Understanding Medicare PPOs, HMOs, and POS Plans: A Guide for Seniors

-

Last Updated July 20, 2026

Written by Shiloh Carpentier

Medicare Broker Licensed in OK, AK, AZ & 18 other states

When it comes to choosing a Medicare plan, understanding your options can feel overwhelming. Three common types of plans available under Medicare Advantage (Part C) are Preferred Provider Organizations (PPOs), Health Maintenance Organizations (HMOs), and Point of Service (POS) plans. Each of these plan types comes with its own benefits and drawbacks, and knowing the differences can help you make an informed decision that suits your healthcare needs.

What Is a Medicare Advantage Plan?

Medicare Advantage plans are alternatives to Original Medicare, offering coverage for hospital and medical services (Parts A and B) and often including additional benefits like dental, vision, and prescription drug coverage. These plans are provided by private insurance companies and come in various forms, including PPOs, HMOs, and POS plans. To understand the basics of how Medicare works overall, see our Medicare 101 guide. Let’s dive into what each of these plan types entails.

Medicare Preferred Provider Organization (PPO) Plans

How Medicare PPO Plans Work

PPO plans offer flexibility when choosing healthcare providers. You have access to a network of doctors and hospitals, but you’re not restricted to using only those in the network. You can also see specialists without needing a referral from your primary care doctor.

Benefits of PPO Plans

- Freedom to Choose Providers: You can see any doctor or specialist, in or out of the network, though staying in-network usually costs less.

- No Referrals Needed: Unlike other plans, you don’t need a referral to visit a specialist.

- Comprehensive Coverage: Many PPOs include extra benefits like vision and dental care. See 7 surprising Medicare Advantage benefits most people don't use.

Drawbacks of PPO Plans

- Higher Costs: Premiums, copayments, and deductibles are typically higher than those of HMO plans. Some plans advertise $0 premiums — read the truth about "free" Medicare Advantage plans before assuming lower cost means better value.

- Out-of-Network Charges: While you can go out of network, you may face higher out-of-pocket costs for these services.

- Complexity: Understanding the differences in costs between in-network and out-of-network services can be confusing.

Who Should Consider a PPO?

A PPO might be a good choice if you value flexibility and don’t mind paying more for the ability to see a wider range of providers, especially if you have specific doctors or specialists you prefer who may not be in a network.

Medicare Health Maintenance Organization (HMO) Plans

How Medicare HMO Plans Work

HMO plans are structured around a network of healthcare providers. You must choose a primary care physician (PCP) who coordinates your care and provides referrals to specialists when needed. Typically, you must use providers within the plan’s network for your care to be covered.

Benefits of HMO Plans

- Lower Costs: HMOs often have lower premiums and out-of-pocket expenses compared to PPOs.

- Coordinated Care: Your PCP helps manage your healthcare, ensuring you receive appropriate treatments.

- Predictable Costs: Copayments and coinsurance rates are usually straightforward and consistent.

Drawbacks of HMO Plans

- Limited Provider Network: You’re restricted to using network providers, except in emergencies.

- Referrals Required: You need a referral from your PCP to see a specialist, which can delay care in some cases.

- Lack of Out-of-Network Coverage: Non-emergency services outside the network typically aren’t covered.

Who Should Consider an HMO?

HMOs are ideal for individuals who prioritize lower costs and are comfortable receiving care within a defined network. If you don’t frequently see specialists or prefer a simpler, coordinated approach to your healthcare, an HMO might be a good fit.

Medicare Advantage Point of Service (HMO-POS) Plans

What Is an HMO-POS Plan and How Does It Work?

POS plans combine elements of both PPOs and HMOs. Like HMOs, you’ll need to select a primary care physician and get referrals for specialists. However, POS plans allow you to seek care outside the network, though at a higher cost.

Benefits of HMO-POS Plans

- Flexibility: You can go out of network for care if needed.

- Coordinated Care: Your PCP oversees your healthcare, similar to an HMO.

- Balanced Costs: POS plans often have moderate premiums and out-of-pocket expenses.

Drawbacks of HMO-POS Plans

- Referrals Needed: You’ll still need referrals for specialist visits, which can add an extra step.

- Out-of-Network Costs: While out-of-network care is allowed, it often comes with higher costs.

- Complexity: Understanding the balance between in-network and out-of-network care can be challenging.

Who Should Consider a POS Plan?

