Turning 65 and New to Medicare: What To Do Next

-

Last Updated July 20, 2026

Written by Charles Wheeler

Medicare Broker Licensed in MA, CT, FL & 3 other states

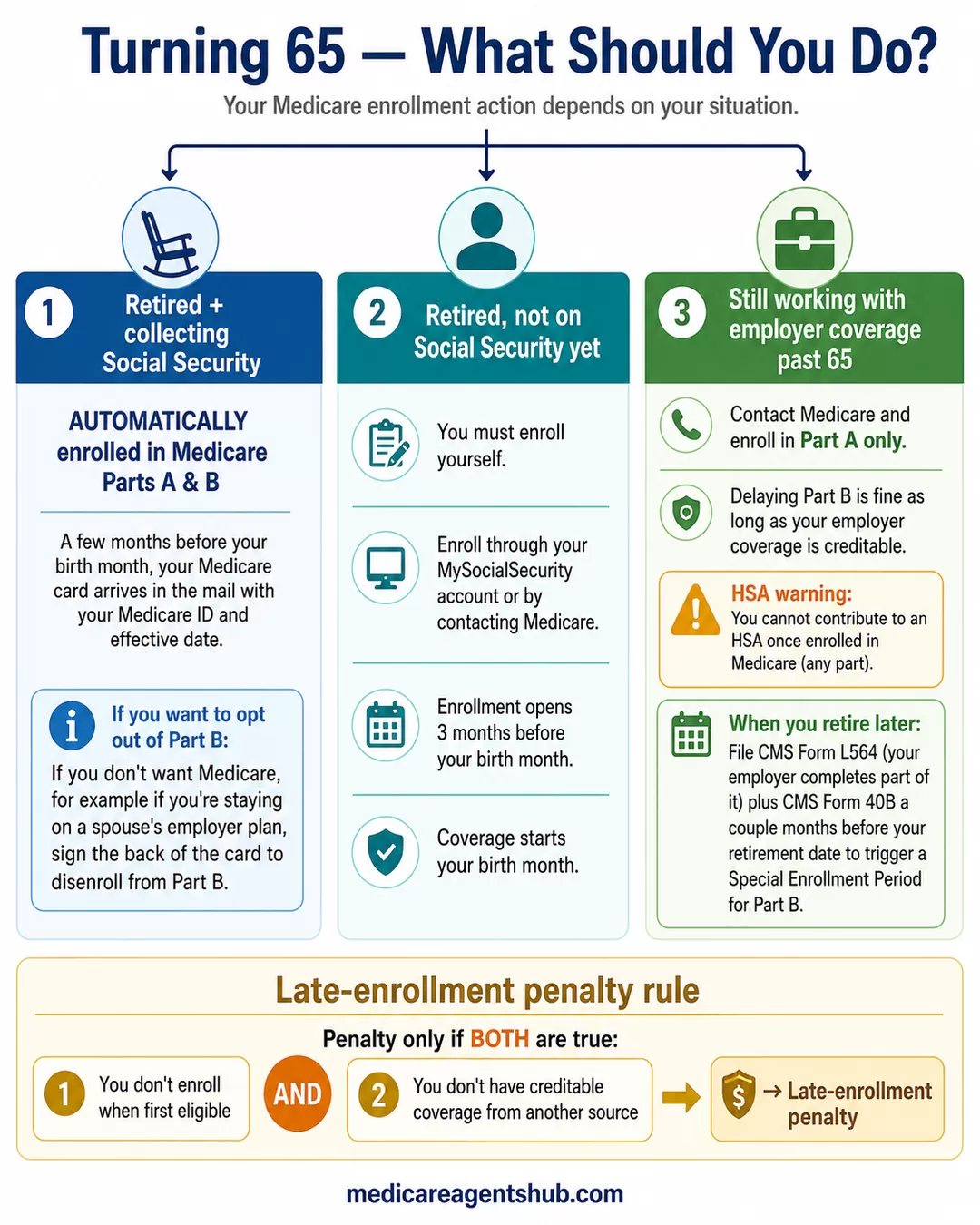

The time has come, you are turning 65 and eligible for Medicare. This is called your Initial Enrollment Period. Most people dread this news as they feel they are getting old, but the truth is these are the "golden years" and should be the most enjoyable time of your life. That being said, now you need to figure out what to do about Medicare. It is very confusing and everyone's situation is different. This article will cover a few different scenarios for Medicare enrollment.

I am already retired...

If you are already retired AND collecting Social Security, congratulations! A few months ahead of your birth month you will be AUTOMATICALLY enrolled in Medicare A and B. Among the piles of literature you receive from health insurance companies, you will be sent a card in the mail showing your Medicare ID# and effective dates (the month you turn 65). If you plan on using Medicare as your health insurance moving forward you do not need to take any further action. You will simply need to understand your secondary plan options, such as Medicare Supplement vs. Medicare Advantage. It is best to consult a Medicare broker to help guide you through the myriad of options available to you. Be aware that the plan type you choose during your IEP can have long-term consequences; some agents caution that picking Medicare Advantage at 65 may limit your options later.

