Why Medicare Grocery Cards Largely Disappeared in 2026 and Who Still Qualifies

-

May 2, 2026

If you had a Medicare Advantage plan that helped pay for groceries in 2024 or 2025, there's a good chance that benefit is gone. New rules from the Centers for Medicare & Medicaid Services (CMS) took effect for the 2026 plan year, and they fundamentally changed how grocery and food card benefits work. For 2026, CMS tightened the rules around food and grocery benefits under SSBCI, and many standard Medicare Advantage members who previously saw these benefits may no longer qualify. In practice, these benefits are now much more closely tied to Special Needs Plans and documented chronic-condition eligibility.

Meanwhile, the TV commercials haven't changed much. Seniors are still calling their agents asking how to get the grocery card they saw advertised. Agents describe it as one of the most common questions they get, year after year. And now they're having to explain that the benefit most callers are asking about has been pulled from the plans they're eligible for.

Here's what actually happened, who can still qualify, and where to turn if you need help putting food on the table.

A quick clarification: Original Medicare (Parts A and B) has never offered a grocery card or food benefit. These benefits, when available, come exclusively through certain Medicare Advantage plans.

The Short Version

- CMS restricted grocery and food card benefits for 2026 under tighter SSBCI rules

- Standard Medicare Advantage plans have largely dropped these benefits

- Dual Special Needs Plans (DSNP) and Chronic Condition Special Needs Plans (C-SNP) are the main paths to grocery benefits now

- Benefit amounts range from $25 to $200/month depending on plan type and eligibility

- Programs like SNAP, Medicare Savings Programs, and Meals on Wheels can help seniors who don't qualify

Why Did Medicare Grocery Cards Disappear in 2026?

The benefit that most people called a "grocery card" or "food card" was technically part of a category called Special Supplemental Benefits for the Chronically Ill (SSBCI). Under SSBCI rules, Medicare Advantage plans could offer extra benefits like grocery allowances, utility assistance, and pest control to enrollees with qualifying chronic conditions.

Before 2026, some insurance carriers stretched the SSBCI rules. They offered grocery cards on regular Medicare Advantage plans, not just Special Needs Plans. The qualifying bar was low, and the benefit became one of the most heavily advertised perks in Medicare Advantage marketing.

CMS tightened the rules. Starting with the 2026 plan year, grocery and food-related flex card benefits are now much more tightly regulated, with qualifying criteria that effectively limit them to two types of plans:

- DSNP (Dual Special Needs Plans) for people who have both Medicare and Medicaid

- C-SNP (Chronic Condition Special Needs Plans) for people with specific qualifying chronic conditions verified by their physician

If you're on a standard Medicare Advantage HMO or PPO, the grocery card you had in previous years is very likely no longer part of your plan. CMS tightened the SSBCI eligibility and documentation requirements to the point where most standard MA plans dropped food benefits rather than try to comply with the new criteria.

Can Medicare pay for my groceries?

Due to changes made in the 2026 plans, some members may qualify for a plan that includes a flex card that will cover healthy grocery items if a person is below a certain income level or has qualifying health conditions. Previously, these benefits were available in plans that were not DSNP (Dual Special Needs Plans) or CSNP (Chronic Special Needs Plans) but changes made to Medicare prior to the Annual Enrollment Period for 2026 eliminated the flexible spending grocery benefits for regular plans, limiting the benefits to people with special needs.DSNP plans are for members receiving both Medicare and Medicaid benefits, and CSNP plans are available for members with specific chronic health conditions, such as Diabetes, Heart, or Lung Conditions.

