A Senior's Guide to Medicare: What to Know Before Choosing a Plan

-

Last Updated July 23, 2026

Choosing a Medicare plan is one of the most important healthcare decisions a senior can make, and one of the most confusing. While it's tempting to follow the crowd or pick the lowest premium, those shortcuts can lead to costly mistakes. Consider this your senior's guide to Medicare planning, drawn from real-world advice given by licensed Medicare agents who've worked with thousands of seniors navigating this very decision.

Your Medicare Plan Is Personal, Not Popular

One of the most critical points emphasized repeatedly is that Medicare is not a one-size-fits-all solution. A plan that works for your friend or spouse might not suit your medical needs, financial situation, or provider preferences. Every senior has a unique "Medicare puzzle," and making decisions based solely on someone else's plan can result in gaps in coverage, higher out-of-pocket costs, or the inability to see preferred doctors.

Choosing a plan should reflect your specific priorities. If you travel often, nationwide provider access might be critical. If you're on a fixed income, predictable monthly costs could matter more. If you need frequent care, low co-pays or better specialist access might top the list. Know what you value and build your coverage around it.

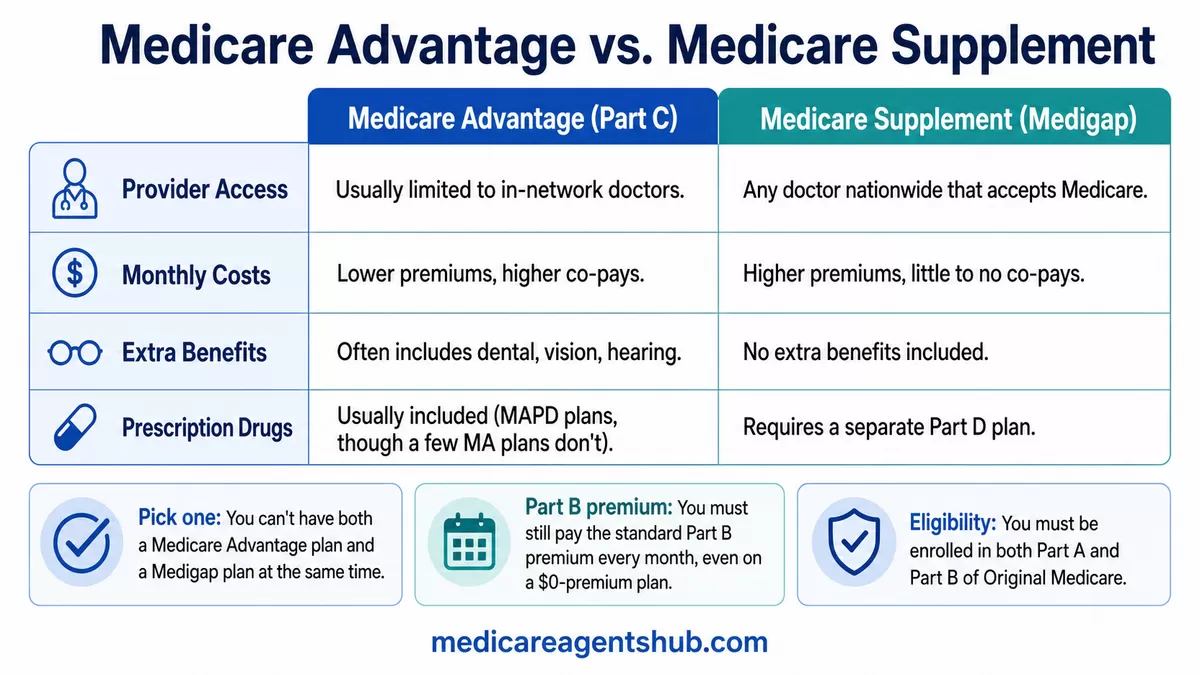

The Two Main Paths: Medicare Advantage vs. Medicare Supplement

Many seniors begin their Medicare journey unaware of the significant differences between Medicare Advantage and Medicare Supplement (also known as Medigap) plans. These paths come with different networks, coverage rules, out-of-pocket responsibilities, and restrictions.

| Feature | Medicare Advantage (Part C) | Medicare Supplement (Medigap) |

|---|---|---|

| Provider access | Usually limited to in-network doctors | Any doctor nationwide that accepts Medicare |

| Monthly costs | Lower premiums, higher co-pays | Higher premiums, little to no co-pays |

| Extra benefits | Often includes dental, vision, hearing | No extra benefits included |

| Prescription drugs | Usually included (MAPD plans, though a few MA plans don't) | Requires a separate Part D plan |

Medicare Advantage plans often include extra benefits but have more limited provider networks and may require prior authorizations. Medicare Supplement plans usually offer broader access but come with higher premiums and fewer "extras." Knowing how each structure works is foundational to making an informed choice. Medigap plans are federally standardized, so a Plan G from one carrier covers the same things as a Plan G from another; the official Medigap comparison chart lays out what each letter plan covers.

