5 Medicare Myths Some Agents Still Believe

-

June 17, 2026

Medicare has more than 60 million beneficiaries, a rulebook that changes every year, and a workforce of licensed agents who interpret those rules for the public. Most of them get it right. But when you read thousands of agent answers side by side, patterns emerge that should concern anyone shopping for coverage: agents confidently stating things that other agents, correctly, dispute.

This is not about bad agents. It is about a system complex enough that even experienced professionals sometimes carry outdated or incomplete information. The difference between a good agent and a great one often comes down to details that cost you nothing to verify, if you know what to ask.

Myth 1: "You Have Six Months From Turning 65 to Get a Medigap Plan Without Underwriting"

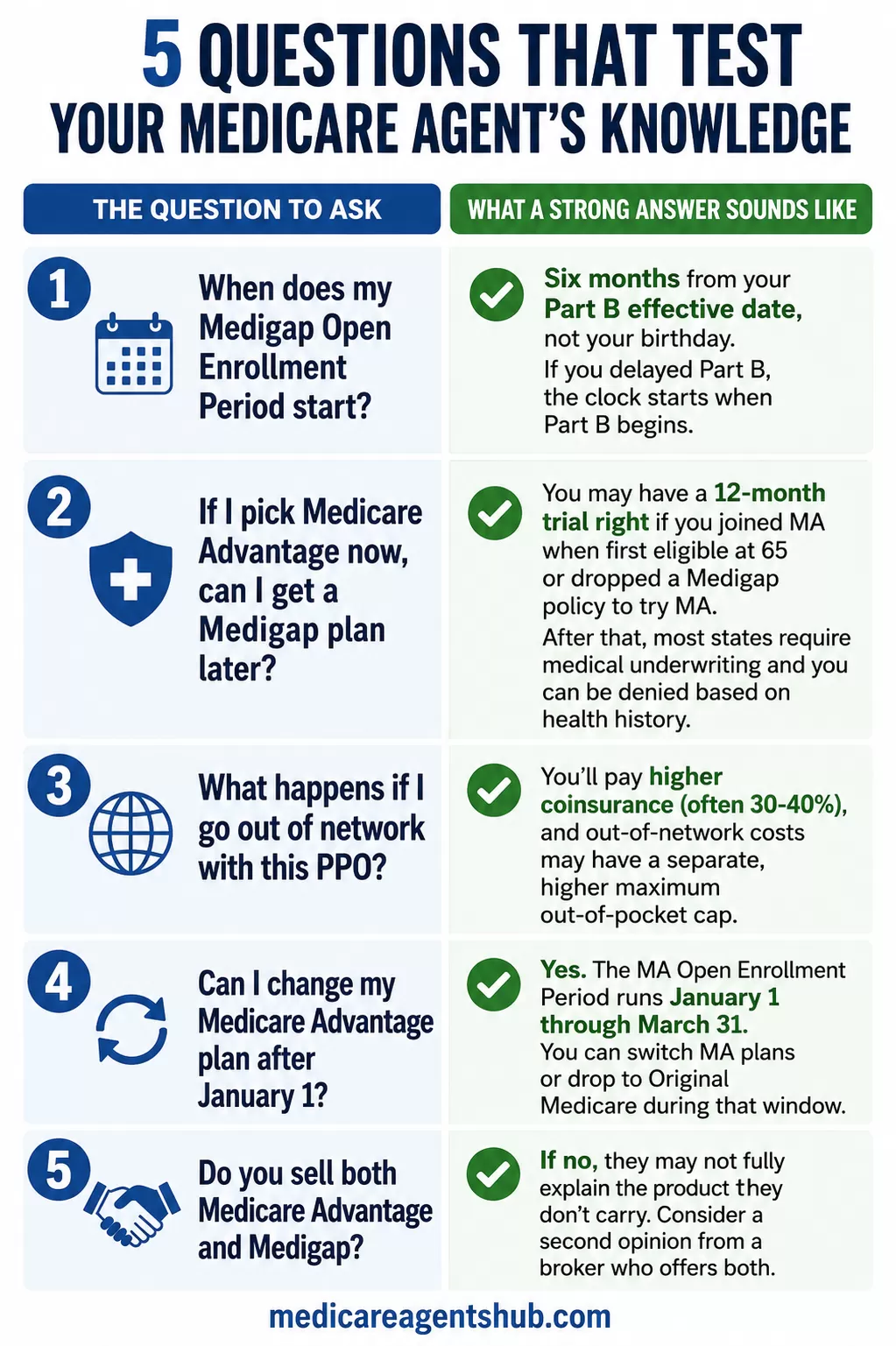

This is one of the most common statements in the Medicare agent community, and it is almost right, which makes it dangerous. The actual rule is that your six-month Medigap Open Enrollment Period begins the first month you are both 65 or older AND enrolled in Medicare Part B. For many people, that lines up with turning 65. But for anyone who delays Part B because they are still working with employer coverage, the clock does not start at their birthday. (Source: Medicare.gov)

We found agents across our Q&A platform describing this window in at least four different ways. Some said it starts "three months before your 65th birthday." Others said "the month you turn 65." A few correctly identified the Part B effective date as the trigger. The distinction matters enormously for anyone who retires at 67 or 70 and assumes their Medigap window closed years ago.

An agent who works with a lot of people aging out of employer plans will know this cold. An agent who primarily sells Medicare Advantage may not think about it often enough to get the nuance right. When you are interviewing agents, ask specifically: "When does the Medigap Open Enrollment Period start for someone who delayed Part B?" The right answer references the Part B effective date, not your birthday.

What is Guaranteed Issue for Medicare Supplement plans, and when does it apply?

Guaranteed Issue (GI) for a (Medigap/Medicare Supplement) plan means an insurance company must sell you a policy, cannot deny you coverage, cannot charge you more because of health conditions, and cannot impose waiting periods for pre-existing conditions. Medigap works alongside **Original Medicare** to help cover out-of-pocket costs like deductibles and the 20% Part B coinsurance. The strongest GI protection occurs during your one-time, six-month Medigap Open Enrollment Period, which begins when you are age 65 or older and enrolled in Medicare Part B.You may also qualify for Guaranteed Issue in certain special situations, such as losing employer coverage, your **Medicare Advantage** plan leaving Medicare or your service area, or exercising a 12-month “trial right” after first joining Medicare Advantage. In these cases, you typically have 63 days to apply for certain standardized Medigap plans without medical underwriting. Outside of these protected periods, insurers in most states can require health screening and may deny coverage or charge higher premiums.

