Understanding the differences between Medicare Advantage vs. Medicare Supplement

The Medicare system can be overwhelming, and intimidating, especially since every year there are changes to the coverage. Most seniors struggle to understand all the various parts and plans involved with Medicare. And with the billions of dollars spent every year on advertising the plans, it certainly does not get any easier.

The first thing to understand is that there are two main options for your Medicare coverage. These options are Original Medicare (usually accompanied by a Medicare Supplement) which is made up of Part A (Hospital Coverage) and Part B (Medical Coverage), or Medicare Advantage which is also known as “Part C”.

Most people that go the Original Medicare route also buy a Medicare Supplement, because there are large out of pocket costs with Original Medicare by itself.

So, let’s break down the two main options for your Medicare coverage: Medicare Supplements, and Medicare Advantage.

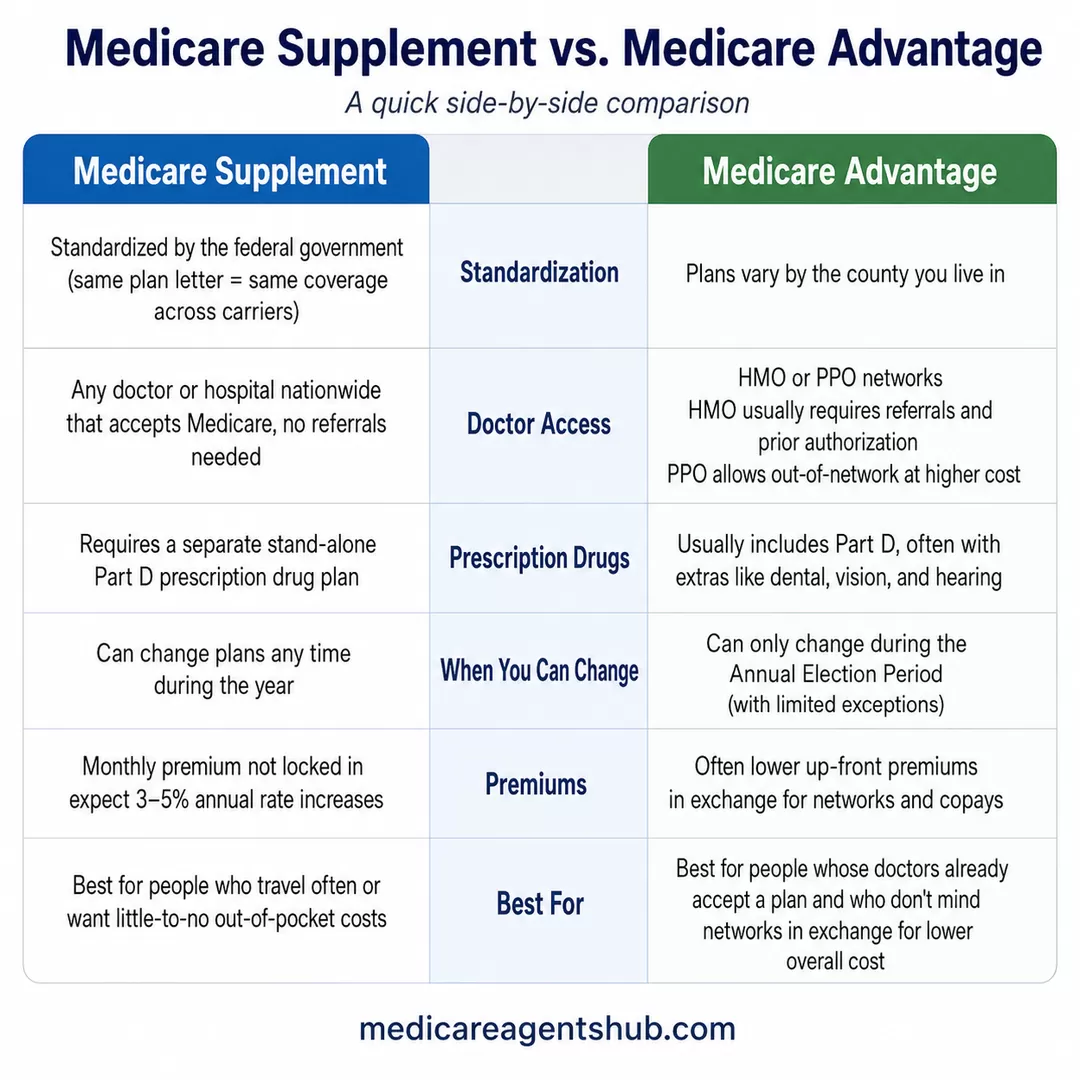

Medicare Supplements

A Medicare Supplement plan, also known as a Medigap plan (just to make it more confusing), is an insurance policy that supplements your Original Medicare (Parts A & B). The supplement helps pay the portion of Medicare costs that Original Medicare does not cover, such as the 20% coinsurance in Part B, and the large deductible in Part A.