One important rule: you can't have both a Medicare Advantage plan and a Medigap plan at the same time. They're two different roads. Pick one. And regardless of which you choose, you'll continue to pay the standard Part B premium every month, even if your plan advertises a $0 monthly premium.

To be eligible for either a Medicare Advantage or Medicare Supplement plan, you must be enrolled in both Part A and Part B of Original Medicare. Some people delay enrolling in Part B while still working, which is allowed if they have creditable coverage, but they must follow the correct procedures and submit documentation to avoid penalties.

As a senior, what should I know about the differences between Original Medicare and Medicare Advantage before I choose?

There are lots of things to know but 2 very specific ones is that original Medicare does not have a max out of pocket on part B so no matter the size of the bill you will owe 20% over and over again, where a Medicare Advantage plan does have a max out of pocket, so once you hit that the plans covers you at a 100% for the rest of the year as long as its medically necessary, and approved by the plan.The other thing I would say is how networks work. Original Medicare uses the Medicare network so as long as the doctor or the hospital etc take Medicare they will accept your original Medicare card and you don't need a referral. With a Medicare Advantage plan, you have to use the specific carrier's network, they have PPO's, HMO's and more but those are the 2 main ones. The doctors must take the plan with an HMO no exception and with a PPO they must be willing to bill it. If your doctors don't take the plan then you will have to pay the bill yourself, so always make sure your doctors are covered.

There is a laundry list of things you need to know, you can reach out at any time.

Start Planning Early and Come Prepared

Rushing into a decision can have long-term consequences. Seniors are encouraged to start researching their options at least six months before turning 65. Early planning allows for a smoother enrollment process and better understanding of the timelines involved, especially for those still working or on employer coverage.

It's also vital to understand that some decisions are difficult to reverse later. For example, switching from a Medicare Advantage plan back to a Medigap plan may involve medical underwriting after your initial enrollment period.

Before speaking with an agent or selecting a plan, prepare a list of:

- Your current doctors, specialists, and preferred hospitals

- All prescriptions: name, dosage, and frequency

- Preferred pharmacies

- Any regular treatments or therapies

This information is essential for accurately comparing plans and avoiding surprises. Understanding Medicare is a process. The more time you give yourself to explore the landscape, the more confident and stress-free your enrollment experience will be.

What Medicare Covers (and Where Seniors Get Surprised)

A common misconception is that Medicare covers all healthcare expenses. In reality, Original Medicare (Parts A and B) does not cover most dental, vision, or hearing care, and it also has significant gaps around nursing home care and prescription drug coverage. Without additional coverage or supplemental plans, out-of-pocket costs can become overwhelming. For most seniors, Original Medicare alone is not enough; that's why the Advantage vs. Medigap decision above matters so much.

Prescription drug coverage requires careful evaluation. Medications can significantly affect your total healthcare costs, and plans differ widely in how they cover drugs. It's essential to list your medications and compare how each plan handles them. Formularies (the list of drugs a plan covers) and pharmacy networks vary between plans, and choosing incorrectly can lead to unexpected costs or access issues.

I have multiple medications; how can I ensure my Medicare Part D plan covers them all without breaking the bank?

That is a very common concern, especially if you take several medications.The first thing to know is that not all Part D plans cover drugs the same way. Each plan has its own formulary, which is simply its list of covered medications. You want to make sure every one of your prescriptions is on that list and preferably on a lower cost tier.

Next, look at where you fill your prescriptions. Many plans have preferred pharmacies or offer better pricing through mail order. That alone can lower your costs.

It is also worth asking your doctor if any of your medications have a generic or lower cost alternative that works just as well. Sometimes a small change can make a big difference in what you pay.

Finally, review your Part D plan every year. Plans can change their drug lists and pricing, and switching during the Annual Enrollment Period can potentially save you hundreds or even thousands over time.

A quick personalized drug review each year is one of the smartest ways to keep costs under control.

Check doctor and hospital networks before you enroll. Many Medicare Advantage plans operate within specific networks. Before choosing a plan, seniors should verify that their current doctors, hospitals, and specialists are included. Even within the same insurance company, networks can differ by plan or region. Confirming this in advance ensures continuity of care and avoids frustrating changes after enrollment.

My Medicare Advantage plan listed my doctor, but now they say he's out of network. How is that even allowed?

That can be frustrating! Medicare Advantage plans typically have contracts with specific networks of doctors, hospitals, and other healthcare providers. However, sometimes these contracts change throughout the year. Even if your doctor was in-network when you enrolled in your plan, they might have been removed from the network later due to changes in the insurance company’s agreements or policies.Unfortunately, this can happen, but you do have some options.

