The Most Overhyped Medicare Advantage Benefits, According to Agents Who Sell Them

-

Last Updated July 27, 2026

Flex cards for groceries. Part B givebacks. Silver Sneakers. Free dental. If you watch TV during enrollment season, you'd think Medicare Advantage plans hand out money and benefits like party favors. But the agents who actually sell these plans have a different take. Many of the "extras" that dominate advertising are either unavailable to most people, barely used, or nowhere near as generous as the commercials suggest.

This isn't an anti-Medicare Advantage article. MA plans serve millions of seniors well, and every plan involves trade-offs. But when marketing outpaces reality, people make decisions based on benefits they'll never actually receive. Here's what agents say about the four most overhyped MA extras.

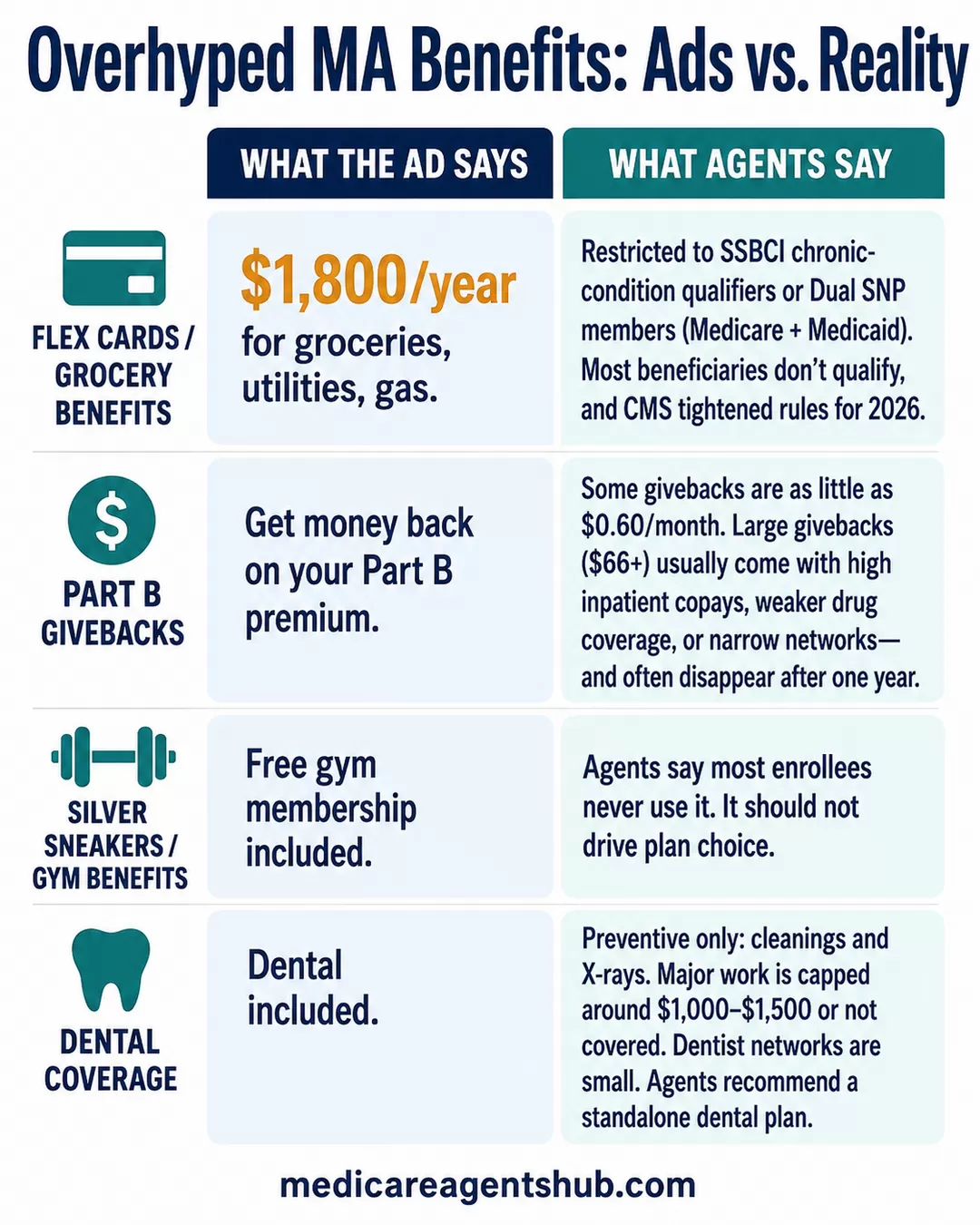

Flex Cards and Grocery Benefits: The Bait That Hooks the Most People

If there's one benefit that agents universally flag as misleading, it's the flex card. TV ads show seniors buying groceries, paying utility bills, and filling up their cars - all with a card loaded with hundreds of dollars. The reality is far more limited.

These cards are tied to Special Supplemental Benefits for the Chronically Ill (SSBCI) or Dual Special Needs Plans (D-SNPs) for people who qualify for both Medicare and Medicaid. That means you either need a qualifying chronic condition or a low enough income to be on Medicaid. The vast majority of Medicare beneficiaries don't qualify for either. And for 2026, CMS tightened the rules even further — most grocery card benefits have largely disappeared from standard Medicare Advantage plans.

What are the most overhyped benefits of Medicare Advantage plans that seniors should be wary of?

The most over-hyped benefits are the Advantage plan Flex cards for groceries, utility bills, even gasoline. While the benefits are genuine, the scam ads don't mention that these benefits only apply to persons who are chronically ill or dual eligible (on Medicaid).The advertising doesn't make that distinction. One agent on our platform described these ads flatly as "scam ads" that lure people into calling a number, only to be steered into a completely different plan once they find out they don't qualify. The ads rely on phrases like "if eligible" and "qualified members" - language that technically keeps them legal while being functionally deceptive.

