Questions Agents Think You Should Ask When it Comes to Medicare

-

August 20, 2025

After interviewing over 120 Medicare agents on Medicare Agents Hub, one thing became clear: the questions most people ask about Medicare aren't the ones that matter most. Costs, enrollment deadlines, and the difference between Parts A through D? Those are starting points, not the finish line.

The agents we spoke with were asked a simple question: "What's the most important question I should be asking about Medicare that I probably haven't thought of yet?" Their answers reveal five overlooked but critical areas that can make or break your Medicare experience, especially as your life and health evolve over time.

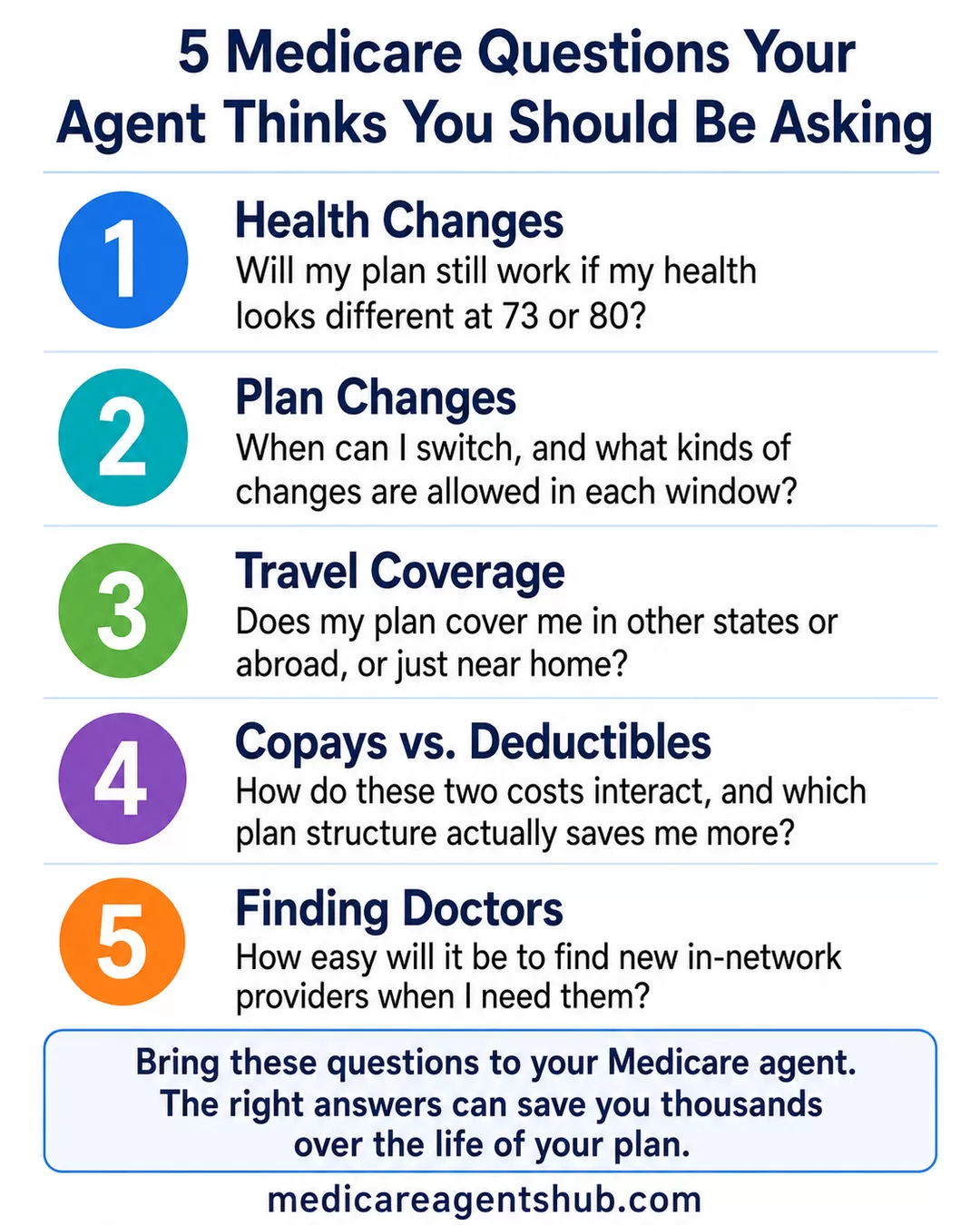

Here are the five questions this article covers:

- How can my Medicare plan still meet my coverage needs if my health changes?

