Learn How Medigap Insurance Functions

-

Last Updated July 21, 2026

Written by Brian Biesiadecki

Medicare Agent Licensed in FL, GA, MI & 2 other states

To purchase a Medigap policy, you typically need to have Original Medicare — both Part A and Part B. Remember, a Medigap policy is designed to cover only one individual; therefore, if both you and your spouse wish to have Medigap coverage, each of you must obtain your own policy.

How Medigap Claims and Payments Work

When you receive medical care, Medicare will cover its share of the Medicare-approved costs for covered services. Most Medigap policies require you to allow the Medigap insurance company to access your Part B claims information directly from Medicare. Your Medigap policy will then pay your doctor the amount owed under your policy, while you will be responsible for any remaining costs. Some Medigap insurers also do this for Part A claims.

If your Medigap insurance company does not retrieve your claims information from Medicare, check with your doctors to see if they "participate" in Medicare. This means they "accept assignment" for all Medicare patients. If your doctor participates, your Medigap insurer is obligated to pay your doctor directly, provided you request it.

Medigap Policy Renewal and Retention Rules

Once you purchase a Medigap policy, you can retain it as long as you continue to pay your premiums. All standardized Medigap policies are automatically renewed each year, even if you encounter health issues. Your Medigap insurer may only terminate your policy under the following circumstances:

- You stop making premium payments

- You provided false information on your Medigap application

- The insurance company goes bankrupt or ceases operations

Medigap Policy Retention

Key Points:

- Automatic Annual Renewal

- Policy Termination Conditions:

- Non-payment of premiums

- False application information

- Insurer bankruptcy or closure

Note: Always review policy details.

How Medigap Works with Other Medicare Coverage

Medigap vs. Medicare Advantage Plans

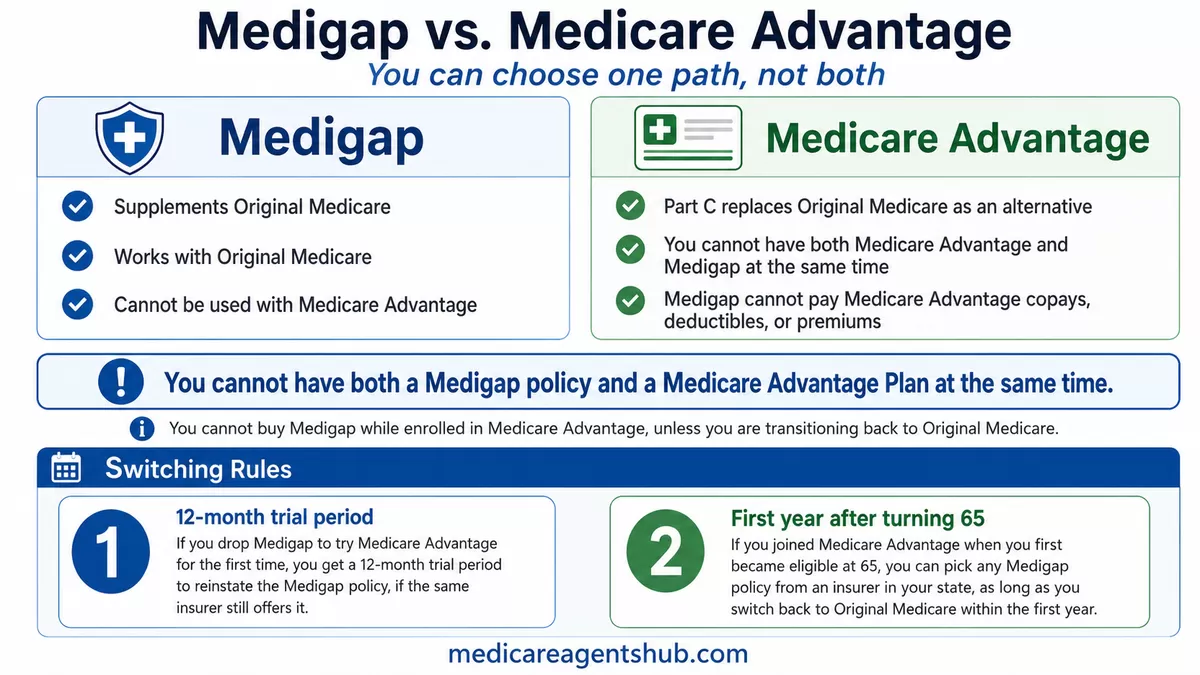

A Medigap policy differs from a Medicare Advantage Plan (Part C). While a Medicare Advantage Plan provides an alternative way to receive Medicare coverage besides Original Medicare, a Medigap policy serves as a supplement to Original Medicare. When you first enroll in Medicare, you can choose to purchase Medigap or sign up for a Medicare Advantage Plan, but you cannot have both simultaneously.

You cannot buy a Medigap policy while enrolled in a Medicare Advantage Plan unless you are transitioning back to Original Medicare. Medigap cannot be used to cover copayments, deductibles, or premiums associated with a Medicare Advantage Plan. If you wish to revert to Original Medicare and acquire a Medigap policy, reach out to your Medicare Advantage Plan to determine if you can disenroll.

If you decide to drop a Medigap policy to join a Medicare Advantage Plan for the first time, you will have a 12-month trial period to reinstate your Medigap policy, provided the same insurance company still offers it upon your return to Original Medicare. If it's unavailable, you can purchase a Medigap policy that you qualify for from an insurer in your state (excluding Plans M and N). Additionally, you may have the chance to enroll in a Medicare drug plan during this time.

If you enrolled in a Medicare Advantage Plan when you first qualified for Medicare Part A at age 65, you can select from any Medigap policy available from an insurer in your state if you switch to Original Medicare within the first year of joining the Medicare Advantage Plan. You may also have an opportunity to enroll in a Medicare drug plan then.

Medigap and Prescription Drug Coverage

Policies sold after 2005 do not include prescription drug coverage. Therefore, if you enroll in Medigap for the first time, it will not cover medications. If you need prescription drug coverage, you can join a separate Medicare drug plan (Part D). What if you already have a Medigap policy that includes drug coverage?

Tip: If you sign up for both a Medigap policy and a Medicare drug plan from the same company, you may need to make two separate premium payments for your coverage. Reach out to your insurance provider for further information.

If you're looking for help understanding your Medigap options, consider speaking with a licensed Medicare agent near you who can walk you through the plans available in your state.

About the Author: Brian Biesiadecki of Medicare Simplified is a Medicare Agent with 11+ Years of Experience, licensed in FL, MI, OH, SC, TX and VA.