Understanding Dental Coverage in Medicare Advantage Plans

-

Last Updated July 31, 2026

Dental care can be one of the most confusing parts of Medicare. Many seniors are surprised to learn that Original Medicare doesn’t cover most dental services. That includes routine checkups, cleanings, fillings, dentures, and even procedures like root canals or crowns (Medicare.gov confirms this exclusion). For coverage like that, many turn to Medicare Advantage plans.

Medicare Advantage, also known as Medicare Part C, is offered by private insurance companies approved by Medicare. These plans must include everything covered by Original Medicare (Parts A and B), but most also offer extra benefits, dental being one of the most popular—alongside vision benefits like cataract surgery coverage.

So do Medicare Advantage plans cover dental? In most cases, yes. But what’s actually covered, and how much you’ll pay out of pocket, depends heavily on the plan you pick.

What Dental Services Are Covered by Medicare Advantage Plans?

Most Medicare Advantage plans offer at least some dental coverage, but what’s included can vary widely. At the basic level, many plans cover preventive care, which usually includes:

- Routine cleanings

- Oral exams

- Yearly X-rays

These are the services that help you maintain oral health and catch problems early.

Beyond preventive care, some plans also offer coverage for more advanced procedures. This might include fillings, simple extractions, root canals, crowns, dentures, or implants. However, just because something is listed as a covered service doesn’t mean it’s fully paid for.

Here’s where it gets tricky. Every plan has its own set of rules for dental coverage. These kinds of plan-specific quirks are among the most common Medicare frustrations seniors face. Some might only pay a portion of the cost. Others may cover certain services only once every few years, and almost all of them set an annual dollar limit on how much dental care they’ll pay for.

