Why Medicare Should Be Part of Your Retirement Strategy

Many people assume Medicare will simply "take care of things" once they turn 65. But like any government program, it comes with complexities, options, and gaps. Understanding how Medicare works, and how to plan for its costs and coverage limits, can help you protect your retirement savings and gain peace of mind.

Medicare Isn’t One-Size-Fits-All

Medicare isn’t just a single program. It’s a framework made up of several parts:

- Part A: Hospital insurance

- Part B: Medical insurance

- Part C (Medicare Advantage): All-in-one alternatives to Original Medicare

- Part D: Prescription drug coverage

- Medigap: Supplemental insurance to help cover out-of-pocket costs

Depending on your health, lifestyle, budget, and long-term goals, your ideal Medicare setup might look very different from someone else’s. That’s why creating a custom Medicare strategy, just like you would with Social Security or investment income, is so important.

Understanding Original Medicare (Parts A and B)

At its core, Original Medicare includes Part A and Part B.

Part A is typically premium-free for individuals who meet eligibility based on work history. Part A covers inpatient hospital stays, hospice care, some skilled nursing facility care, and limited home health services.

Part B has a monthly premium and covers outpatient care, such as doctor visits, preventive services, lab tests, mental health services, and more.

What many don’t realize is that Original Medicare comes with cost-sharing responsibilities. These include deductibles, coinsurance, and copayments. There is no out-of-pocket maximum with Original Medicare alone. That means there’s no cap on how much you might spend in a year if your medical needs are significant.

Additionally, Original Medicare does not cover:

- Routine dental, vision, or hearing services

- Prescription drugs

- Long-term care or custodial nursing home stays

- Care received outside the U.S.

These gaps can come as a surprise, and they may quickly impact your financial well-being if not addressed in your retirement plan.

Supplementing Original Medicare: Part D, Medigap & More

To help close these gaps, many retirees choose to add supplemental coverage.

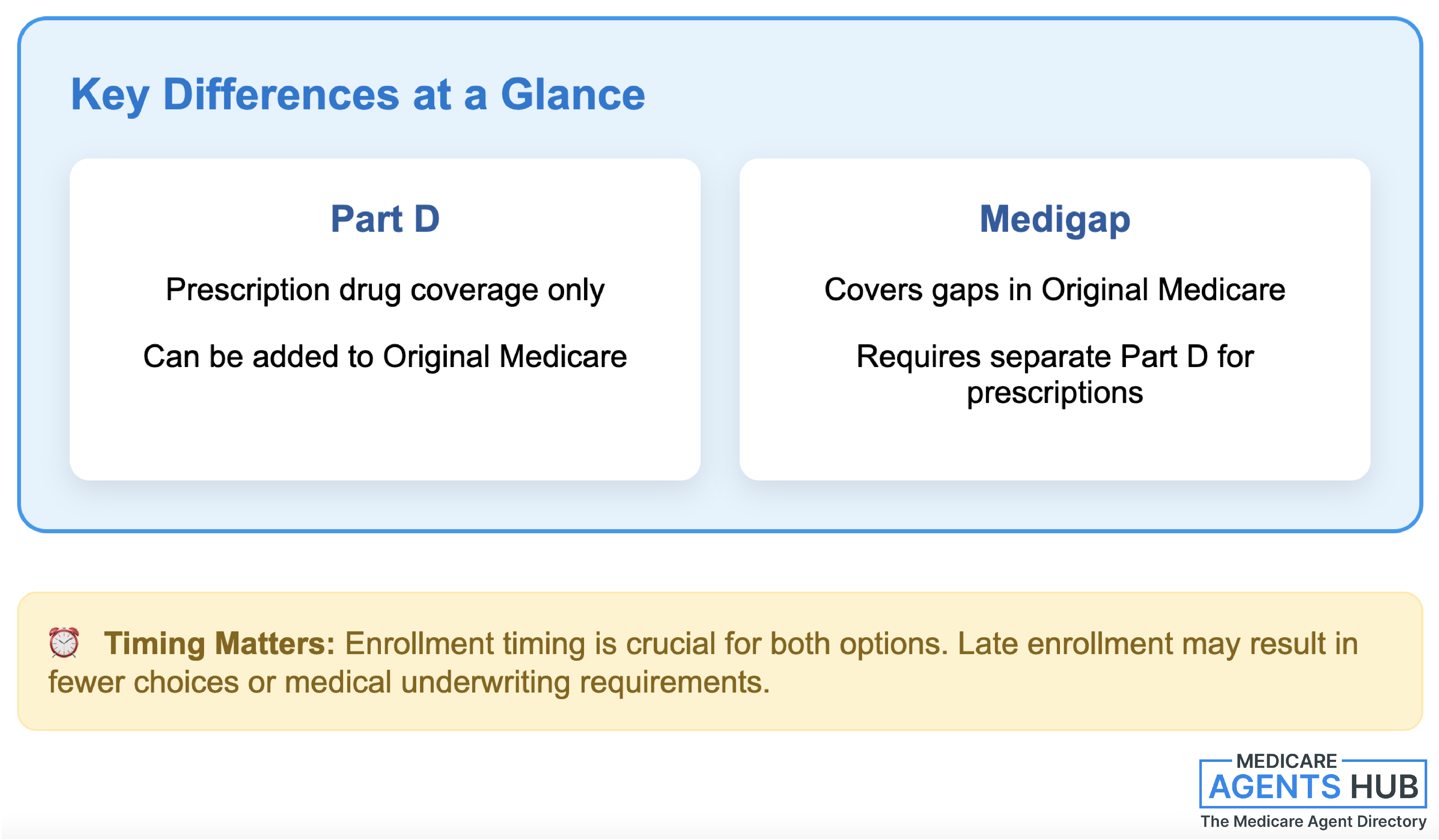

Part D: Prescription Drug Plans

Part D plans help cover the cost of prescription medications and are offered through private insurance companies. While premiums and deductibles vary, it's important to understand that not all medications are covered the same way. These plans often use formularies and pricing tiers that can affect your out-of-pocket expenses.