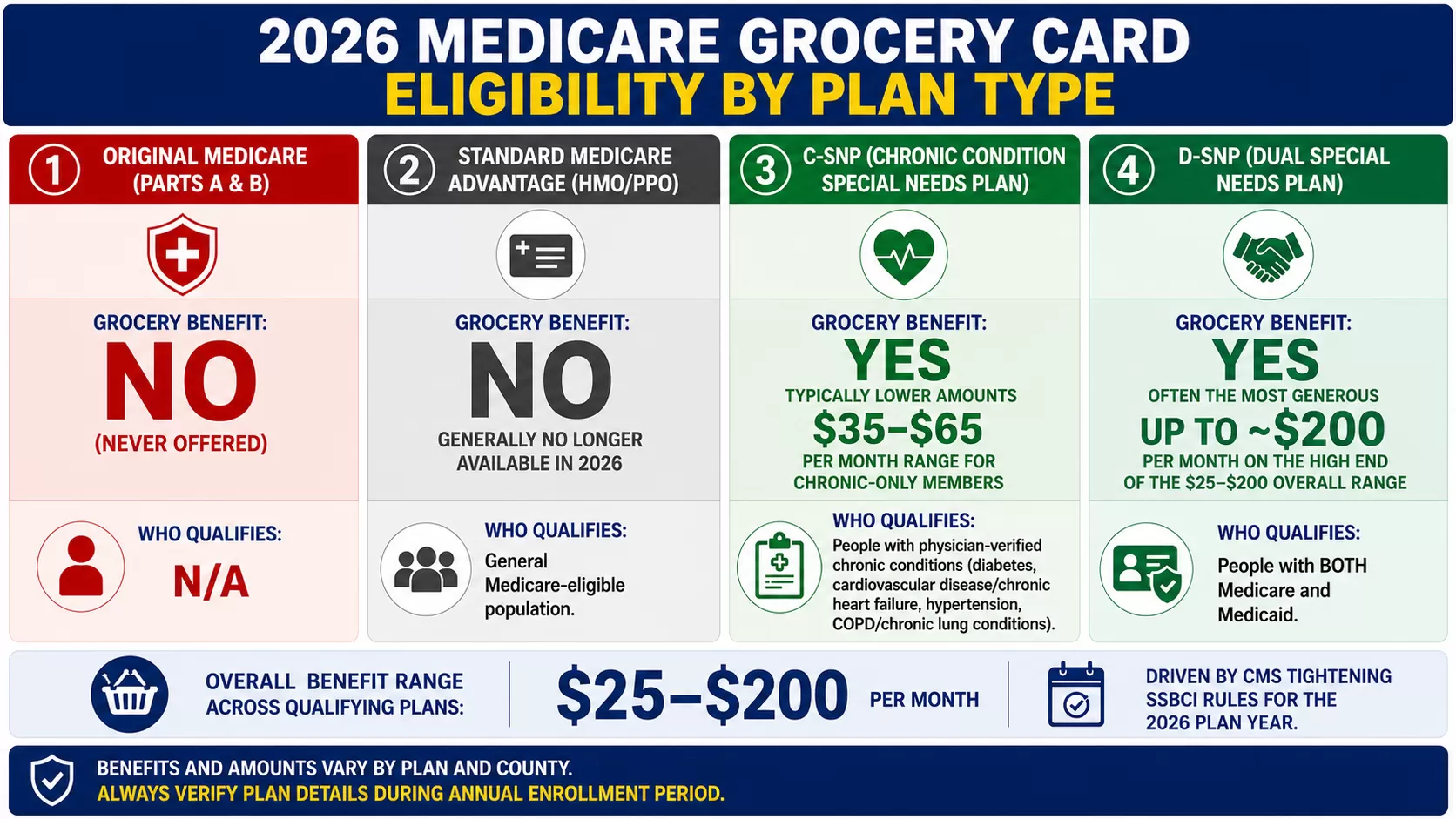

Who Still Qualifies for a Medicare Grocery Card in 2026?

The benefit didn't disappear entirely. It moved behind stricter eligibility gates. Two groups of Medicare beneficiaries can still access grocery or healthy food allowances:

| Plan Type | Grocery Benefit? | Who Qualifies |

|---|---|---|

| Standard Medicare Advantage (HMO/PPO) | Generally no longer available | General Medicare-eligible population |

| D-SNP (Dual Special Needs Plan) | Yes, often the most generous | People with both Medicare and Medicaid |

| C-SNP (Chronic Condition SNP) | Yes, typically lower amounts | People with physician-verified chronic conditions |

| Original Medicare (Parts A & B) | No, never offered | N/A |

Dual-Eligible Beneficiaries (DSNP)

If you receive both Medicare and Medicaid, you may be eligible for a Dual Special Needs Plan. DSNPs typically offer the most generous grocery and OTC benefits. The card can be used at participating retailers for approved healthy food items like produce, dairy, meat, and grains.