Myth 2: "You Can Always Switch Back to a Medigap Plan From Medicare Advantage"

When we asked agents whether someone can leave Medicare Advantage and return to Original Medicare, the answers ranged from a simple "yes, no penalties" to detailed explanations of underwriting risk. Both ends of that spectrum are technically true in isolation, and dangerously incomplete on their own.

Yes, you can always return to Original Medicare during the Annual Enrollment Period or the Medicare Advantage Open Enrollment Period. There is no penalty for that switch. But returning to Original Medicare without a Medigap plan leaves you exposed to 20% coinsurance on Part B services with no cap. The real question most people are asking is whether they can get back to the combination of Original Medicare plus a Medigap supplement, and that is where underwriting enters the picture.

Outside of a few narrow windows, Medigap carriers in most states can ask health questions, charge more based on your medical history, or deny you outright. The most important of these windows is the Medicare Advantage Trial Right: you may have a 12-month trial right if you joined Medicare Advantage when first eligible for Medicare at 65, or if you dropped a Medigap policy to try Medicare Advantage for the first time. Outside those situations, switching back to Original Medicare does not automatically guarantee you can buy the Medigap plan you want without underwriting. (Source: Medicare.gov)

Several agents on our platform conflated this trial right with a general right to return anytime. Others omitted the trial right entirely and jumped straight to "you'll need underwriting." The agents who get it right explain both sides: the trial right exists but is narrow, and outside of it, poor health can block you from getting a supplement entirely.

If we choose a Medicare Advantage plan and later regret it, can we go back to Original Medicare without penalties?

According to the 2026 Medicare and You Handbook, there are only a few, very limited circumstance which will allow a person to enroll into a Medicare Advantage Plan and return to Original Medicare and obtain a Medicare Supplement with no health underwriting (answer health questions, height/weight, pharmacy check, etc) within a 12-month period. The only other guaranteed enrollment without medical underwriting is if the Medicare Advantage Plan was involuntarily terminated from the person. Meaning the plan was cancelled by the company. The person receives a letter from the company which states the plan is ended and they are then allowed to select a Medicare Supplement for a limited time with no health questions.In most cases not listed above, if a person has an Advantage Plan and experiences poor health and desires to get a Medicare Supplement, they may not be able to obtain the Supplement at that time, or most likely, not in the future.