Each year, drug plans may update their coverage. It’s wise to compare options annually during the Medicare Open Enrollment Period.

Medigap (Medicare Supplement Insurance)

Medigap policies are designed to help pay some of the costs not covered by Original Medicare, such as deductibles, coinsurance, and copays. These plans are standardized and sold by private insurers.

You must be enrolled in both Part A and Part B to buy a Medigap policy. However, Medigap plans do not include prescription drug coverage. You would still need a separate Part D plan if you choose this route.

While premiums vary based on plan, location, and age, many retirees appreciate the predictable out-of-pocket costs Medigap can provide. Timing your enrollment is important. You may have fewer plan choices or face medical underwriting if you apply later on.

Medicare Advantage (Part C): An Alternative Path

Instead of adding Part D and Medigap to Original Medicare, some retirees choose a Medicare Advantage plan, also known as Part C. These plans are offered by private insurance companies and typically bundle:

- Hospital and medical coverage (Parts A and B)

- Prescription drug coverage

- Additional benefits like dental, vision, hearing, fitness programs, and more

Medicare Advantage plans often operate through networks. You may need to use in-network doctors and facilities. Many plans offer low or even no premiums, but out-of-pocket costs can vary significantly depending on your use of services and whether you stay within the provider network.

This option might appeal to people who prefer simplicity and want extra benefits not included in Original Medicare. On the other hand, those who value provider flexibility or who travel frequently may find traditional Medicare plus a Medigap plan more suitable.

Early Retirement: Planning for the Medicare Gap

If you plan to retire before you're eligible for Medicare, you’ll need to consider how you’ll cover health care expenses in the interim. Options like COBRA, private individual insurance, or marketplace plans can help, but they may come with higher premiums or limited provider networks.

This gap in coverage is a critical part of your retirement plan. It should be addressed well in advance to avoid surprises or financial strain.

Why Your Medicare Strategy Impacts Your Retirement Plan

Think of Medicare as an essential component of your retirement safety net. The better your understanding and preparation, the more confident and secure you can feel as you transition out of the workforce.

An informed Medicare strategy can help you:

- Reduce the risk of unexpected health care costs

- Maintain access to the care and services you need

- Protect your retirement savings from erosion

- Align your health care decisions with your long-term financial goals

And let’s not forget, health care is consistently ranked as one of the top expenses retirees face. Preparing for these costs today can help prevent future stress and financial pressure.

Common Pitfalls to Avoid

Even savvy retirees can make mistakes with Medicare planning. Here are a few to watch for:

- Missing your Initial Enrollment Period (IEP) – This is a key window that starts a few months before your 65th birthday. Missing it can result in late enrollment penalties and gaps in coverage.

- Assuming Medicare covers everything – It doesn’t. Overlooking the gaps in dental, vision, drug coverage, or long-term care can lead to large out-of-pocket costs.

- Not reviewing plans annually – Medicare plans change, and so do your health needs. Re-evaluating your options during the Annual Enrollment Period helps ensure your coverage is still a good fit.

- Ignoring income-related adjustments – Higher earners may face surcharges on their premiums for Parts B and D. Being proactive about your taxable income in retirement can help manage these costs.

How to Start Building Your Medicare Strategy

You don’t need to be an expert, but you do need a plan. Begin by asking yourself:

- When do I want to retire, and how will I bridge the gap to Medicare if needed?

- Do I have ongoing medical conditions that require specific providers or medications?

- Would I rather manage my own coverage through multiple plans or have it all in one?

- Am I comfortable with provider networks, or do I want maximum flexibility?

Answering these questions can point you toward the right combination of coverage. From there, speaking with a licensed Medicare agent or financial advisor can help you explore your choices, compare plans, and understand enrollment timelines.

Medicare Is a Cornerstone of Retirement Planning

Too often, people think of Medicare as just another government program, something automatic that doesn’t require much attention. But Medicare is more than a health benefit. It is a strategic tool that, when used properly, can protect your finances, safeguard your health, and support your retirement lifestyle.

Whether you're approaching retirement or already there, it’s never too early or too late to take a closer look at how Medicare fits into your overall plan. Taking the time now, meeting with a Medicare Advisor and understanding your options can make a big difference later on, for both your wallet and your well-being.

About the Author: Allan Boothe of Revive Insurance is a Medicare-licensed insurance broker in UT, AK, AL, AR, AZ, CA, CO, CT, DC, DE, FL, GA, HI, IA, ID, IL, IN, KS, KY, LA, MA, MD, ME, MI, MN, MO, MS, MT, NC, ND, NE, NH, NJ, NM, NV, NY, OH, OK, OR, PA, RI, SC, SD, TN, TX, VA, VT, WA, WI, WV, WY and PR.