5 Medicare Mistakes That Cost People Thousands (And How to Avoid Them)

")

Medicare shouldn't be complicated. But for most people approaching 65, it is, and the cost of getting it wrong can be staggering.

Over the years working with Medicare beneficiaries across the country, I've seen the same mistakes repeat themselves over and over again. People who are intelligent, financially savvy, and well-prepared for retirement still stumble when it comes to Medicare, not because they're careless, but because the system is genuinely confusing. Too many conflicting messages, too many plan types, and too much at stake.

Here are the five most common and most costly Medicare mistakes I see, and what you can do to avoid them.

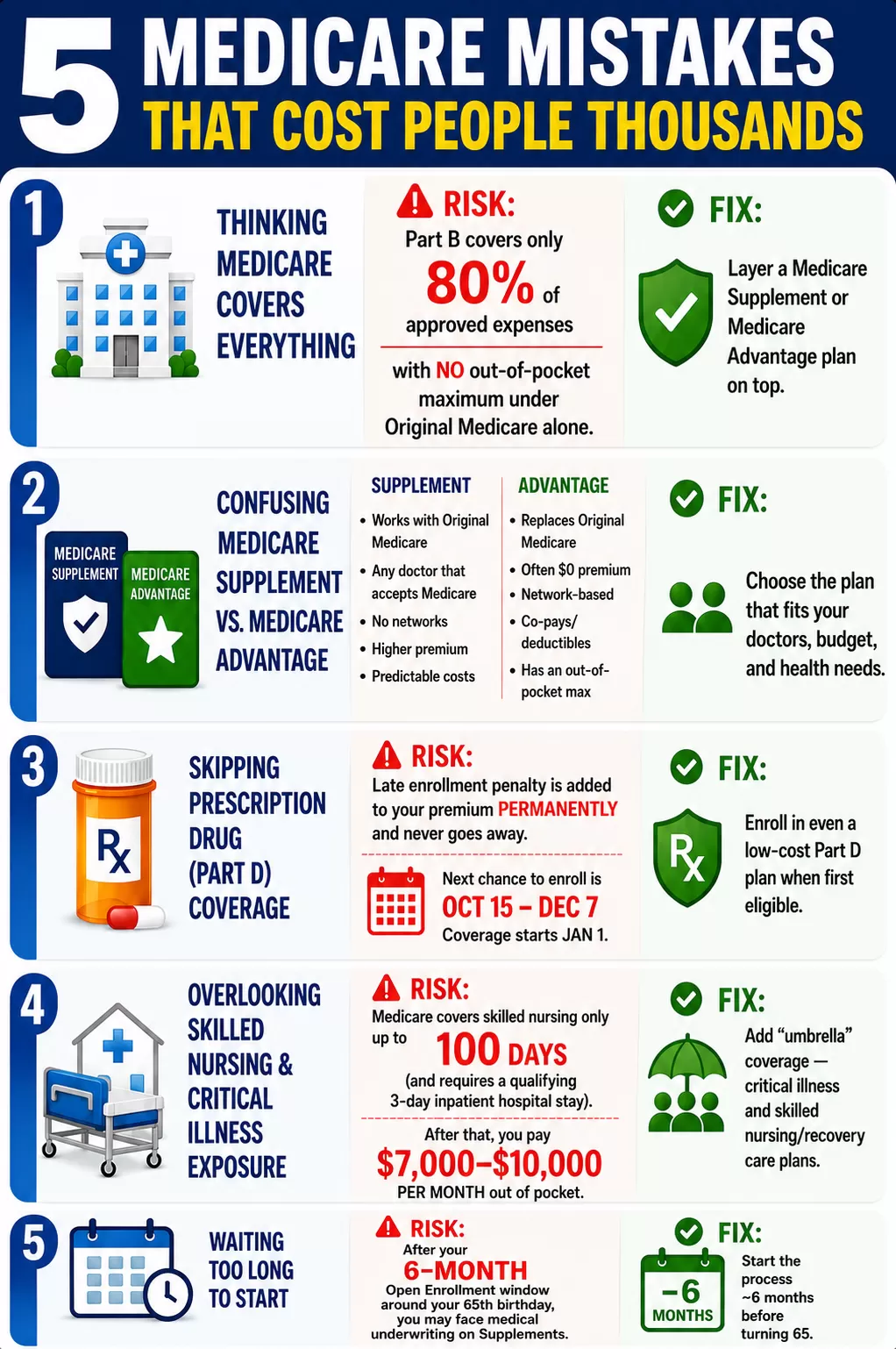

Mistake #1: Thinking Medicare Covers Everything

This is probably the most widespread misconception in the entire Medicare system. People receive their red, white, and blue Medicare card and assume they're fully covered. They're not.

Original Medicare, Parts A and B, is the foundation. Part A covers inpatient hospital stays. Part B covers doctor visits and outpatient care. Together, they form the base of your coverage. But here's what most people don't realize until it's too late: the gaps they leave behind are enormous.

With Part A, if you're admitted to a hospital, you face a significant upfront deductible before coverage kicks in, and if your stay extends beyond a certain number of days, daily co-pays begin stacking up. A prolonged hospital stay under Original Medicare alone can cost you thousands of dollars.

With Part B, Medicare covers 80% of your approved medical expenses. You are responsible for the remaining 20%, with no cap. There is no maximum out-of-pocket limit under Original Medicare alone. That means a cancer diagnosis, a major surgery, or an extended illness could expose you to tens of thousands of dollars in out-of-pocket costs.

I've sat across from clients who were shocked to hear this. One gentleman, a successful, financially astute man, chose to skip additional coverage because he felt confident he could self-pay if anything came up. When he was later diagnosed with leukemia, Medicare covered 80% of his Part B treatments. He paid the other 20%, with no limit, and the bills added up fast.

The fix: Understand that Original Medicare is a foundation, not a complete coverage solution. You need either a Medicare Supplement or a Medicare Advantage plan layered on top to protect yourself from these gaps.