Agents who field these calls describe the same pattern over and over. A senior sees a commercial promising a card worth $1,800 a year for groceries. They call. They don't qualify. And now they're on a targeted call list that won't stop ringing.

If you're curious about the biggest disadvantages of Medicare Advantage, the gap between advertised benefits and actual eligibility ranks high on most agents' lists.

Part B Givebacks: The $0.60 Version vs. the Inflated One

Part B giveback plans reduce your monthly Medicare Part B premium. On paper, that sounds like free money. In practice, agents say the numbers range from laughable to suspicious.

The Trade-Off for Large Givebacks

Some giveback plans return as little as $0.60 per month. Others advertise givebacks of $66 or more. But agents warn that the plans with large givebacks often come with trade-offs that cancel out the savings - higher inpatient hospital copays, weaker drug coverage, or thinner provider networks.

What are the most overhyped benefits of Medicare Advantage plans that seniors should be wary of?

The most overhyped benefit is the "money back" plans that many Medicare Advantage Plans offer. Don't get me wrong, they are a good product IF you are aware of the other benefits that are not nearly as robust as the non "money back" plans. There are some insurance products to pair with "money back on your Part B plans" that most brokers are not aware of.The giveback sounds great in a commercial. But when you compare the actual dollar amount against the plan's copays, deductibles, and out-of-pocket maximum, the math often doesn't work. An agent who has looked at hundreds of these plans put it simply: the giveback makes the plan look attractive at first glance, but nearly every plan with a large giveback also has a very large inpatient hospital copay.

The Sustainability Problem

There's another problem with the bigger giveback plans. Several agents point out that plans offering unusually large Part B reductions are often not financially sustainable. They show up one year, attract a wave of enrollees, and then disappear from the market the following year. That leaves seniors scrambling to find a new plan during the next enrollment period.