One thing that confuses people is where the money actually comes from. As one agent on Medicare Agents Hub explained, the plan gets the money from the state through the Medicaid side, then loads it onto a card for you. It looks like Medicare is paying for your groceries, but it's really the Medicaid funding flowing through your Medicare Advantage plan. That distinction matters, because it means you have to qualify for Medicaid first. Income and asset limits for Medicaid vary by state. If you're unsure how the two programs interact, our guide on how Medicare and Medicaid work together breaks it down.

Chronic Condition Beneficiaries (C-SNP)

If you have a qualifying chronic condition, a C-SNP plan may include a grocery or food allowance as part of its supplemental benefits. Agents report that common qualifying conditions include diabetes, cardiovascular disease or chronic heart failure, hypertension, and COPD or other chronic lung conditions. Your physician must verify the diagnosis, and the plan will typically evaluate your past claims history to confirm eligibility.

Benefit amounts vary widely. Agents report ranges anywhere from $25 to $200 per month depending on the plan and plan type, with chronic-only plans (where you have Medicare but not Medicaid) tending toward the lower end, often $35 to $65 per month. DSNP plans for dual-eligible beneficiaries generally offer more.

Can Medicare pay for my groceries?

Yes, in some plans.These benefits are usually part of Special Supplemental Benefits for the Chronically Ill (SSBCI) → Targeted at people with qualifying chronic conditions (e.g., diabetes, heart disease, hypertension, COPD, or others).

• They’re more common in Special Needs Plans (SNPs), especially Chronic Condition SNPs (C-SNPs) or Dual Eligible SNPs (D-SNPs for those with both Medicare and Medicaid).

• You can generally use the allowance for healthy foods like fresh produce, dairy, meats, grains, and pantry staples at participating retailers (e.g., Walmart, Kroger, CVS)—but not for junk food, alcohol, or non-food items (unless the plan combines it with OTC benefits).

What You Can and Can't Buy

Regardless of the plan, grocery card benefits have restrictions. The card is limited to healthy food purchases at approved retailers. Agents note that eligible items typically include fresh produce, dairy, meats, grains, and pantry staples at participating stores like Walmart, Kroger, and CVS. Alcohol, tobacco, candy, soda, and non-food items are excluded (unless the plan bundles the food benefit with a separate OTC allowance). Unapproved items will be declined at checkout.

A few practical things to watch for if you do have a card:

- Replenishment schedule: Some cards reload monthly, others quarterly. Check which one yours follows.

- Rollover rules: Find out whether unused funds carry over to the next cycle or expire. Many plans don't roll over.

- Earning extra: Some plans add to your benefit amount when you complete specific activities like getting a wellness exam, filling out a health survey, or watching a wellness video.

- Brand and size matching: When shopping in-store, the specific brand and size must match what's on the plan's approved list. If it's not an exact match, you'll be charged out of pocket at the register.

Why Are Those "Free Groceries" Commercials Worse Than Ever?

The celebrity Medicare Advantage commercials were already misleading before 2026. CMS actually forced the company behind the Joe Namath and Jimmie Walker ads to reshoot those commercials a few years ago to strip out the most misleading claims. But the general playbook hasn't changed: ads promise money for food, seniors call in, and most learn they don't qualify.

Now the gap between the advertising and the reality is even wider. The 2026 rule changes mean fewer people qualify for grocery benefits than before, but the commercials haven't adjusted their messaging. As agents on Medicare Agents Hub have pointed out, the most overhyped Medicare Advantage benefits are frequently the ones that get the heaviest advertising.

Agents describe a consistent pattern: the ads generate calls to large call centers, the callers usually don't qualify for the grocery benefit, and they're steered into switching plans anyway. The grocery card is the hook; the plan switch is the goal.

I got a call from a "Medicare agent" promising me free groceries and I almost fell for it. Why is this kind of marketing allowed?

The short answer is: it’s allowed because of loopholes, gray areas, and poor enforcement — not because it’s ethical. Some marketers technically follow the letter of the law while completely violating the spirit of it. They’ll advertise “free groceries,” “food cards,” or “Medicare benefits you’re missing,” then bury the fine print that says you have to qualify for a very specific plan in a very specific area. The goal isn’t education — it’s to get you on the phone so they can flip you into a plan.What really bothers me is that they often blur the line between Medicare and private insurance, use scare tactics, or imply they’re connected to Medicare itself — which they are not. And once your number is in one system, it gets sold and resold, which is why the calls never stop.