However, if a person is Dual Eligible (eligible for both Medicare and Medicaid) and maintain their Medicaid eligibility, they may keep their Advantage Plan because if they follow the plan guidelines, their medical care costs should be covered by Medicaid and their Advantage Plan.

Myth 3: "A PPO Gives You the Flexibility to See Anyone"

If there is one word that gets overused in Medicare Advantage conversations, it is "flexibility." Agents consistently describe PPO plans as giving beneficiaries the freedom to see providers outside their network. That is technically accurate. What many agents fail to explain is what that out-of-network access actually costs. (Source: Medicare.gov)

We reviewed dozens of agent answers to a question about PPO out-of-network billing frustrations. The pattern was striking: the majority of agents confirmed that PPOs allow out-of-network visits but charge significantly more for them. Some agents described out-of-network coinsurance running 30% to 40% of the provider's charges. Several noted that most PPO holders would actually save money in an HMO because they never use the out-of-network benefit intentionally.

The distinction one agent drew is worth memorizing: a PPO gives you permission to go out of network, not price protection. When you do, the insurer pays a "reasonable" amount and the provider can bill you the rest. If you use out-of-network providers often, the flexibility is an expensive illusion.

I picked a PPO for the flexibility, but now every time I go out of network the bills are outrageous. What's the point of even having a PPO?

Great question — and honestly, a really common frustration.Here's the truth: a PPO does give you the flexibility to go out of network. That's literally the point. But flexibility doesn't mean free — it means you have options, and with those options comes cost-sharing.

What most people don't realize is that PPO plans are designed so you can go out of network in an emergency or when your specialist isn't in-network — not so you routinely bypass your network and wonder why the bill is high.

Here's what a licensed agent would have walked you through before you enrolled:

What your in-network costs look like vs. out-of-network

Which providers and specialists you see most — and whether they're in-network

Whether a PPO was actually the right fit for how you use your insurance

This is exactly why working with a licensed agent matters. It's not just about picking a plan — it's about picking the right plan for your life, your doctors, and your health needs.

A PPO might still be right for you. But the cost is a feature, not a bug — and knowing when to use that out-of-network access (and when not to) makes all the difference.

👉 If you're unsure your plan is the right fit, reach out. That's what we're here for.

The question to ask your agent: "What is the out-of-network coinsurance on this PPO, and does the plan have a separate out-of-network maximum out-of-pocket?" Many PPO plans carry two different MOOP numbers, one in-network and one out-of-network, and the out-of-network cap can be thousands of dollars higher. If your agent cannot quote those numbers, they are selling the plan on a word rather than on its actual cost structure.

Myth 4: "There Is No Trap With Medicare Advantage"

We asked agents directly: "What is the trap of Medicare Advantage plans?" The responses split into two camps. One group pushed back on the word "trap" entirely, arguing that Medicare Advantage plans are legitimate, well-regulated, and suitable for many beneficiaries. The other group described a specific and well-documented risk: after your initial enrollment period, switching from Medicare Advantage to a Medigap supplement requires medical underwriting in most states.

Both camps make valid points, but only one is giving the full picture. The agents who dismiss the "trap" framing are correct that Medicare Advantage plans must cover everything Original Medicare covers. But the agents who describe the underwriting risk are addressing the real concern most consumers have: what happens if I get sick and want to change?

The answer is specific and important. You may have a 12-month trial right if you joined Medicare Advantage when first eligible for Medicare at 65, or if you dropped a Medigap policy to try Medicare Advantage for the first time. After that window closes, if you want to switch to Original Medicare with a Medigap plan, carriers can evaluate your health history. If you have developed cancer, heart disease, diabetes, or other chronic conditions during your time on Medicare Advantage, you may be declined for a Medigap policy or offered one at a substantially higher premium. That is the mechanism behind what people call the "trap," and glossing over it does a disservice to consumers making a decades-long coverage decision at age 65.

