Medicare Supplements vs. Medicare Advantage Plans: Key Differences

When it comes to enhancing your healthcare coverage under Medicare, two popular options are available: Medicare Supplement (Medigap) plans and Medicare Advantage (Part C) plans. While both aim to reduce out-of-pocket costs and provide more comprehensive coverage, they work in very different ways. Understanding the distinction between the two can help you make an informed decision about which option is best for your healthcare needs.

What is Medicare Supplement (Medigap)?

Medicare Supplement, often referred to as Medigap, plans are sold by private insurance companies and are designed to work alongside Original Medicare (Parts A and B). These plans help cover the "gaps" in coverage that Original Medicare doesn’t pay for, such as copayments, coinsurance, and deductibles. Medigap plans are standardized, with 10 different plan options labeled A through N, each offering varying levels of coverage.

Key Features of Medigap Plans:

- Supplemental Coverage: Medigap plans cover the out-of-pocket expenses that Original Medicare does not, helping reduce financial burdens.

- Coverage Options: These plans typically cover Part A and Part B coinsurance, blood, skilled nursing facility coinsurance, and sometimes Part A deductibles and excess charges.

- No Network Restrictions: Medigap plans don’t restrict which doctors, hospitals, or specialists you can visit, as long as they accept Medicare. There are no regional network limitations.

- Flexibility: You can use your Medigap plan across the U.S., offering peace of mind for frequent travelers or those living in multiple locations.

- Standardized Plans: Medigap plans are standardized by the federal government, meaning that a Plan G in one state is identical to a Plan G in another. The only variation is the price, which may differ depending on the insurance provider. Medigap premiums can also increase over time.

Who Should Consider Medigap?

Medigap plans are a good option for those who prefer having fewer limitations on care and want to minimize out-of-pocket costs. If you are healthy and want flexibility in healthcare providers, a Medigap plan could be a strong choice. It is also ideal for individuals who travel frequently and prefer to have nationwide coverage.

What is Medicare Advantage (Part C)?

Medicare Advantage, also known as Part C, is an alternative to Original Medicare that is offered by private insurance companies. Medicare Advantage plans combine the coverage of Parts A and B into one plan and often include additional benefits such as prescription drug coverage (Part D), dental, vision, and hearing services. Unlike Medigap, which supplements Original Medicare, Medicare Advantage plans completely replace it.

Key Features of Medicare Advantage Plans:

- All-in-One Coverage: Medicare Advantage plans often include coverage for hospital stays (Part A), doctor visits (Part B), and sometimes additional benefits like prescription drugs (Part D), dental, vision, and wellness programs.

- Fixed Costs: Many Medicare Advantage plans have lower monthly premiums than Medigap plans, but they often come with deductibles, copayments, and coinsurance. These plans may have an out-of-pocket maximum, which limits the total amount you’ll pay for services in a given year.

- Network Restrictions: Most Medicare Advantage plans operate with network restrictions. Depending on the plan, you may need to use a specific network of doctors and hospitals, and you may need a referral to see a specialist. This can limit your freedom of choice in healthcare providers.

- Additional Benefits: Many Medicare Advantage plans offer benefits not covered by Original Medicare, such as prescription drug coverage, dental and vision care, hearing aids, gym memberships, and wellness programs.

- Annual Plan Changes: Unlike Medigap plans, Medicare Advantage plans can change each year. Premiums, benefits, and network providers can all vary annually, so you must review your plan regularly to ensure it meets your needs.

Who Should Consider Medicare Advantage?

Medicare Advantage plans are ideal for individuals who want an all-in-one solution and are comfortable with network restrictions. If you’re looking for a plan that bundles coverage with additional benefits like dental and vision, and you are okay with working within a specific network of providers, Medicare Advantage might be the right choice. These plans can be especially beneficial for those who need prescription drug coverage and want to avoid the need to buy a separate Part D plan.

