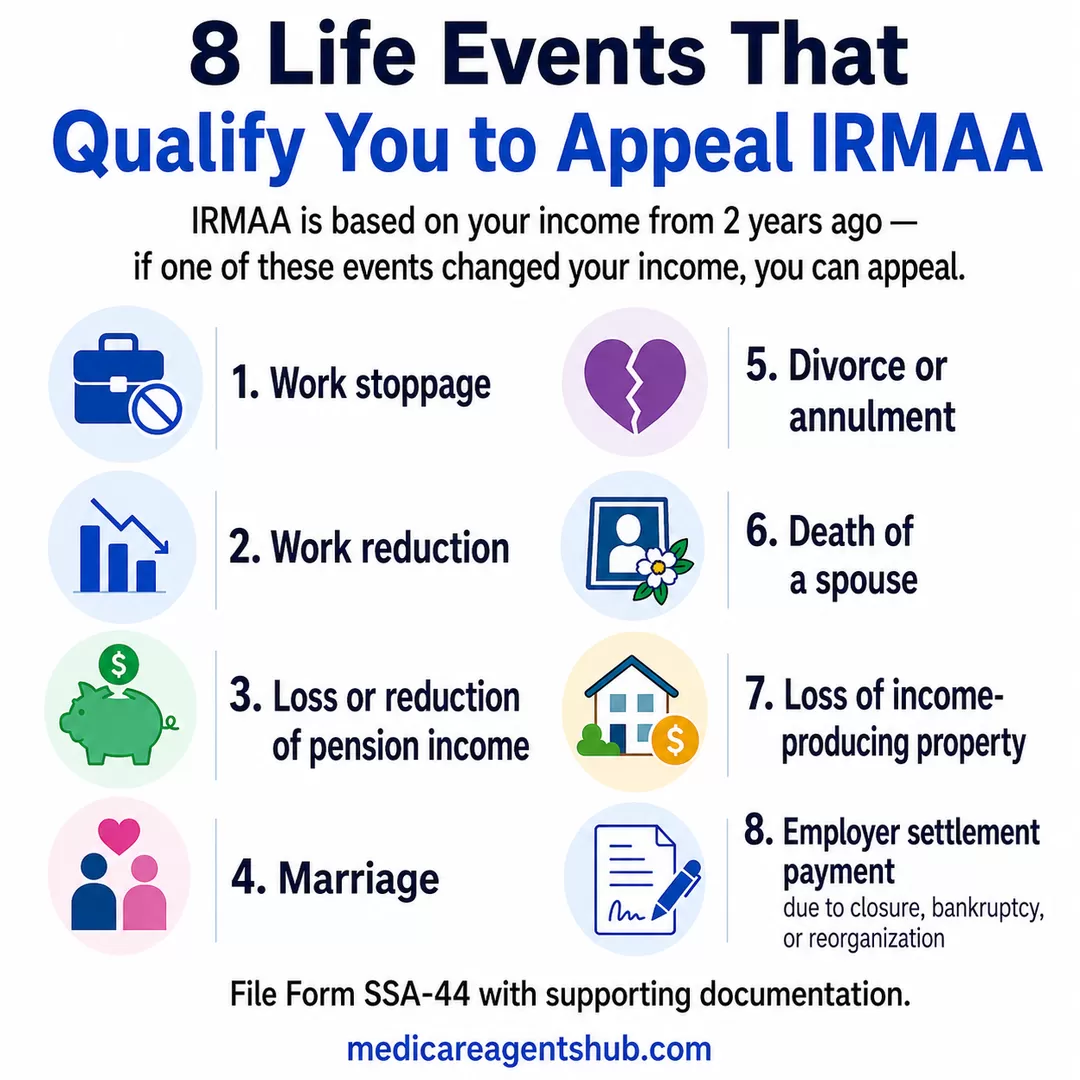

When You Can Appeal IRMAA

You can’t appeal simply because you don’t like the surcharge amount. The SSA allows IRMAA appeals if you’ve experienced specific “life-changing events” that reduce your income. These can include:

-

Retirement or reduction in work hours

-

Loss of a pension

-

Divorce or annulment

-

Death of a spouse

-

Loss of income from property

-

Certain types of settlement payments

Marriage is another life event that can unexpectedly affect your IRMAA — particularly getting married later in life, when combined household income may push you into a higher surcharge bracket even if neither spouse’s income changed individually.