This is exactly why I tell people: Medicare doesn’t call you, and legitimate agents don’t lead with giveaways. If groceries, cash cards, or “extra benefits” are the hook, that’s a red flag. Real Medicare planning starts with your doctors, your prescriptions, and your costs — not gimmicks.

If anyone ever wants a second opinion, I’m always happy to take a look and tell them straight up whether something is real, exaggerated, or just marketing fluff. No pressure, no scare tactics, and no free-grocery bait.

If you receive an unsolicited call from someone promising free groceries through Medicare, that's a red flag. CMS rules prohibit agents from cold-calling Medicare beneficiaries without prior permission.

What's the Hidden Trade-Off Most People Don't Hear About?

Even for people who do qualify for a plan with a grocery card, there's a cost that rarely gets mentioned in the ads. Agents report that many of the plans offering food benefits, particularly DSNP and C-SNP HMOs, come with network restrictions that limit which doctors and hospitals you can use. Some also carry higher copays and out-of-pocket limits than the plan you might be leaving.

A $50 monthly food benefit sounds good until you realize the plan doesn't cover your current doctors, restricts specialist access to in-network referrals only, or has a higher maximum out-of-pocket than your existing coverage. Every Medicare Advantage plan involves trade-offs, and the flashy extras are often what distract people from the details that actually matter.

This is exactly why agents push back against the idea of switching plans for a single benefit. Your doctors, your prescriptions, and your total cost exposure should drive the decision, not a grocery card.

If you're weighing multiple plan options, talking to a local Medicare agent who can compare everything side by side is the fastest way to see whether the trade-off is worth it for your situation.

What Should You Ask Before Switching Plans for a Grocery Card?

If you're considering a plan switch specifically because of a grocery or food benefit, slow down and ask the right questions first. A grocery card that saves you $50 a month isn't worth it if the new plan costs you more in other ways. Before you make any changes, get clear answers on these points:

- Are my current doctors in this plan's network? Losing access to a physician you trust can have real consequences, especially if you're managing ongoing health issues.

- Are all my prescriptions covered on this plan's formulary, and at what tier? A drug that moves from Tier 1 to Tier 3 can mean hundreds more per year in copays.

- What is the maximum out-of-pocket cost for the year? Compare this directly against your current plan. A lower grocery benefit doesn't help if your MOOP jumps by thousands.

- Does the food benefit require a documented chronic condition or physician verification? Some plans list the benefit but have eligibility gates you may not clear.

- Does the monthly allowance roll over if I don't use it all? Many plans reset unused balances each month, so the advertised annual total may not reflect what you actually receive.

- How long is the benefit guaranteed? Plan benefits can change every year at renewal. A grocery card offered in 2026 may not be there in 2027.

An independent Medicare agent can help you compare these details side by side. The goal is to make sure you're not trading meaningful coverage for a perk that looks good on paper but doesn't hold up under scrutiny.

Common Myths About Medicare Grocery Cards

Between the TV ads and word of mouth, there's a lot of misinformation circulating about Medicare grocery benefits. Here are the most common myths agents hear from callers, and what's actually true.

Myth: Everyone on Medicare gets a free grocery card.

Reality: Original Medicare has never offered food benefits. Only certain Medicare Advantage plans include them, and after the 2026 rule changes, eligibility is largely limited to DSNP and C-SNP enrollees.

Myth: The grocery card covers anything at the store.

Reality: Cards are restricted to approved healthy food items at participating retailers. Alcohol, tobacco, candy, soda, and non-food products are excluded. The specific brand and size must match the plan's approved list.

Myth: If I call the number in the commercial, I'll get a grocery card.

Reality: Those commercials route to large call centers. Most callers don't qualify for the grocery benefit. Agents report that the food card is used as a hook to get seniors to switch plans, often into coverage that may not fit their needs.

Myth: A $50/month grocery card is always worth switching plans for.

Reality: A plan with a grocery benefit may come with a narrower doctor network, higher copays, or a higher maximum out-of-pocket limit. Those costs can easily outweigh $600 a year in grocery help. The benefits that actually save money are sometimes the ones nobody advertises.