Don't judge plans solely by premiums. Low premiums can be misleading. A plan with no monthly premium may come with higher co-pays, narrow networks, or poor prescription coverage. On the flip side, a higher premium plan may offer broader access and better financial protection. Evaluating total expected costs, including deductibles, co-pays, and maximum out-of-pocket limits, is more important than focusing only on the monthly bill.

Enrollment Deadlines and Costly Penalties

Missing enrollment deadlines can result in lifelong penalties or gaps in coverage. For example, delaying enrollment in Part B without creditable coverage (like employer insurance) can lead to permanent monthly surcharges. Seniors should also be aware of the need to submit forms like the L-564 form if deferring enrollment while working past 65.

Enrollment timing also affects your flexibility. Some decisions, like enrolling in a Medigap plan, offer guaranteed acceptance only for a limited time after you start Part B. After that window closes, medical underwriting may apply, meaning you could be denied based on health. Planning ahead helps avoid these restrictions and keeps more options open.

I'm turning 65 next month; what are the first steps I should take regarding Medicare enrollment?

If you’re turning 65 next month, the first step is to confirm whether you should enroll in Medicare Part A and Part B right away or if you can delay Part B because you’re still covered under an employer plan. From there, we look at whether a Medicare Supplement with a Part D plan or a Medicare Advantage plan makes the most sense for you, and we time everything so your coverage starts seamlessly with no gaps or penalties.Working with a Medicare Agent and Avoiding Bad Actors

A recurring theme in expert advice is the benefit of working with an independent Medicare agent. These professionals have access to a wide range of plans and carriers, giving them the ability to match your needs to the best available options. When evaluating agents, it helps to understand agent designations and credentials so you know what qualifications to look for. Importantly, using an agent doesn't cost you anything; commissions are paid by the insurance companies, not the clients.

Not every agent represents every carrier, so it's always fair to ask which companies they can quote before you dig into plan options. If you'd rather talk with someone who isn't paid by any carrier at all, your State Health Insurance Assistance Program (SHIP) offers free, unbiased Medicare counseling from trained volunteers in every state.

Many seniors fall victim to aggressive marketing tactics and unsolicited calls. It's important to know that telemarketing without prior consent is illegal in this space. Trustworthy agents won't rush you or push a specific plan. They'll help you evaluate all your options with transparency and patience.

From understanding basic terminology to comparing benefit structures, Medicare can be confusing. Seniors should never hesitate to ask questions, even if they feel basic. An informed decision is far better than an educated guess.

Watch Out for "Freebies" and Gimmicks

Some plans advertise enticing perks like gym memberships, grocery cards, or flex spending benefits. While these extras may seem attractive, they should not be the primary reason for selecting a plan. Coverage for doctors, hospitals, and prescriptions should always come first, followed by a careful look at cost-sharing, deductibles, and network access.

Along similar lines, you may come across free Medicare seminars in your area. These events can be helpful, but they vary widely in quality and intent. Before attending, it's worth considering whether free Medicare seminars are actually worth your time.

Plan for Change: Annual Reviews and the Unexpected

Healthcare availability, networks, and plan options can differ greatly depending on where you live. Just because a plan works well in one area doesn't mean it's a good fit elsewhere. Local agents often have the best understanding of what works in your region and which carriers have the strongest presence.

Your health may be stable now, but Medicare is about long-term planning. Choosing a plan with the future in mind, one that accommodates unexpected illness, mobility changes, or new medications, will provide better peace of mind.

Even after you choose a plan, it shouldn't be set in stone forever. Healthcare needs, medications, and plan benefits can change year to year. The Annual Enrollment Period runs October 15 through December 7 each year, which is your window to switch Medicare Advantage or Part D plans for the following year. Meeting with a trusted agent during that window ensures your coverage continues to meet your evolving needs.

Which Medicare Supplement plan (Medigap) offers the best value for most seniors, and why?

For most seniors, Medigap Plan G is often considered the best overall value because it provides near-complete coverage—paying for almost all out-of-pocket costs except the small Part B deductible, which makes healthcare expenses very predictable. However, Medigap Plan N can be a better value for healthier individuals, since it offers lower monthly premiums in exchange for small copays and a bit more risk. In simple terms, Plan G is best if you want maximum coverage and peace of mind, while Plan N is ideal if you want to save money and don’t mind occasional out-of-pocket costs—so the “best value” really depends on your health usage and budget.Final Thoughts: Don't Go It Alone

The overwhelming consensus from Medicare experts is clear: don't try to figure everything out on your own. With so many moving parts: enrollment windows, plan types, cost structures, and coverage details, it's easy to miss something important. Fortunately, knowledgeable professionals are available, at no cost to you, to help guide the way. The best Medicare decision is one made with clarity, care, and support. Find a local Medicare agent near you to get started.