Is Original Medicare Enough? 5 Essential Services It Doesn’t Cover

-

Last Updated July 23, 2026

When you turn 65, enrolling in Medicare can feel like a huge relief. You finally have health insurance that helps cover many of the medical costs you might face in retirement. But it’s important to understand what Original Medicare (Parts A and B) actually includes, and just as importantly, what it leaves out.

While Original Medicare provides a solid foundation for your healthcare, it doesn't offer complete protection. When working with Medicare advisors, many retirees are surprised to find they still face significant out-of-pocket costs or need additional coverage for essential services. If you’re planning to rely on Medicare Parts A and B alone, here are five key services it doesn’t cover, and what that could mean for you.

5 Services Original Medicare Does Not Cover

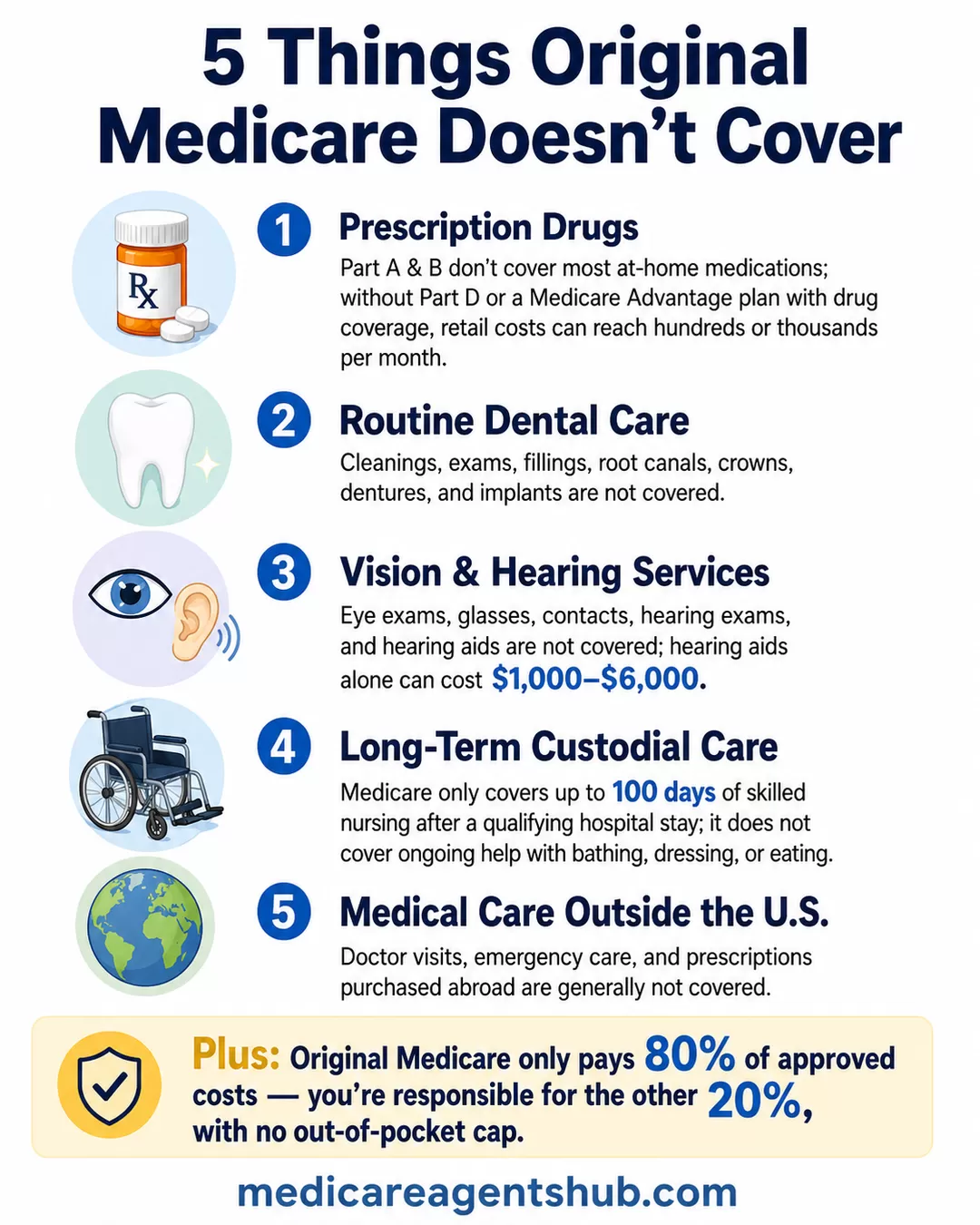

1. Prescription Drugs

Perhaps the most well-known gap in Original Medicare is prescription drug coverage. Part A covers hospital care, and Part B covers outpatient services like doctor visits and lab work, but neither covers most prescription medications you take at home.