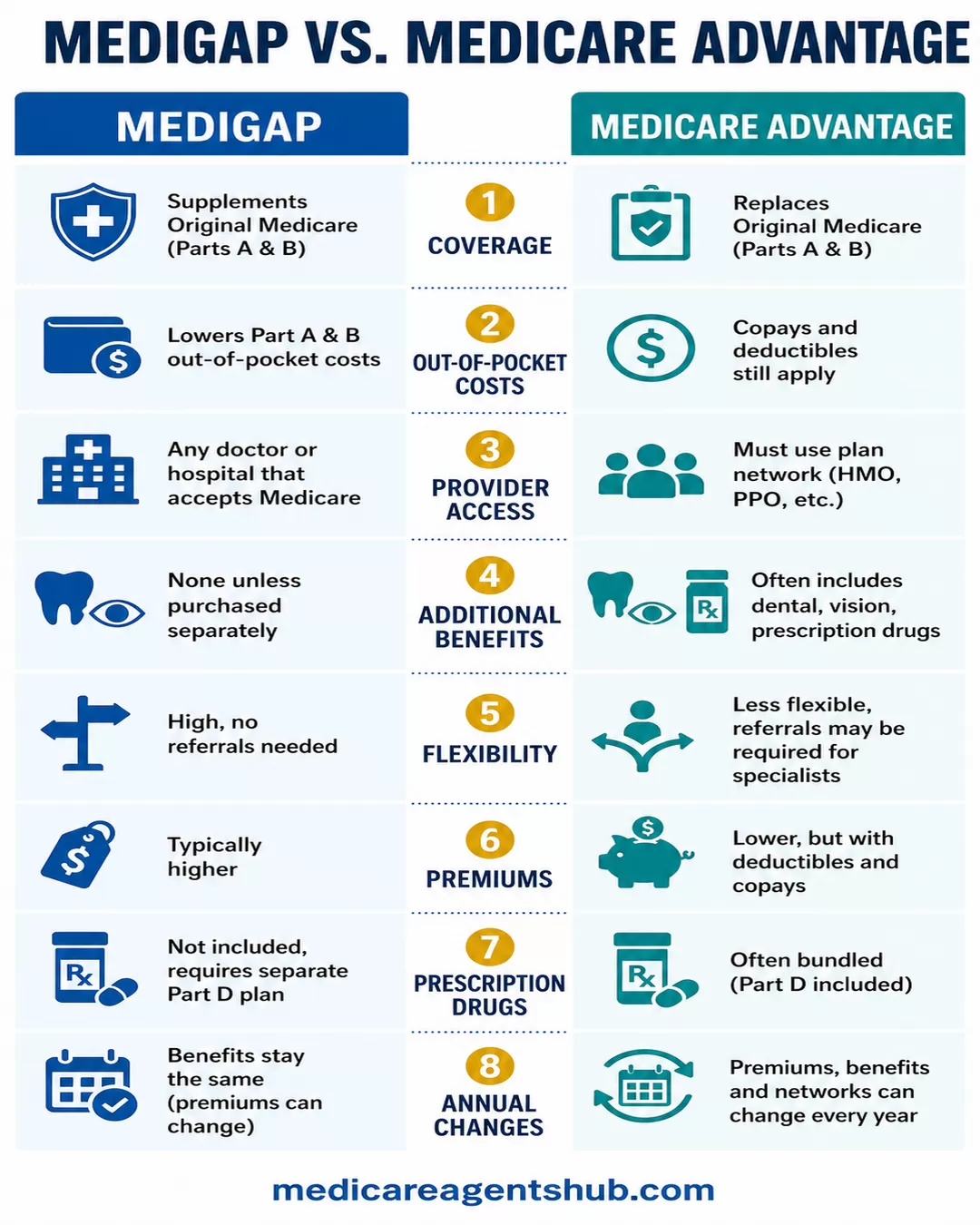

Key Differences Between Medicare Supplement and Medicare Advantage Plans

Here’s a more detailed comparison of the two options:

- Coverage

- Medicare Supplement (Medigap): Supplements Original Medicare (Part A and B).

- Medicare Advantage (Part C): Replaces Original Medicare (Parts A and B).

- Out-of-Pocket Costs

- Medicare Supplement: Lowers out-of-pocket costs for Part A and B.

- Medicare Advantage: Can have out-of-pocket costs such as copays and deductibles.

- Provider Access

- Medicare Supplement: Access to any doctor or hospital that accepts Medicare.

- Medicare Advantage: Network restrictions, must use plan’s network (HMO, PPO, etc.).

- Additional Benefits

- Medicare Supplement: No additional benefits unless you purchase separately.

- Medicare Advantage: Often includes extra benefits like dental, vision, and prescription drug coverage.

- Flexibility

- Medicare Supplement: High flexibility, no referral needed.

- Medicare Advantage: Less flexibility, may need referrals for specialists.

- Premiums

- Medicare Supplement: Typically higher premiums.

- Medicare Advantage: Lower premiums, but may have deductibles and copays.

- Prescription Drugs

- Medicare Supplement: Not included, must be added through a separate Part D plan.

- Medicare Advantage: Often includes prescription drug coverage (Part D).

- Annual Changes

- Medicare Supplement: Premiums can change, but benefits remain the same.

- Medicare Advantage: Plan benefits, premiums, and network may change annually.

Which Plan is Right for You?

Choosing between Medicare Supplement and Medicare Advantage depends on your healthcare needs, preferences, and budget.

- Medicare Supplement (Medigap) might be a better fit if you prefer the flexibility to see any doctor or specialist who accepts Medicare and want predictable out-of-pocket costs with minimal surprise charges.

- Medicare Advantage (Part C) is a great option if you’re looking for a lower-cost plan with the convenience of bundled benefits, including prescription drugs and additional services like dental and vision, and are willing to use a network of providers.

Ultimately, the right choice for you will depend on your medical needs, whether you need prescription drug coverage, how much you're willing to pay in premiums, and whether you're comfortable with network restrictions.

Conclusion

Both Medicare Supplement and Medicare Advantage plans are designed to enhance your Medicare coverage, but they cater to different needs and preferences. Understanding the differences—such as coverage, cost, flexibility, and additional benefits—can help you make an informed decision that ensures you get the right healthcare coverage for your needs.

About the author: Jennifer Robbins is a seasoned Medicare Broker with extensive expertise in helping individuals navigate the complexities of Medicare. With a deep understanding of Medicare Supplement and Medicare Advantage plans, Jennifer is dedicated to empowering clients to make informed healthcare decisions that fit their unique needs. Her passion for simplifying the Medicare process ensures personalized guidance and peace of mind for every client.