The PPO Mirage: Why Agents Say 9 Out of 10 Medicare PPO Holders Would Be Better Off in an HMO

-

May 22, 2026

Ask a Medicare agent whether your PPO is the right plan, and you might not like the answer. Across more than 75 responses to a single question about PPO frustrations on Medicare Agents Hub, agents landed on a remarkably consistent take: most people who buy a Medicare Advantage PPO for "flexibility" don't actually use that flexibility, are getting worse in-network benefits than the equivalent HMO from the same carrier, and would save money by switching.

That's a strong claim. But the reasoning behind it is straightforward, and it comes down to how insurance companies price risk. That doesn't mean PPOs are bad plans, or that every PPO enrollee should switch. But agents say many seniors choose PPOs for theoretical flexibility they rarely use, and pay for it on every claim.

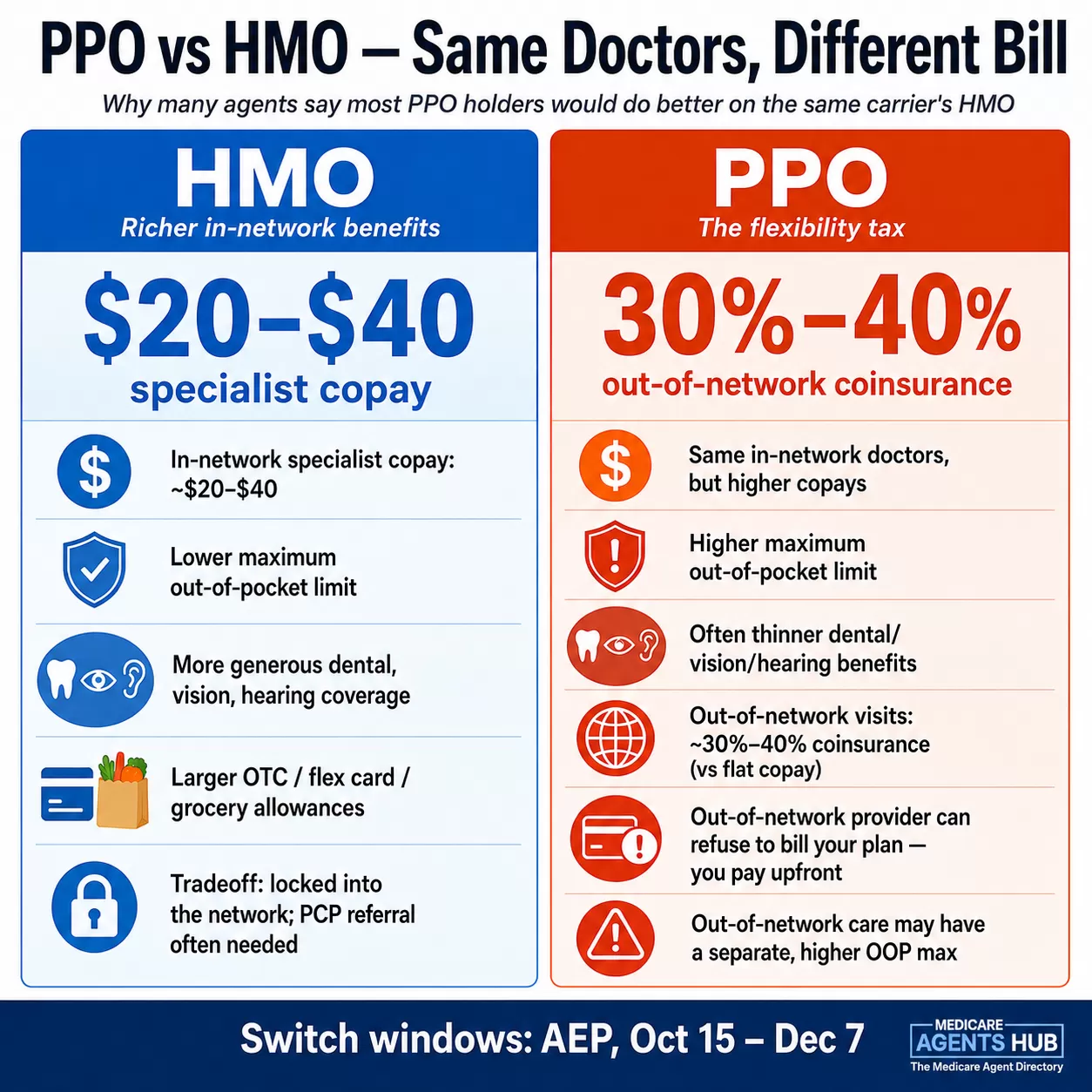

The Insurance Math Behind the PPO Tax

When a carrier offers a PPO, it takes on more financial exposure. The plan has to cover claims from providers who haven't agreed to the carrier's negotiated rates, and those out-of-network bills can be unpredictable. To offset that risk, the carrier does something that most enrollees never think about: it pulls back benefits on everything else.