A POS plan might be suitable for those who want the structure of an HMO but also desire the flexibility to see out-of-network providers occasionally.

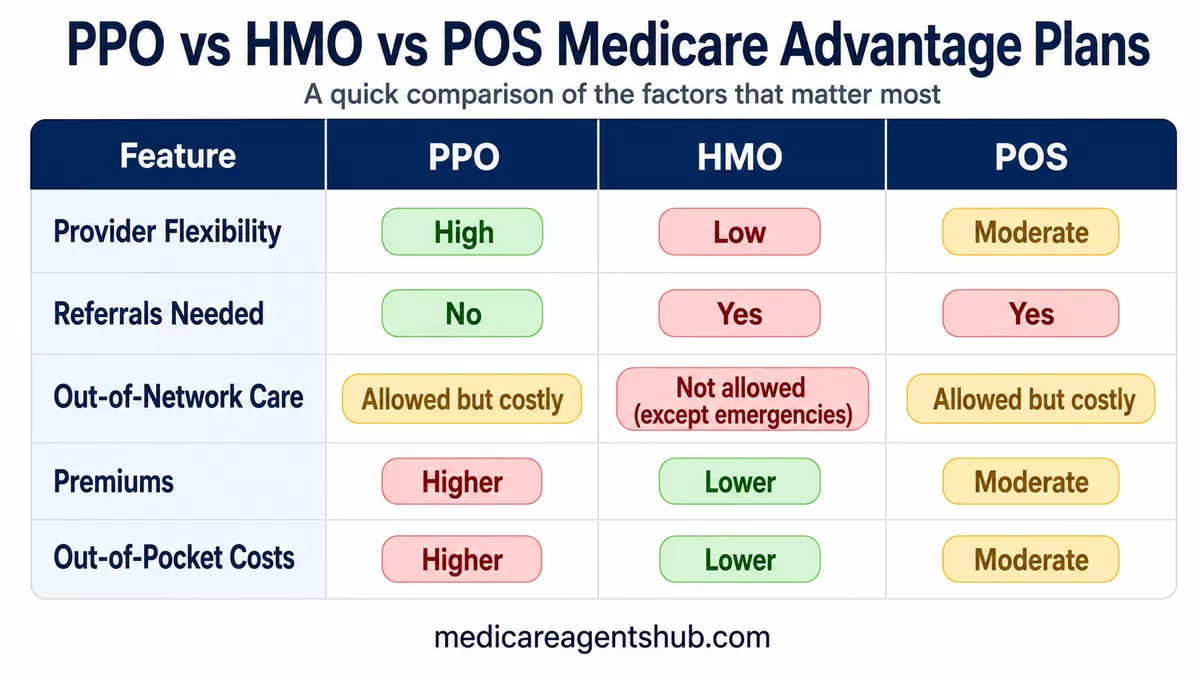

HMO vs PPO vs HMO-POS: Comparing Costs and Coverage

| Feature | PPO | HMO | POS |

| Provider Flexibility | High | Low | Moderate |

| Referrals Needed | No | Yes | Yes |

| Out-of-Network Care | Allowed but costly | Not allowed (except emergencies) | Allowed but costly |

| Premiums | Higher | Lower | Moderate |

| Out-of-Pocket Costs | Higher | Lower | Moderate |

Key Considerations for Seniors

When choosing between PPO, HMO, and POS plans, consider the following:

- Healthcare Needs

- Do you frequently visit specialists?

- Do you have specific doctors you prefer to see?

- Budget

- Are you comfortable paying higher premiums for greater flexibility?

- Do you need predictable costs to manage your healthcare expenses?

- Lifestyle

- Do you travel frequently and need out-of-network coverage? (See: How Medicare Works When You Live in Two States)

- Are you okay with staying within a network for most of your care?

- Convenience

- Do you prefer a simpler system with coordinated care?

- Are you willing to deal with referrals for specialist visits?

Conclusion

Choosing the right Medicare Advantage plan is a personal decision that depends on your health needs, financial situation, and preferences. PPOs offer the most flexibility but at a higher cost. HMOs provide affordability and simplicity, but with stricter network limitations. POS plans strike a balance, offering moderate costs and some flexibility.

Take the time to compare your options — our article Do You Have the Right Medicare Advantage Plan? can help — review the plan details, and to consult with a licensed Medicare advisor. By understanding the benefits and drawbacks of each plan type, you can select the coverage that best supports your health and well-being in your senior years.