Mistake #2: Confusing Medicare Supplement and Medicare Advantage

Almost every new client I meet with has heard both terms but can't clearly explain the difference. And honestly, that's not surprising, the marketing around Medicare Advantage plans especially can be overwhelming and confusing.

Here's the clearest way I know to explain it:

Medicare Supplement (also called Medigap) works alongside Original Medicare. You keep your red, white, and blue card, and the supplement acts as secondary insurance, filling in the gaps that Medicare leaves behind. These plans typically allow you to see any doctor or hospital in the country that accepts Medicare, with no network restrictions. They cost more per month, but they come with predictable, comprehensive coverage and minimal financial exposure.

Medicare Advantage replaces your Original Medicare coverage with a private insurance plan. These plans are often zero-premium or very low cost, and they frequently include extra benefits like dental, vision, hearing, and gym memberships. The trade-off is that they operate within a network, and you'll have co-pays, deductibles, and an out-of-pocket maximum, meaning your healthcare costs can vary significantly depending on how much care you need in a given year.

I tell people: with a Medicare Supplement, you pay more and get more. With Medicare Advantage, you pay less upfront but take on more financial exposure.

Neither option is universally better. I have clients thriving on both. The right answer depends entirely on your health, your doctors, your medications, your budget, and your risk tolerance. But you cannot make a good decision if you're confusing the two, and most people are. Medigap.

Mistake #3: Skipping Prescription Drug Coverage

This one comes up time and again, and it almost always follows the same pattern: someone turns 65, they're in good health, they're not taking any medications, and they decide there's no point in paying for a drug plan they don't need.

It's an understandable logic. But it ignores two important realities.

First, health changes. Sometimes slowly, sometimes suddenly. A person who takes no prescriptions at 65 may be managing multiple medications at 70, including expensive specialty drugs for chronic conditions. By the time they realize they need coverage, they can't simply enroll mid-year. They have to wait until the Annual Enrollment Period (October 15 through December 7), with coverage not starting until January 1.