Myth: Unused grocery card money rolls over every month.

Reality: Most plans reset unused balances at the end of each month or quarter. If you don't use it, you lose it.

What Are the Alternatives If You Don't Qualify?

If you don't qualify for a DSNP or C-SNP with grocery benefits, there are other programs designed to help seniors afford food. These aren't tied to your Medicare plan at all.

SNAP (Supplemental Nutrition Assistance Program)

Formerly known as food stamps, SNAP provides monthly benefits loaded onto an EBT card for purchasing groceries. Many seniors who qualify don't apply because they assume they're ineligible or find the process confusing. Income limits vary by state and household size. Contact your state's SNAP office or your local Department of Social Services to check eligibility and apply.

Medicare Savings Programs (MSPs)

MSPs don't directly pay for groceries, but they can free up money in your budget by covering your Medicare Part B premium, deductibles, and copays. If you qualify for a Medicare Savings Program, you may also automatically qualify for Extra Help with Part D prescription costs. That can add up to significant savings each year, money that can go toward food and other essentials. Contact your state Medicaid office to see if you qualify.

Area Agencies on Aging

Every county in the United States has an Area Agency on Aging (AAA) that connects seniors with local resources, including meal delivery programs, congregate meal sites at senior centers, emergency food assistance, and referrals to food pantries. Call the Eldercare Locator at 1-800-677-1116 to find your local AAA.

Meals on Wheels and Food Banks

Meals on Wheels delivers prepared meals directly to homebound seniors, often at no cost or on a sliding scale. Local food banks and food pantries also serve seniors regardless of income. Neither program requires any connection to your Medicare coverage.

How to Check Whether You Qualify

If you think you might be eligible for a DSNP or C-SNP plan that includes grocery benefits, here's where to start:

- Check your Medicaid status. If you receive Medicaid or think you might qualify based on your income, a DSNP could be an option. Contact your state Medicaid office to verify.

- Review your health conditions. If you have a chronic condition like diabetes, heart disease, or COPD, ask your doctor whether it qualifies you for a C-SNP in your area. The plan will look at your claims history to verify.

- Talk to a local Medicare agent or broker. An independent agent can look up which SNP plans are available in your county and whether you meet the eligibility requirements. They can also help you weigh the trade-offs, because SNP plans come with their own network restrictions and rules. Find a Medicare agent near you to get started.

Frequently Asked Questions

Does Original Medicare offer a grocery card?

No. Original Medicare (Parts A and B) does not include grocery or food benefits. These have only ever been offered through certain Medicare Advantage plans.

Can Medicare Advantage plans still offer healthy food benefits in 2026?

Some can, but the rules are much stricter. Plans must now meet tighter SSBCI criteria, and in practice, food benefits are largely limited to D-SNP and C-SNP plans for members with qualifying chronic conditions or dual Medicare-Medicaid eligibility.

Do I need Medicaid to get a Medicare grocery card?

Not necessarily. Dual-eligible beneficiaries (Medicare + Medicaid) can access food benefits through DSNP plans, but people with qualifying chronic conditions may also access them through C-SNP plans without Medicaid.

What chronic conditions may qualify for food benefits?

Common qualifying conditions include diabetes, cardiovascular disease, chronic heart failure, COPD, and hypertension. Your physician must verify the diagnosis, and the plan reviews your claims history.

Are Medicare grocery card commercials legitimate?

The benefits they describe can be real, but the ads are often misleading about who actually qualifies. Most callers don't meet the eligibility criteria, especially under the 2026 rules.

Can Medicare still pay for groceries in 2026?

Only through specific plan types. DSNP plans (for dual Medicare-Medicaid beneficiaries) and C-SNP plans (for those with qualifying chronic conditions) may still include grocery allowances. Standard Medicare Advantage HMOs and PPOs have largely dropped these benefits.

Are grocery card commercials misleading?

In most cases, yes. The ads promise benefits that the majority of callers won't qualify for. CMS has previously forced advertisers to revise misleading claims, but the core tactic of using food benefits as a hook to drive plan switches continues.

Don't switch plans just for the grocery card. Work with someone who will compare your full list of needs, not just the extras. And if someone calls you out of the blue promising free groceries? Hang up. The truth about "free" Medicare Advantage plans is that the real cost is often hidden in the details.