To appeal, you’ll typically file Form SSA-44 along with documentation supporting your claim, such as proof of retirement or reduced income. While this may sound simple, understanding what qualifies, gathering the right documents, and presenting your case effectively can be harder than it seems.

Does IRMAA go away automatically if my income drops, or do I need to report it to Social Security?

IRMAA doesn’t just fall off on its own when your income goes down. Social Security bases it on the tax return from two years ago. If your income has dropped because of retirement, a job loss, or another life change, you’ll need to let Social Security know. You can do that by filling out Form SSA-44 or by calling them. Once they review your situation, they can lower or remove the IRMAA.How a Medicare Advisor Can Help

A Medicare advisor’s job is to understand the ins and outs of the program, including IRMAA appeals, and guide you through the process so you can potentially reduce your premiums faster and with less stress.

Here’s how they can help:

-

Identifying if You Qualify for an Appeal

A Medicare broker can review your current and past income, your life events, and your tax situation to determine if you meet SSA’s criteria for an IRMAA adjustment. This prevents you from wasting time on an appeal that’s unlikely to be approved. -

Helping With Documentation

One of the biggest reasons appeals are denied is incomplete or unclear documentation. An advisor can help you gather and organize the correct proof, like retirement letters, pay stubs, or tax records, so your application is solid from the start. -

Filing Correctly the First Time

A Medicare agent understands the nuances of Form SSA-44 and can guide you in filling it out accurately, reducing the risk of delays or denials caused by small mistakes. -

Explaining the Impact on Your Overall Medicare Plan

If your IRMAA is lowered, it changes your total monthly costs. An advisor can help you see how this fits into your budget and even review your Medicare plan options during open enrollment to ensure you’re not overpaying elsewhere.

Why Many Beneficiaries Choose Professional Help

Some people successfully appeal IRMAA on their own, but others prefer professional guidance, especially if the stakes are high. A Medicare advisor doesn’t just fill out forms; they offer peace of mind, help you avoid costly errors, and can also review your coverage to ensure you’re getting the most out of your benefits.

One quick caveat: not every agent handles IRMAA appeals. Ask upfront whether an advisor offers this service before sharing income documents or tax records.

It’s also worth noting that Medicare brokers and agents typically do not charge you directly for their services when helping with plan selection, they’re compensated by the insurance companies when you enroll in a plan. While IRMAA appeal assistance may be offered as part of their advisory service, many advisors integrate this into an overall review of your Medicare situation.

Common Misunderstandings About IRMAA Appeals

Many beneficiaries assume that once SSA sets their IRMAA, nothing can be done. Others believe that filing an appeal guarantees success. In reality:

-

Appeals must be based on approved life-changing events. For example, see how the loss of a spouse can affect your Medicare and Social Security.

-

You need proof of the event and its impact on your income.

- Timing matters. Filing too late or without current documentation can hurt your chances.

A Medicare advisor can clarify these points and set realistic expectations, so you’re not blindsided by the process.

Your Moves Matter

If your Medicare premiums have gone up due to IRMAA and your income has dropped since the tax year SSA is using, you have the right to appeal. Beyond the appeals process, there are also proactive income strategies that can help you avoid or reduce IRMAA surcharges before they hit. While you can go through the process on your own, working with a Medicare advisor, broker, or agent can streamline the process, improve your documentation, and potentially speed up a favorable decision.

Appealing an IRMAA adjustment isn’t just about saving money, it’s about making sure your premiums fairly reflect your current financial reality. With expert guidance, you can navigate the process more confidently and focus on enjoying your retirement without unnecessary financial strain.