Second, and this one catches people off guard, skipping Part D when you're first eligible results in a late enrollment penalty. This penalty is calculated based on how many months you went without coverage, and it gets added to your monthly premium permanently. It never goes away. You can read real examples of how these penalties add up in real stories of lifelong Medicare penalties.

There are very inexpensive Part D plans available. Even if you're currently taking no medications, enrolling in a low-cost plan protects you from the penalty and ensures coverage is in place when you need it. The few dollars a month you spend now could save you a significant penalty and a coverage gap later.

Mistake #4: Overlooking Skilled Nursing and Critical Illness Exposure

This is the most underestimated financial risk in the entire Medicare system. And it's the one that, when it hits, can devastate a family's financial legacy.

Most people don't realize that Medicare only covers skilled nursing care for up to 100 days, and even getting those 100 days covered requires jumping through several hoops, including a qualifying three-day hospital inpatient stay and demonstrating continued improvement. Once those 100 days are up, Medicare coverage stops entirely. The cost of a nursing home or skilled care facility, which can run $7,000 to $10,000 per month depending on the level of care and geographic location, falls completely on you.

Similarly, a diagnosis of cancer, heart attack, or stroke creates costs that Medicare often doesn't fully cover. Treatments, therapies, and medications specific to these conditions can result in significant out-of-pocket expenses, even with a good base Medicare plan in place.

The solution is what many in the industry call umbrella coverage, layering additional protection on top of your Medicare plan to address these specific risks. Critical illness coverage for cancer, heart attack, and stroke. Skilled nursing and recovery care coverage. These aren't luxury add-ons. For many families, they're the difference between maintaining financial stability and depleting a lifetime of savings.

I've worked with families in the middle of these crises, and I can tell you from experience that the ones who had the right protection in place faced an already-difficult situation with far less financial panic than those who didn't.

Mistake #5: Waiting Too Long to Start the Process

The Medicare enrollment window seems generous on paper, but in practice, waiting until the last minute creates real problems.

For Medicare Supplement plans, the optimal time to start the process is about six months before your 65th birthday. During this window, called your Open Enrollment Period, you have guaranteed issue rights, meaning insurance companies cannot deny you coverage or charge you more based on pre-existing health conditions. Once this window closes, you can still apply for a Medicare Supplement, but you may be subject to medical underwriting. That means your health history could affect your eligibility or your rates.

Starting early also gives you time to compare plans, understand your options, ask questions without the pressure of a deadline, and correct any errors before your coverage start date. People who begin the process six months out are almost always calmer, better informed, and better covered than those who wait until two weeks before their birthday.

One more thing worth addressing: many people hesitate to engage with an agent or broker because they assume it will cost them something. It doesn't. Medicare brokers are compensated by the insurance carriers, not by you. You pay the exact same price for a plan whether you work with a broker or navigate it alone, the difference is that working with an experienced, independent broker means you have someone in your corner, year after year, keeping your coverage aligned with your changing needs.

What are the reasons why I should work with a Medicare agent?

A local agent beats an 800 number every time — you get a real person who knows your market and actually cares about your situation. We break Medicare down into simple, easy-to-understand pieces, and our services cost you absolutely nothing.The Bottom Line

Medicare isn't a one-time decision. Your health changes. Your medications change. The plans themselves change every year. The people who navigate Medicare successfully are the ones who approach it proactively, work with someone they trust, and treat it as an ongoing conversation rather than a box to check.

If you take nothing else away from this article, take this: the worst decision you can make with Medicare is doing nothing. There are options available at nearly every price point. But you have to take action, early, informed action, to make sure those options are working in your favor.

If you're approaching 65 or helping a loved one get started, consider connecting with a local Medicare agent in Tennessee or find an agent near you to get the process started on the right foot.

About the Author: Nathan Wright is a licensed Medicare advisor and founder of Medi65, based just outside of Nashville, Tennessee. Specializing in Medicare Advantage, Medicare Supplement, and prescription drug plans, Nathan is known for his straightforward, education-first approach to helping retirees make confident Medicare decisions. He is the author of 64+: Your Ultimate Guide to Medicare & Retirement Planning, published by Game Changer Publishing.