Annual Dental Limits in Medicare Advantage

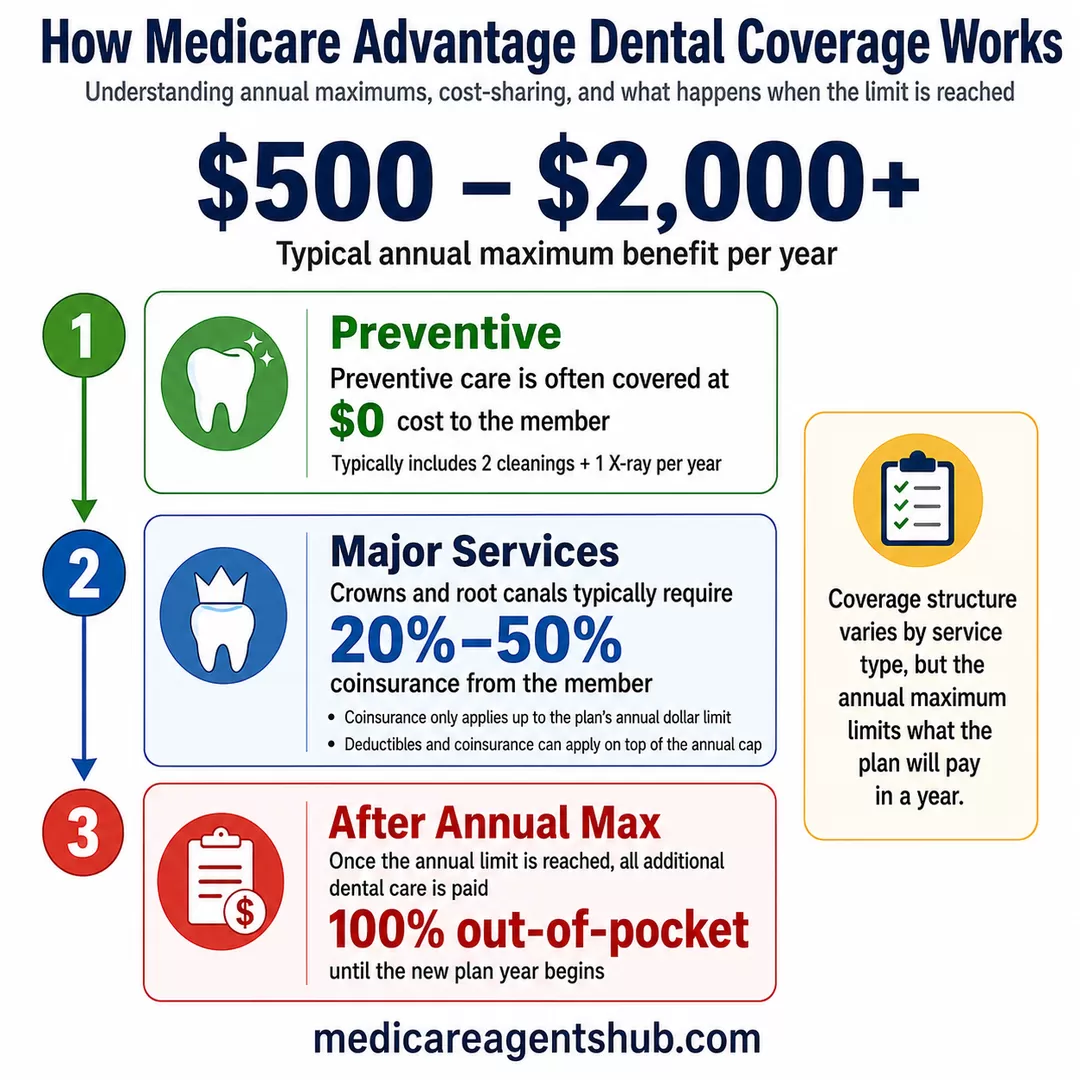

A common feature of Medicare Advantage dental benefits is the annual maximum. This is the total amount the plan will contribute toward dental care in a given year. It can range from as low as $500 to as high as $2,000 or more, depending on the insurer and the plan.

For example, a plan might give you two cleanings and one X-ray per year with no cost to you. However, if you need a crown, root canal, or dentures, you may have to pay 20% to 50% of the cost, and that’s only up to your plan’s yearly limit. Once that limit is reached, any additional dental care is paid out-of-pocket until the new plan year begins.

Many plans also include cost-sharing like deductibles or coinsurance. So while a dental benefit may exist, it doesn't always mean the service is free or even inexpensive. This is where it’s helpful to compare not just whether dental is offered, but how it works.

Waiting Periods for Major Dental Services

Something a lot of new enrollees miss: many Medicare Advantage dental benefits come with waiting periods before major services kick in. Preventive care (cleanings, exams, X-rays) is usually available right away, but coverage for crowns, dentures, and other major work might not start for 6 to 12 months after enrollment.

If you know you need bigger dental work soon, check the plan’s Evidence of Coverage for the waiting period rules before you enroll. Otherwise you could end up paying full price on a procedure you thought was covered.

The Importance of Dentist Networks

One of the biggest frustrations seniors face is finding a dentist who accepts their Medicare Advantage plan. Most plans have a provider network, this means you can only use certain dentists or dental offices if you want your benefits to apply.

HMO plans usually require you to stay in-network, while PPO plans might allow out-of-network visits, but at a higher cost. Some plans offer more flexibility, but it’s always smart to check if your preferred dentist is covered before enrolling.

Even when a plan looks good on paper, network restrictions can be a deal-breaker. A benefit is only helpful if you can actually use it.

Don’t Be Misled by Marketing

Many seniors hear about dental coverage from TV commercials or flyers that arrive in the mail. These ads often highlight free or low-cost dental care, but they rarely tell the full story. Some leave out important details about limits, exclusions, and provider access.

Always look beyond the advertising. Ask for the plan’s Summary of Benefits or the Evidence of Coverage (EOC). These documents explain exactly what services are covered, how much they cost, and what the limitations are. If something isn’t listed in those documents, don’t assume it’s covered.

It’s also wise to find a licensed Medicare advisor who can break down the differences between plans and help you find one that fits your dental needs.

Is a Standalone Dental Plan a Better Option?

Sometimes, Medicare Advantage dental benefits aren’t enough, especially if you expect to need major dental work. In that case, a separate dental insurance plan might make more sense.

Standalone dental plans tend to offer higher annual limits and broader coverage, though you’ll pay an extra monthly premium. They can be a good supplement to Medicare Advantage if you want more peace of mind or flexibility.

However, this also means coordinating between two insurance companies and paying for two plans. It’s not always necessary, but it’s worth considering if your Medicare Advantage plan falls short on dental.