What is the trap of Medicare Advantage plans?

I wouldn’t call it a “trap,” but there are a few things people don’t always realize going in.The biggest one is that Medicare Advantage plans are network-based. You may need to stay within a specific group of doctors and hospitals, and referrals can be required. That’s not always an issue—until you need care outside the network or want more flexibility.

Another thing is the cost structure. These plans often have low or even $0 premiums, but you’re paying as you use services through copays and coinsurance. If you have a more serious health year, those costs can add up quickly.

Also, switching later isn’t always as easy as people think. In many cases, moving from a Medicare Advantage plan back to a Supplement can require health underwriting, depending on your situation.

For some people, Medicare Advantage works very well. But it’s important to understand the trade-offs upfront so you’re not surprised down the road.

Myth 5: "You Can't Change Your Medicare Advantage Plan After You Enroll"

On the flip side, some agents overstate how locked in you are once you pick a Medicare Advantage plan. We found agents telling consumers they are stuck until the next Annual Enrollment Period, which runs October 15 through December 7. That is incomplete.

The Medicare Advantage Open Enrollment Period (MA OEP) runs from January 1 through March 31 every year. During that window, anyone already enrolled in a Medicare Advantage plan can switch to a different Medicare Advantage plan or drop Medicare Advantage entirely and return to Original Medicare. (Source: Medicare.gov) This is not a well-known enrollment period, and some answers in our Q&A database failed to mention it when addressing related questions.

Beyond the MA OEP, there are Special Enrollment Periods triggered by specific events: moving out of your plan's service area, losing Medicaid eligibility, qualifying for a chronic condition Special Needs Plan, or your plan's star rating changing. An agent who tells you flatly that you cannot change plans until fall is missing at least two enrollment windows and possibly more.

What's a common Medicare myth that even some agents still believe?

“You can’t change your Medicare Advantage plan after you enroll.”The truth: While it's true that you're generally locked in for the year after choosing a Medicare Advantage (Part C) plan during Annual Enrollment (Oct 15–Dec 7), there's a lesser-known window:

Medicare Advantage Open Enrollment Period (MA OEP): Jan 1–Mar 31

During this time, beneficiaries already enrolled in a Medicare Advantage plan can:

Switch to a different Medicare Advantage plan, or

Drop their Advantage plan and return to Original Medicare (and add a Part D plan if they want).

Many agents forget or overlook this option, which could help clients who regret their decision, dislike their network, or have unexpected issues with coverage.

Knowing this sets great agents apart — and gives clients peace of mind.

Why These Myths Persist

Medicare agents are not required to sell every type of product. Some are contracted only with Medicare Advantage carriers. Others specialize exclusively in Medigap supplements. This creates a structural bias: agents tend to know the rules best for the products they sell, and they may oversimplify or skip details about products they do not offer.

Another misconception flagged on our Q&A platform: some agents believe Medicare stays primary when a client signs up for a Medicare Advantage plan. It does not. The private company must provide the same benefits, but Medicare is no longer primary, which means the consumer is subject to that company's network rules and processes.

What's a common Medicare myth that even some agents still believe?

The common belief that I see some agents make is believing that Medicare stays primary when a client signs up for an MA plan. This is just not true. The private company must provide the same benefits as Medicare, but Medicare is not primary. This makes the consumer subject to that company's network.None of this means you should avoid working with an agent. Most agents are experienced, ethical, and genuinely committed to finding the right plan for their clients. But knowledge gaps do exist, and they cluster around the boundaries between product types: where Medicare Advantage rules meet Medigap rules, where enrollment periods overlap, and where federal protections end and state-specific rules begin.

Five Questions That Test Your Agent's Knowledge

If you are meeting with a Medicare agent for the first time, these questions will help you gauge whether they understand the full landscape or only the slice they sell.

The Takeaway

The agents who answered our questions most accurately were not always the most experienced or the most credentialed. They were the ones who addressed nuance instead of defaulting to a sales pitch. They mentioned underwriting when talking about Medigap. They distinguished the Part B effective date from a birthday. They named specific enrollment periods instead of saying "you can always change."

You do not need to become a Medicare expert yourself. But you do need an agent who is one. The questions above take less than five minutes to ask, and the answers will tell you whether your agent is working from the full rulebook or a simplified version of it.