- How often can I change my Medicare plan?

- Are there plans that allow me to travel anywhere and still be covered?

- What's the difference between copays and deductibles?

- How can I find new doctors in my network?

How Can My Medicare Plan Still Meet My Coverage Needs If My Health Changes?

Too many Medicare beneficiaries choose a plan based solely on their needs at age 65, then forget to consider how their health might look at 68, 73, or 80. In an answer to this question, Tracy Davis explains:

"The great thing with Medicare is there isn't 'one size fits all', so each year things are changing and evolving. I have plenty of members that begin their Medicare journey at 65 years old and are healthy. Eventually, they experience some health concerns and are able to utilize additional 'add ons' to their plans to fill in the gaps that Medicare doesn't cover."

This is why asking how flexible a plan is over time matters so much. Does it allow you to add supplemental coverage if you develop a chronic illness? Is the prescription drug coverage robust enough to handle new medications down the road?

The best Medicare strategies are layered. A good agent will explain how Medigap plans, Advantage plans, or standalone Part D drug options can be added or switched to keep your coverage strong, even when your health shifts. If you're living with a chronic condition, proactive planning is one of the smartest steps you can take.

How Often Can I Change My Medicare Plan?

Parris Brady stresses that people often misunderstand how much flexibility they actually have when switching plans. Depending on the time of year and the type of plan you have, your options may be wider (or more limited) than you realize. Parris replied to this question saying:

"AEP starts October 15th through December 7th. You can change plans as often as you like during that time period. However, after January 1st through March 31st (OEP), if you have a Medicare Advantage plan, you are allowed only one (1) change to another Medicare Advantage plan."

The rules change once you step outside of AEP. From January 1 through March 31, the Medicare Advantage Open Enrollment Period (OEP) applies, but this only allows individuals enrolled in a Medicare Advantage plan to switch to another Advantage plan or go back to Original Medicare entirely.

There are also Special Enrollment Periods (SEPs) throughout the year tied to life events like moving, losing group coverage, or becoming eligible for Medicaid. Knowing exactly when you can change plans, and which changes are allowed during each window, ensures you're not stuck in a plan that no longer meets your needs.

Are There Plans That Allow Me to Travel Anywhere and Still Be Covered?

A common misconception is that all Medicare plans travel with you wherever you go. Kelli Holt answers this question directly:

"Original Medicare (Part A and Part B) generally provides coverage nationwide, so you can get care anywhere in the U.S. However, it doesn't cover non-emergency care outside the U.S. Medicare Advantage plans (Part C) often have network restrictions, so coverage may be limited when traveling outside your plan's service area. Some plans offer coverage for emergency care when you're traveling within the U.S. or even abroad, but it varies by plan."

Original Medicare does not cover non-emergency care abroad. Some Medicare Supplement (Medigap) plans (specifically Plans C, D, F, G, M, and N) include foreign travel emergency coverage up to a $50,000 lifetime limit, after a small yearly deductible and with 80/20 coinsurance.

Medicare Advantage (Part C) plans typically have network restrictions and may not cover anything outside your geographic service area. While emergency situations are usually covered, routine care could be excluded or billed at an out-of-network rate.

If you're a snowbird splitting time between two states, this is especially important to plan for. Frequent travelers should ask whether a plan offers travel-friendly features like nationwide networks or emergency foreign travel benefits. Certain PPO plans or plans with national networks can make a significant difference in peace of mind.

What's the Difference Between Copays and Deductibles?