Comparing Medicare Advantage Dental Plans

When comparing plans, focus on what services are covered, how often you can use them, what they’ll cost you, and whether your dentist is in-network. Getting in touch with a Medicare Broker is always a good way to make sure this is drawn out well. Here’s a quick comparison example:

| Feature | Option A | Option B |

|---|---|---|

| Annual Max | $1,000 | $2,000 |

| Preventive Services | 100% covered | 100% covered |

| Your Coinsurance for Major Services | 50% | 20% |

| Dentist Network | Local only | National PPO network |

This kind of side-by-side review makes it easier to see the real value of a plan, beyond just the monthly premium. Remember: a lower coinsurance percentage means you pay less out of pocket for major work.

FAQs

I picked a Medicare Advantage plan because of the dental and now I found out it only covers cleanings. Why didn't anyone tell me this upfront?

With Medicare Advantage plans or Part C, it is difficult when there are generalizations that the plans include dental coverage. It is really important to know what coverage is included with each of the plans. Worse yet, over the years, the high profile celebrities come in and advertise "free" benefits and may share details that licensed, appointed and certified agents cannot and many would not say that are advertised on T.V. Although there have been attempts at regulating what is advertised on T.V., it is important to identify and understand the details of the plans according to the Plan ID.Medicare itself does not include dental coverage. It is considered to be a value added benefit. It can be added to Part C or Medicare Advantage plans. Insurance carriers can choose to offer discount coverage which many do not consider true dental coverage, or can offer just preventative or basic coverage, and some opt to include more comprehensive coverage.

The "Evidence of Coverage" will reveal the details of the coverage which can be found on the insurance carriers website, Medicare.gov, and agents should be able to provide or send the evidence of coverage or summary of benefits documents that will outline the coverage.

As legislation has changed and insurance carriers evaluate utilization and rising healthcare costs, insurance carriers have had to adjust what benefits can be offered or have had to place maximum limits for items such as dental as well as vision and hearing coverage that may be added to plans. The Value Based Insurance Designs are sunsetting at the end of 2025 that were instituted in 2017. This has prompted insurance carriers to reevaluate benefits that may be included in the plans.

My Medicare Advantage plan covers dental, but I can't find a dentist who accepts it. Is this a common problem?

Yes, this is an common problem. Many seniors find that while their plan "includes" dental, the actual list of dentists who accept it is surprisingly small. This often happens because many dentists feel the reimbursement rates are too low, or they aren't part of the specific network your insurance uses.Here is the best advice to help you find a provider:

Search by the "Network Name," not just the Plan: Your insurance might be through one company, but they often use a third-party dental specialist like DentaQuest or Delta Dental. When calling a dentist, ask if they take that specific network name—they are much more likely to recognize it than your general Medicare Advantage plan name.

Use the Official "Find a Dentist" Tool: Don't rely on old paper booklets. Use the live online search tools from your insurer—whether you're with Aetna, Humana, or UnitedHealthcare—as these are updated more frequently.

Check for "Out-of-Network" Coverage: If your plan is a PPO, you might not be strictly limited to a list. You can often see any licensed dentist you like; you’ll just pay a bit more out of pocket while the plan still covers a portion of the bill.

Consider a Standalone or Discount Plan: If your current network is just too restrictive, you might look into a standalone dental plan or a "dental discount plan." Many local dentists prefer these because there is far less paperwork involved than with Medicare Advantage.

I have Original Medicare, and I'm wondering if I'd save more on my dental cleanings if I switched to a Medicare Advantage plan instead.

Original Medicare does not cover routine dental care including cleanings, fillings, or dentures. Many Medicare Advantage plans include built-in dental benefits with coverage for cleanings, exams, and sometimes even major services. Whether you’ll save depends on how often you use dental care and the plan’s annual maximums, provider network, and copays — so it’s worth comparing your current out-of-pocket dental costs with what a local Medicare Advantage plan offers.Final Thoughts

Dental coverage under Medicare Advantage can be helpful, but it’s rarely one-size-fits-all. Each plan has its own strengths and weaknesses, and the fine print matters. If you only need cleanings and exams, a basic plan might do the job. But if you expect more serious dental work, you’ll want to look deeper.

The best step is to work with a trusted Medicare advisor who can walk you through your options and help you find a plan that meets your personal health and financial needs. Don’t wait until you’re in the dental chair with a surprise bill, get ahead of it now by understanding what your plan really offers.