Since Prescription Drugs are not covered in Part A or Part B of Medicare, the supplement does not cover prescriptions either. The supplement only covers what Original Medicare covers. Therefore, you will need a separate stand along Prescription Drug plan to cover prescription drugs, if desired.

Key features of Medicare Supplements

Monthly rates vary from carrier to carrier, so it is important to shop around.

- A plan with the same letter is the same from one insurance company to the next. This is because the plans themselves are standardized by the federal government, even though they are sold by private insurance companies.

- The monthly rate is not locked in. You can and should expect the premium to rise over time. 3-5% per year is not unusual.

You can go to any doctor, any hospital, anywhere in the United States, as long as the provider accepts Medicare.

- Referrals are not needed to see a specialist.

- Coverage outside the United States does exist with most Medicare Supplements but is limited.

You can apply for a new Medicare Supplement at any time of the year — you are not restricted to the Annual Election Period (AEP).

- Important: unless you are inside your 6-month Medigap Open Enrollment Period or qualify for a guaranteed issue right, the insurance company can ask you health questions (medical underwriting) and either deny your application or charge a higher premium. Do not drop your current plan assuming you can easily replace it.

Medicare Supplements are ideal for people that travel often, or just want the peace of mind of having little-to-no out-of-pocket costs.

Medicare Advantage

Medicare Advantage, also known as Part C, is the privatized version of Medicare. It acts as an “all-in-one” alternative to Original Medicare.

The plans incorporate Part A, Part B, and usually Part D of Medicare. Sometimes, the plans offer additional benefits above and beyond that of which Original Medicare offers, such as coverage for dental, vision, and hearing.

Key features of Medicare Advantage plans

Plans vary based on the county you live in

Plans have doctor and hospital networks, usually HMO or PPO

- With an HMO you will need a referral to see a specialist and will require “prior authorization" before certain procedures more often than with a PPO.

- PPO’s do not require referrals to see a specialist and offer the convenience of being able to go “out of network” to see more doctors, usually at a higher out of pocket expense.

You can only (with a few exceptions) change coverage during the Annual Election Period (AEP)

Advantage Plans are ideal for people whose doctors already accept a plan, and don’t mind having networks in exchange for, often, lower overall cost.

Be sure to confirm any doctor you want to see accepts the plan before enrolling, and that your prescription drugs are covered as well.

Is one option better than the other?

To say one option is always better than the other would be malpractice on anyone’s behalf. What you must do is to consider your own individual needs, budget, and risk tolerance.

That being said, we came up with a few questions to ask yourself to help you determine which route is better for you:

- Is keeping all your doctors a priority for you?

- Does the idea of getting referrals to see a specialist stress you out?

- Do you travel a lot?

- Are you comfortable with a monthly premium?

- Does the idea of having copays stress you out?

- Are you ok with potentially buying additional coverage for prescription drugs, dental, or vision coverage?

The above questions should be “yes,” “no,” or “Depends.”

If you said “yes” to 4 or more of the above questions, then a Medicare Supplement is probably right for you. If you said “yes” to less than 4 then a Medicare Advantage plan is probably right for you.

Of course, this test is a simple analysis and shouldn’t be substituted for a deep risk analysis. But meant to at least start the conversation and point you in the right direction and starting your Medicare journey. Working with a knowledgeable insurance broker is always the best way to assess your needs and manage your risk.

Summary

There are numerous options to consider for your Medicare coverage. But, having a thorough understanding of the two main options will help you be able to properly protect your health, and financial life. Do not allow yourself to be swayed by a smooth-talking insurance salesman, or a charming celebrity endorser.

There are many plans that seem “too good to be true.” Be sure to look deeper than the “freebies” these plans seem to offer. Health insurance is more than a $50 a month over-the-counter gift card.

Likewise, do not allow yourself to become over-insured either. Understanding the real costs of each option can help. You do not want to be spending your entire Social Security check on health insurance, copays, and prescription drug costs.

Trust your instincts and do what is right for you and your family.

About the Author: David Walls has been serving the Medicare community since 2012; focusing on helping individuals protect their retirement with Medicare Supplements, Medicare Advantage, and Medicare Part D prescription drug plans in the State of Florida.