That means higher copays at the same in-network doctors, higher specialist costs, higher maximum out-of-pocket limits, and often fewer supplemental benefits like dental, vision, and hearing coverage. You're paying a "flexibility tax" on every visit, even when you stay in network.

I picked a PPO for the flexibility, but now every time I go out of network the bills are outrageous. What's the point of even having a PPO?

Steve Brauer's estimate of nine out of ten may sound aggressive, but the pattern holds across dozens of agent answers. The same doctors, the same hospitals, the same lab work, but higher costs on the PPO side of the ledger. And the reason is pure actuarial math: the carrier has to reserve funds for potential out-of-network claims, so the tradeoffs built into Medicare Advantage hit PPO enrollees harder.

Why HMOs Typically Offer Richer Benefits

This is the part that catches most seniors off guard. They assume a PPO is the "better" plan because it costs more or because it has fewer restrictions. But in Medicare Advantage, fewer restrictions usually means fewer benefits.

An HMO plan locks you into a defined network. The carrier knows exactly which providers will be submitting claims and at what rates. That predictability lets the carrier invest more in the plan's benefit structure: lower copays, lower out-of-pocket maximums, richer dental and vision packages, better hearing benefits, more generous over-the-counter allowances.

What's the trade-off between a Medicare Advantage PPO and HMO when it comes to flexibility?

A PPO stands for a preferred provider organization, and what that means is they prefer for you to stay in network with their organization. However, you can go outside of that network. Now, you could be looking at some higher co-pays, co-insurances, and such if you do choose to go outside of the network, so that is definitely something to keep in mind.

Now, an HMO stands for health maintenance organization. One key word I want you to keep in mind when thinking of an HMO is the word "have." With an HMO, you have to have a referral in order to see a specialist. What that means is your primary care doctor has to write your referral in the event that you want to see a specialist.

Okay, now another thing that I want you to keep in mind with an HMO is that you have to stay in the network with the doctors that are inside of that HMO's network. If you do go outside of that network, you are going to have to pay the full price for those services, okay?

Now, one thing to keep in mind is that an HMO is gonna have higher dental, vision, hearing, and flex benefits because they know that you are more likely to stay in their network, okay? So those are some things to consider when choosing between an HMO and a PPO. I hope that helps. If you guys have any questions, don't hesitate to reach out to me. And until next time, y'all, keep it real.

Brianna makes a point that agents across the country echo: HMOs often come with stronger supplemental benefits specifically because the carrier isn't hedging against out-of-network risk. That dental coverage, those vision benefits, the hearing aids, the flex cards and grocery allowances that get advertised during AEP, these tend to be more generous on HMO plans. If you picked a PPO and are wondering why your benefits feel thin compared to what your neighbor got, this is probably why.

Of course, an HMO is only better if its network actually includes the doctors, hospitals, and specialists you use. The richest benefits in the world don't help if you can't see your preferred providers. Always verify your provider list before assuming an HMO switch will work for you.

Out-of-Network Doesn't Mean "Any Doctor You Want"

The biggest misconception about PPOs is that out-of-network coverage means you can see any doctor anywhere and your plan will pick up part of the tab. That's not how it works in practice.

First, the cost-sharing for out-of-network care is steep. Where an in-network specialist visit might cost you a $20 or $40 copay, out-of-network visits often come with 30% to 40% coinsurance, applied against whatever that provider decides to charge, not the plan's negotiated rate. Depending on the provider, the plan, and whether the provider agrees to bill the plan, you may owe substantially more than you expected, and you may have to deal with reimbursement or billing issues yourself.

Second, and this is something agents see constantly, the out-of-network provider can simply refuse to bill your plan at all.