If for some reason you DO NOT want Medicare as your health insurance plan. For example, if your spouse is going to continue to carry you on employer coverage, then you need to decline Part B by following the instructions included in your "Welcome to Medicare" packet, or by contacting Social Security directly before your Part B coverage start date. (Note: current Medicare cards no longer include a signature line for opting out of Part B.) It is always smart to compare employer coverage to Medicare as in some instances it may make sense to enroll in Parts A/B. Again, consult a Medicare broker to help you make these comparisons.

If you are retired but NOT collecting Social Security then if you want Medicare coverage you will have to enroll in Medicare via your MySocialSecurity account or by contacting Medicare. You can enroll for your benefits 3 months ahead of your birth month. (i.e. if you are born in May, you can begin your enrollment February 1st.) Your coverage still will not start until your birth month but nonetheless you can start the enrollment process.

What happens if I am already retired and collecting Social Security when I turn 65?

If you are already retired AND collecting Social Security, congratulations! A few months ahead of your birth month you will be AUTOMATICALLY enrolled in Medicare A and B. Among the piles of literature you receive from health insurance companies, you will be sent a card in the mail showing your Medicare ID# and effective dates (the month you turn 65). If you plan on using Medicare as your health insurance moving forward you do not need to take any further action.I am still working...

A large group of people continue working past age 65 until full retirement age or beyond, this is common place. Independent of how long someone is working they are typically eligible for Medicare at age 65. If someone plans on continuing to work past 65 and wants to keep their employer coverage then they simply need to contact Medicare and enroll in JUST Part A. In a lot of cases you are AUTOMATICALLY enrolled in Part A when turning 65 but nonetheless it is a wise move to contact Medicare and make sure they have you enrolled. In many cases people are continuing to carry a spouse or children on their employer coverage and as such delaying Medicare makes perfect sense.

Again, it still makes sense to compare your employer coverage to Medicare benefits. In some cases people have been able to save money AND get more comprehensive coverage by going on to Medicare. One thing to note is that if you are continuing to work and contribute to an HSA, you CANNOT contribute to an HSA while on Medicare. Ultimately, as explained earlier, contact a Medicare broker to help you understand your options as well as the pros and cons.

Will I be penalized?

A big concern for people as they turn 65 is if they DO NOT enroll in Medicare they will be penalized. It is a common misnomer. The truth is someone will be penalized if (1) They do not enroll in Medicare when first eligible AND (2) They DO NOT have creditable coverage from another source (employer, spousal coverage, etc). If you continue to work, or have insurance through your spouse, (as long as it is creditable) you WILL NOT be penalized. In most cases employer coverage meets the standard of creditable coverage but double check with your HR department.

Will I be penalized if I do not enroll in Medicare when I turn 65?

A big concern for people as they turn 65 is if they DO NOT enroll in Medicare they will be penalized. It is a common misnomer. The truth is someone will be penalized if (1) They do not enroll in Medicare when first eligible AND (2) They DO NOT have credible coverage from another source (employer, spousal coverage, etc). If you continue to work, or have insurance through your spouse, (as long as it is creditable) you WILL NOT be penalized.I didn't take Medicare at 65 and am now retiring...

Congratulations, you have worked hard to get here. Now, a few things need to happen AHEAD of your retirement date. First, once you know the date you are retiring you will need to apply for Medicare Part B. You will need to create a "special enrollment period" as you are (most likely) outside your turning 65 enrollment period.

You will need to fill out Medicare Forms: CMS L564 and CMS 40B

- CMS L564 is partly filled out by you and then the remainder if completed by your employer. It explains that you are retiring and losing employer coverage.

- CMS 40B is your application for Medicare Part B. It, along with CMS L564, explains to Medicare that you are losing coverage through your employer and now need to elect your Medicare Part B benefits.

Typically, you complete and submit these forms a couple months ahead of your retirement date. Your Medicare Part B starts the 1st of the month following the end of your employer benefits (typically employer benefits extend to the end of the month). For example, if you are retiring on September 4th your employer benefits would extend to September 30th and your Medicare Part B (along with A) would kick in on October 1st, leaving no gap in coverage.

Make sure to keep your employer health insurance card for 6 Months-1 Year as CMS (Medicare) may not have recognized that you had employer coverage post-65 and will assess a penalty. The penalty can easily be appealed by sending in a form and a copy of your employer health insurance card.

What do I need to do if I didn't take Medicare at 65 and am now retiring?

A few things need to happen AHEAD of your retirement date. First, once you know the date you are retiring you will need to apply for Medicare Part B. You will need to create a 'special enrollment period' as you are (most likely) outside your turning 65 enrollment period. You will need to fill out Medicare Forms: CMS L564 and CMS 40B. CMS L564 is partly filled out by you and then the remainder is completed by your employer. It explains that you are retiring and losing employer coverage. CMS 40B is your application for Medicare Part B. It, along with CMS L564, explains to Medicare that you are losing coverage through your employer and now need to elect your Medicare Part B benefits.Conclusion

At the end of the day, whether you are turning 65 or retiring, Medicare can be extremely confusing. For a broader overview, see our Medicare 101 guide. Some states also have unique considerations that make the process even more nuanced. If you are in the Sunshine State, for instance, check out what Florida residents need to know about Medicare at 65 for guidance tailored to that market. Medicare brokers are there to help guide you through your options and explain, what (if anything) needs to be done.