Understanding the terminology of Medicare is one of the quickest ways to avoid surprise bills. Daniel Underwood explains simply:

"A deductible is the amount you must pay out of pocket each year before your insurance starts covering costs. A copay is a set dollar amount you pay each time you get a service, like a doctor visit or prescription, even after your deductible is met."

For example, even if you've already met your deductible for the year, you may still have to pay a $30 copay each time you visit a specialist.

Why does this question matter? Because two plans can look identical at first glance (similar premiums, same networks) but a lower deductible paired with higher copays can prove more expensive over time depending on your usage.

People who visit doctors frequently are often better served with a plan that has higher premiums and low copays. Someone who rarely sees a doctor might prefer a lower-premium plan even if the deductible is higher. Understanding how these two costs work together gives you a clearer picture of your true out-of-pocket spending.

What Agents Wish You Knew Before Picking a Plan

What's one piece of advice you wish every senior knew before picking a Medicare plan?

One piece of advice I wish every senior knew before picking a Medicare plan is that the best plan for your neighbor or spouse isn’t necessarily the best plan for you. Everyone’s health needs, prescriptions, preferred doctors, and budget are different — and Medicare plans can vary drastically in how they cover those specifics. What looks good on paper or worked well for someone else might leave you paying much more out-of-pocket or losing access to your preferred providers. Taking the time to review your medications, doctors, and expected care needs each year can make a huge difference in both cost and peace of mind.I always tell clients that Medicare isn’t a “set it and forget it” decision. Plans change every year — premiums, drug formularies, and networks shift — so an annual review with a trusted, licensed agent ensures you’re still in the plan that truly fits your life. A little preparation before enrolling can save hundreds, even thousands, of dollars and prevent surprises later in the year.

How Can I Find New Doctors in My Network?

Another highly overlooked question is about how easy it will be to access providers, not just today, but in the future. Tracy Davis says:

"My members call me and ask for a list of doctors in the area that take their plan. The insurance company also provides an app you can download on your phone and look there for an in-network provider. Most of their websites will also have a way to check to see if a provider is in-network."

Even if you have good relationships with your current doctors, providers move, retire, or sometimes stop accepting your insurance. What matters is not just whether the plan has doctors in your area right now, but how easy it will be to find new in-network doctors whenever you need them.

Many insurance companies offer apps and website tools to search their provider network on demand. And perhaps most importantly, your local Medicare agent can help you find and verify trusted physicians in your network. This becomes even more critical if you move to a new city or develop a condition that requires a specialist you haven't worked with before.

The Biggest Enrollment Mistake, According to Agents

What is the biggest mistake seniors make when enrolling in Medicare?

In my experience, the biggest mistake seniors make with Medicare is listening to their friends and choosing a plan based on what works well for someone who isn't in their shoes. Don't get me wrong - people who are already in the Medicare system can provide great insight into the things they like and dislike about their plans and experiences with Medicare, but they are not you. Only you know what is important to you. You know what your medical needs have been and what they are most likely to be in the future. You know how you feel about "managed care", prior authorizations and networks and only you know your budget.Even if you listen to your friends and choose Medicare Advantage over Original Medicare, only you know what doctors you want to see and what medications you need to have covered on the formulary. And if your life experience is different and you already have a chronic condition, only you can decide if you would sleep better at night with Original Medicare and a Supplement plan than you would with Medicare Advantage.

When you choose your first Medicare plan, it could be the last health insurance plan that you choose for the rest of your life. This decision is too important to make on a whim or because a plan worked great for your pickle ball buddies. Give it the time and consideration that it deserves.

Making the Most of These Questions

Choosing a Medicare plan doesn't end when you enroll. It's an ongoing process that requires asking the right questions, especially the ones most people don't think to ask.

By bringing these five questions to your local Medicare advisor early in your Medicare journey, you position yourself to make informed decisions not just at enrollment, but every year as your needs and lifestyle change.

Medicare isn't static, and your plan shouldn't be either.

Want help walking through these questions with a professional? Find a licensed Medicare agent in your area, or contact your State Health Insurance Assistance Program (SHIP) for free, unbiased counseling.