I picked a PPO for the flexibility, but now every time I go out of network the bills are outrageous. What's the point of even having a PPO?

So if you, for instance, are going to get a surgery done normally with a plan that's in network, maybe you'll have a few hundred dollars copay. However, if you're out of network with a PPO, as an example, sometimes with those plans, you'll pay 20, 30, 40, or even higher percentage of that until you hit the maximum out of pocket. Just keep in mind that each plan typically has its own max out of pocket. If it's an in-network versus out-of-network plan, sometimes you'll see two different max out of pockets for plans.

Regarding HMO, typically with HMO plans, you don't have the extra flexibility. However, if you are in a situation that is an emergency, you will be covered regardless if you're an HMO or PPO or not. I hope this helps.

Michael's point about there being "no contract with that specific hospital system" is critical. A PPO gives you the theoretical ability to go out of network, but the provider on the other end has no obligation to participate. They can refuse to submit the claim to your insurer, leaving you to pay the full amount upfront and try to get reimbursed on your own. And out-of-network providers may have a separate, higher maximum out-of-pocket limit on your plan, meaning you could be exposed to thousands more in costs before the plan's cap kicks in.

Agents who deal with real Medicare frustrations from their clients say this scenario plays out more often than you'd think.

When a PPO Actually Does Make Sense

Not everyone is better off in an HMO. Agents are clear about the situations where a PPO earns its keep:

Snowbirds and multi-state retirees. If you split your year between two states, an HMO's local network won't cover your routine care in the second location. A PPO with a national network, or better yet, a Medigap plan paired with Original Medicare, gives you access in both places. This is probably the single most common legitimate use case agents cite for PPOs.

I thought I was covered during my snowbird months in Florida, but apparently not. What kind of plan do I actually need for that?

You actually have several options. Sounds like you have a HMO Advantage plan where you live. One option would be to stay on original Medicare with a supplemental plan. That would allow you access to any provider that accepts Medicare across the country. Another option would be a PPO Medicare Advantage plan if its available in you area. Several national carriers have network providers across the nation and would also provide coverage out of network.If you're a snowbird trying to figure out how Medicare works across state lines, Michael Ryan's answer highlights the key point: a PPO is one option, but a Medicare Supplement might actually be the better fit depending on how much time you spend away from home.

Rural areas with thin networks. In some parts of the country, especially rural counties, the HMO networks are so small that your nearest in-network specialist could be hours away. In those areas, a PPO's out-of-network access isn't a luxury. It's a necessity.

Established specialist relationships. If you have a long-standing relationship with a specialist who isn't in any local HMO network, and switching doctors would genuinely disrupt your care, a PPO lets you keep that relationship (assuming the specialist is willing to bill the plan).

Travelers who aren't snowbirds. Full-time RVers, people who spend extended time visiting family across the country, or anyone whose healthcare needs might pop up far from home. An HMO's emergency-only out-of-area coverage isn't enough for people who are regularly away from their service area.

For everyone else, and agents say this is the majority, the PPO's flexibility goes unused while the benefit reduction hits every single claim.

The HMO-POS Option Most Seniors Never Get Pitched

Between the full lockdown of a standard HMO and the expensive openness of a PPO, there's a plan type that most seniors have never heard of: the HMO-POS, or Health Maintenance Organization with a Point of Service option.

An HMO-POS works like a regular HMO for day-to-day care. You pick a primary care doctor, stay in network, and get the richer benefits that come with managed care. But it adds a limited out-of-network option for situations where you need it, typically at higher cost-sharing but without the full benefit reduction of a PPO.

I signed up for a Medicare Advantage HMO, and I'm wondering if I can see a cardiologist out of network without paying everything myself.

This on can be tricky.Using an HMO plan typically means you would want to stay within the network in order to keep your costs as low as possible. If you see a doctor outside of the network, you could end up paying the full cost for that care. There could be some exceptions if this was an emergent care issue while out of network. Be careful seeing an out of network doctor on an elective basis.

Some HMO plans are Point of Service (POS). A POS plan may allow you go out of network for some things. If it is a POS plan, you can probably count on paying a higher price if you choose an out of network provider, however.

Call your plan provider and double check before having the services provided. It's really the only way to know for certain what you're facing. Wish you best!

