Do You Need Medicare If You Have VA Benefits? What Veterans Need to Know

-

August 9, 2025

For millions of U.S. veterans, VA health care has served as an essential lifeline. When turning 65, many veterans face a common question: Should I enroll in Medicare if I already have VA benefits? At first glance, the idea of signing up for another health insurance program, especially one that comes with monthly premiums, may seem unnecessary. However, failing to enroll in Medicare could leave veterans vulnerable to coverage gaps, unexpected costs, or restricted access to care.

Here's what veterans need to know about how Medicare and VA benefits work together, and why enrolling in both is often the smartest decision.

How VA Health Benefits Work

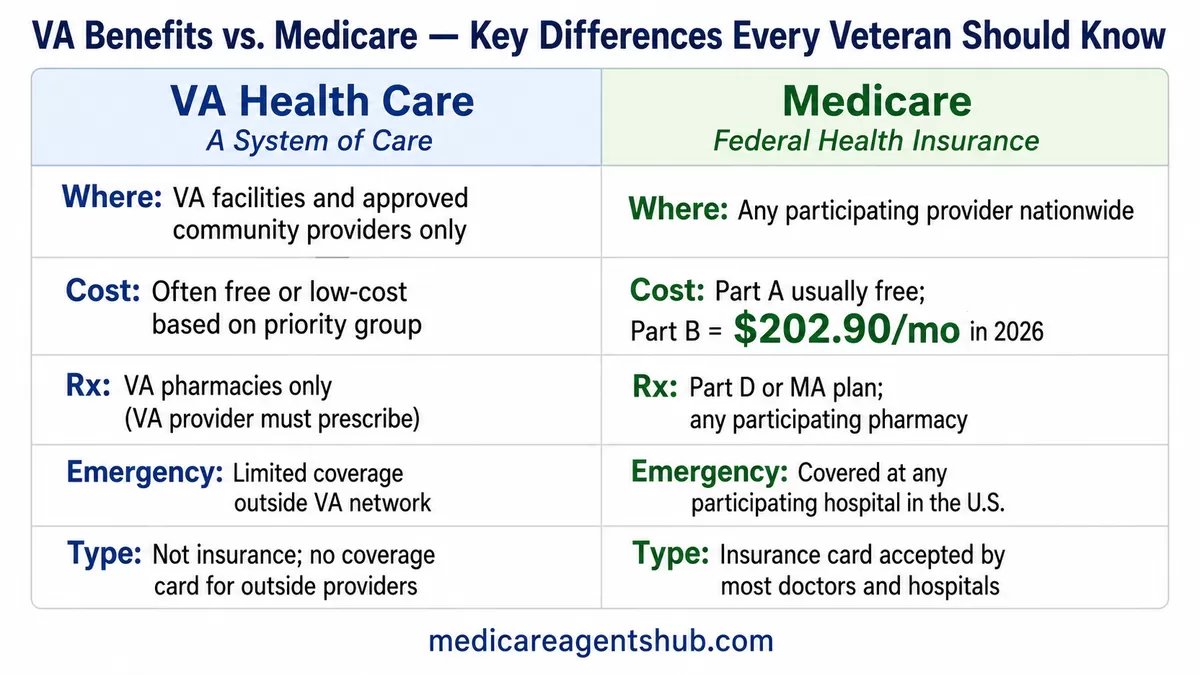

The U.S. Department of Veterans Affairs (VA) provides health care to eligible veterans through a network of VA medical centers, outpatient clinics, and affiliated facilities. VA health care is generally low-cost, and in some cases, completely free depending on the veteran's priority group, service-connected disability rating, and income.

However, VA health care is not insurance. It is a system of care that only covers services provided within the VA network or pre-authorized care from approved community providers. This limitation becomes important when veterans need care outside of the VA. For instance, in emergencies, when traveling, or when specialized services aren't available within VA facilities.

What Medicare Covers and Why It Matters

Medicare is a federal health insurance program for individuals aged 65 and older, as well as younger people with qualifying disabilities. Original Medicare consists of Part A (hospital insurance) and Part B (medical insurance). Part A is typically premium-free if you or your spouse paid Medicare taxes during your working years. Part B, however, comes with a monthly premium: $202.90 per month in 2026 for most enrollees.

While VA benefits only cover VA-authorized care, Medicare provides access to nearly every hospital, doctor, or specialist in the country. By enrolling in Medicare, veterans expand their care options and ensure they're covered when the VA system cannot meet their needs. Part B also covers a wide range of preventive screenings and services that can catch health issues early.

This is particularly important in emergency situations. If you need emergency care at a non-VA hospital, the VA may not cover those costs (especially if you are not enrolled in Medicare and the care isn't pre-authorized). Medicare, on the other hand, will cover emergency treatment at any participating facility in the U.S.