Before chasing a giveback, it's worth understanding the real cost of Medicare Advantage vs. Medigap and how these trade-offs play out over a full year of care.

Silver Sneakers: The Benefit Almost Nobody Uses

Gym memberships through programs like Silver Sneakers are a staple of Medicare Advantage marketing. Plans tout free fitness access as a wellness perk, and it sounds appealing. But agents who track actual usage tell a different story.

What are the most overhyped benefits of Medicare Advantage plans that seniors should be wary of?

The least used benefit for all the advantage plans is the silver sneakers Fitness benefits anything that has to do with exercise. I always tell everyone if you’re able to use a Fitness benefit from your advantage plan work with a local fitness provider even though you’re not using their service at least you are providing income into the communityIt's not that Silver Sneakers is a bad benefit. Free gym access is genuinely useful for seniors who will use it. The problem is that it's often presented as a headline benefit - something that should factor into your plan decision - when in reality, most enrollees never set foot in a gym after signing up.

Agents consistently say the same thing: don't pick a health plan because of a gym membership. Pick a plan based on whether your doctors are in network, whether your prescriptions are covered, and what your out-of-pocket costs look like if you actually need care. If the plan also includes Silver Sneakers, that's a nice bonus. But it shouldn't be the reason you chose it.

For a broader look at benefits that go unused, agents have weighed in on surprising Medicare Advantage benefits most people don't use.

Dental Coverage in MA: Not the Same as a Real Dental Plan

Original Medicare doesn't cover routine dental work. Medicare Advantage plans often do - and that's a legitimate selling point. But agents are blunt about the gap between what's advertised and what the coverage actually looks like.

Most MA dental benefits cover preventive care only: cleanings, X-rays, and basic exams. If you need a crown, a root canal, dentures, or implants, you're likely looking at either a hard annual cap (often $1,000 to $1,500) or no coverage at all. The network of participating dentists is also typically small, and your preferred dentist may not accept the plan.

Are Medicare Advantage plans really "free," or is that just clever marketing?

Medicare Advantage plans are not free and anyone using that verbiage is misleading and breaking CMS rules. They may be zero premium but that does not mean free. Zero premium means it cost you nothing but they aren’t free because they are subsidized by the government. Free and zero premium is not the same.Multiple agents recommend getting a standalone dental plan instead of relying on the dental benefit bundled into your MA plan. A standalone plan usually has a broader network, higher annual maximums, and coverage for major procedures that MA dental simply doesn't touch.

If dental coverage is a priority, you can explore how to get dental and vision coverage with Medicare and what dental coverage in MA plans actually includes.

What Actually Matters When Choosing a Plan

Agents aren't saying Medicare Advantage is bad. They're saying the extras are just that - extras. The core of any good health plan is whether it covers the care you actually need at a price you can afford.

Here's what agents say should drive your plan decision, in order of priority:

- Provider network. Are your doctors, specialists, and preferred hospitals in-network? This is non-negotiable.

- Out-of-pocket costs. Look at copays, coinsurance, deductibles, and the maximum out-of-pocket limit. A $0 premium plan can still cost thousands if you need care.

- Prescription drug coverage. Make sure your medications are on the plan's formulary and that the copays are manageable.

- Ancillary benefits. Dental, vision, hearing, fitness, OTC cards. Nice to have, but they should never be the deciding factor.

What are the most overhyped benefits of Medicare Advantage plans that seniors should be wary of?

Medicare advantage plans have a lot of nice extra benefits but in my opinion, where seniors fall victim, is when they focus too much on their plans extra benefits instead of looking at the actual medical benefits and their out of pocket exposure. You want to make sure your plans medical benefits are in line with with your needs and the the extra benefits are what they are.A local Medicare agent who specializes in Advantage plans can walk you through the actual benefits side by side, without the marketing spin. That comparison is where the real picture emerges - not from a 30-second commercial promising grocery money you may never qualify for.