Bill Filer's advice to "call your plan provider and double check" before going out of network applies doubly here. HMO-POS plans vary widely in how they handle out-of-network access, and the details matter. Some HMO-POS plans only allow out-of-network access for certain services, so seniors should not assume the POS feature works like a PPO. But for those who want the security of knowing they could go outside the network if they absolutely had to, without paying the ongoing "flexibility tax" on every routine visit, an HMO-POS can be a strong middle ground.

Not every market has HMO-POS plans available, and they're less heavily marketed than standard HMOs and PPOs. A thorough plan comparison with a licensed agent is the best way to find out what's offered in your area.

Prior Authorization: A Shared Pain Point

One argument you'll hear in favor of PPOs is that they don't require referrals to see specialists. That's generally true, and it's a real advantage for people who see multiple specialists regularly. HMOs typically require your primary care doctor to authorize specialist visits, which can add days or weeks to the process.

But there's a catch that trips up many PPO enrollees. While the insurance plan may not require a referral, the specialist's office often does. Many specialist practices have their own internal policies requiring a referral from a primary care physician before they'll schedule you, regardless of what your insurance says. Agents see this constantly with dermatologists, cardiologists, and orthopedic surgeons. You think you're bypassing the gatekeeper, but the doctor's front desk has their own gate.

And prior authorization requirements apply to both HMOs and PPOs. Whether you need approval for an MRI, a specific medication, or a surgical procedure, your plan type doesn't exempt you from the carrier's utilization management process. The referral-free specialist access that PPO enrollees prize is narrower than it looks on paper.

How to Tell If Your PPO Is Costing You More Than It Should

If you're currently enrolled in a Medicare Advantage PPO, here's a quick way to evaluate whether you're getting your money's worth from it:

Check your claims from the last 12 months. How many were out-of-network? If the answer is zero or one, you're paying the PPO tax on every visit for a benefit you're not using.

Compare your plan's benefits to the same carrier's HMO. Most major carriers offer both plan types in the same market. Pull up the Summary of Benefits for each and compare copays, maximum out-of-pocket limits, dental coverage, and supplemental benefits side by side. The gap may surprise you.

Look at your provider list. If every doctor you see regularly is in-network on both the PPO and the HMO version, the PPO isn't giving you anything but higher costs.

Think about your travel patterns. Do you actually spend extended time out of your service area? Not a one-week vacation (emergency coverage handles that on any plan), but months at a time? If not, the PPO's out-of-area flexibility isn't relevant to you.

The Annual Election Period runs from October 15 through December 7 each year. That's your window to switch between plan types without any penalty or underwriting. If you've been paying for flexibility you don't use, that's the time to make the move.

Before switching, ask a licensed local Medicare agent to compare your current PPO against available HMOs, HMO-POS plans, and Medigap options using your actual doctors, prescriptions, travel habits, and claims history. The right plan isn't always the one with the most freedom. Sometimes it's the one that gives you the best coverage for the care you actually get.

Frequently Asked Questions

Is a Medicare Advantage PPO better than an HMO?

Not for most people. A PPO gives you more flexibility to see out-of-network providers, but that flexibility comes at a cost: higher copays, higher out-of-pocket maximums, and often fewer supplemental benefits like dental and vision, even when you stay in network. If your doctors are all in-network and you don't travel extensively, an HMO will typically give you richer benefits at lower cost.

Why do Medicare HMOs often have better extra benefits?

Because insurance carriers can predict their costs more accurately with HMOs. When everyone stays in a defined network with pre-negotiated rates, the carrier faces less financial uncertainty. That lets them invest more in dental coverage, vision benefits, hearing aids, over-the-counter allowances, and other supplemental benefits that attract enrollees.

Can I see any doctor with a Medicare PPO?

Not exactly. A PPO lets you see out-of-network providers, but the provider can refuse to bill your plan, and the cost-sharing for out-of-network care is significantly higher. You may face 30% to 40% coinsurance instead of a flat copay, and you could be responsible for charges above what the plan considers reasonable. "Out-of-network coverage" means you have the option, not that it's affordable or guaranteed.

Who should consider a Medicare Advantage PPO?

Agents say PPOs make the most sense for snowbirds who split time between states, seniors in rural areas with limited HMO networks, people with established specialist relationships outside any local network, and frequent travelers who need routine care away from home. If none of those describe you, compare your PPO's benefits to the same carrier's HMO before your next Annual Election Period.