Why Veterans Should Enroll in Medicare Part B

The biggest hesitation among veterans is often Medicare Part B, which comes with that monthly premium. But opting out of Part B can result in costly consequences down the road.

If you don't sign up for Medicare Part B when first eligible at age 65, and later decide you want it, you'll likely face a late enrollment penalty. This penalty is permanent and increases the longer you go without coverage. Even if you rely exclusively on the VA for years, once you need care outside the VA, you might find yourself without coverage and paying higher Medicare premiums for the rest of your life. For a full breakdown of how these penalties work and how to avoid them, see our guide on avoiding Medicare penalties when turning 65.

I’ll be turning 65 in April. I have full VA coverage and good hospital and doctor coverage through Eisenhower here in the desert. The VA doesn’t provide dental care. Do I still need to enroll in Medicare, and if so, which part makes sense for my situation?

Penalty avoidance – The Part B late-enrollment penalty is permanent, so even if you don’t think you’ll need it now, enrolling at 65 keeps the door open without extra cost later.Freedom of choice – VA care is excellent for many, but it’s tied to VA facilities. Medicare gives you access to a much wider network, which can be crucial if you want to see a specialist outside the VA system or if you’re traveling.

Safety net – Life changes — you might move, your preferred VA clinic could get busier, or you might need urgent care while away from home. Medicare fills those gaps.

Smart coordination – You can strategically use VA for certain services (like prescriptions) and Medicare for others (like local specialists), often lowering your out-of-pocket costs.

Regarding Dental, Medicare generally doesn’t cover routine dental. You’d need a standalone dental plan or a Medicare Advantage plan that includes dental benefits.

Some veterans assume they'll never need non-VA care. But health needs change. If the VA cannot provide a specific treatment or specialist, or if you relocate to an area with limited VA facilities, having Medicare ensures you won't be left without options.

Medicare and VA Benefits Don't Overlap, They Complement Each Other

VA benefits and Medicare do not coordinate or share costs. You cannot use VA coverage to pay your Medicare co-pays, and vice versa. But having both gives you dual access: VA care when it suits your needs, and Medicare-covered care when the VA is unavailable or inconvenient.

Can you explain how Medicare works with other types of insurance like Veterans Affairs benefits or employer plans?

Medicare can work alongside other insurance types like VA benefits and employer-sponsored plans, but coordination rules vary. VA benefits are separate, and you choose which to use for each service. Medicare and VA benefits generally don't pay for the same services, with the VA covering care at VA facilities and Medicare covering care elsewhere. Medicare pays second to employer plans if you're working past 65This flexibility is especially valuable in rural or underserved areas where VA facilities may be hours away. Veterans with Medicare can see local doctors or go to nearby hospitals rather than traveling long distances.

What About Medicare Advantage or Part D?

Some veterans consider Medicare Advantage (Part C) plans, which bundle Medicare Parts A and B, often with extra benefits like dental or vision. These plans may be attractive if you want additional benefits and are comfortable with provider networks. However, since VA benefits already include prescription coverage, many veterans don't enroll in Medicare Part D (standalone drug coverage). Still, having a Medicare Advantage plan with prescription coverage may offer added flexibility when filling prescriptions outside of the VA system.

If you do choose to use VA pharmacies, your prescriptions must be written by a VA provider, which can sometimes limit access to certain medications prescribed by outside physicians.

How do eligibility rules differ for those on TRICARE or Veterans Affairs (VA) benefits?

For those that have earned VA benefits the goal is to find a Medicare plan that can add another layer of coverage to the benefits they are entitled to through their military service. The flexibilty to go to a local doctor or fill a prescription at a local pharmacy so that don't need to run to the VA hospital for everything. Typically, a low cost Medicare Advantage plan will achieve this goal and not impact their VA benefits.So, Should You Enroll in Medicare If You Have VA Benefits?

In most cases, yes, veterans should enroll in Medicare Parts A and B when they become eligible. Doing so ensures more complete health coverage and protects against unexpected costs. Even if you plan to use the VA as your primary provider, Medicare offers valuable coverage outside the VA system, especially in emergencies or when traveling.

Think of Medicare as a safety net that fills in the gaps the VA cannot cover. For most veterans, the combination of VA benefits and Medicare provides peace of mind and broad access to quality care nationwide. You can also explore common questions veterans ask about Medicare and VA coverage to learn what other vets are asking.

A Smart Strategy for Lifelong Coverage

Enrolling in Medicare (even when you have access to VA health benefits) isn't redundant; it's a strategic move. It expands your choices, protects against future penalties, and ensures you're never caught off guard by limitations in either system. Some Medicare Advisors even specialize in working with Veterans for this reason.

If you're nearing 65 or helping a veteran prepare for Medicare, consider speaking with a licensed Medicare advisor who understands how VA benefits work. Platforms like MedicareAgentsHub.com can connect you with independent brokers who can explain your options clearly and help you make the right call based on your unique situation.