If you need ongoing medications for conditions like high blood pressure, diabetes, or arthritis, you’ll need to enroll in a Part D drug plan or choose a Medicare Advantage (Part C) plan that includes drug coverage. Without one, you could end up paying the full retail price for your prescriptions, which can easily run into hundreds, or even thousands of dollars per month.

I have multiple medications; how can I ensure my Medicare Part D plan covers them all without breaking the bank?

I recommend you shop with your total yearly out-of-pocket cost as the #1 priority. That means zero in on the combo of premium + copays/coinsurance for your specific drugs over the whole year. That's what really hits your wallet.You can have an agent do this or do it yourself on Medicare.gov's Plan Finder. Plug in your ZIP, list every med (name, strength, how you take it), and it'll show plans that cover them.

Compare by "Estimated Annual Drug Costs" or "Total Out-of-Pocket"—premium plus pharmacy costs for your exact list. Pick the lowest total for you

Big key step most skip: After you narrow to a couple plans, check pharmacy prices in the tool—costs can swing $50–$200+ per fill just by where you go. List at least 5 nearby ones to compare: Walmart (usually cheap generics), a grocery store pharmacy like Kroger or Publix (great for convenience and often low prices), a big brand like CVS or Walgreens (good selection but watch premiums), maybe Costco if you're a member, and an independent local one if you have a favorite. Run your meds through each—pick the combo of plan + pharmacy that keeps your yearly total lowest.

Plan stars or customer service ratings are nice to glance at, but they don't pay your bills. If two plans cover your meds the same, chase the cheapest total you pay—stars won't cover a big price difference.

2. Routine Dental Care

Original Medicare does not cover routine dental services such as cleanings, exams, fillings, root canals, crowns, dentures, or dental implants. These are considered non-medical services and are not included in Medicare Parts A or B. While Medicare Part A may cover a dental procedure if it’s medically necessary during a covered hospital stay. For example, jaw reconstruction after an accident, this is the exception rather than the rule. The everyday dental care that most seniors rely on is entirely out of pocket.

This lack of coverage is a significant concern, as poor dental health has been linked to more serious health issues, including infections and heart disease. The absence of dental, vision, and hearing coverage under Original Medicare is one of several gaps agents say are long overdue for reform. If you want help covering dental costs, you’ll need to purchase a standalone dental insurance policy or look into a Medicare Advantage plan that includes dental benefits.

3. Vision and Hearing Services

Vision and hearing care are also missing from Original Medicare. Here’s what that means:

-

Eye exams for glasses or contact lenses are not covered

-

Hearing exams and hearing aids are not covered

-

Eyeglasses, contacts, and hearing devices must be paid for out of pocket

This can be especially frustrating since hearing and vision often decline with age. Hearing aids alone can cost $1,000–$6,000 or more, and Medicare won’t help with that expense unless you have a supplemental plan that includes it.

Some Medicare Advantage plans offer limited vision and hearing benefits, but under Original Medicare, you’ll need to budget for these services yourself.

What are the 6 things Medicare doesn't cover?

Original Medicare does not cover routine eye or hearing exams, nor does it cover eye wear except after cataract surgery or hearing aids. It also does not cover dental except in very limited instances or custodial care in a nursing facility, only rehabilitation. Medicare Advantage plans may cover some of these additional benefits but Original Medicare does not. Over the counter benefits, food cards, and gym memberships are also not covered by Original Medicare. When someone illegally cold calls and tells you Medicare covers these things and you are eligible because you have Parts A and B, hang up, this is not true.4. Long-Term Custodial Care

This is one of the most misunderstood gaps in Medicare coverage. While many people assume Medicare will pay for a nursing home or assisted living facility, that’s not usually the case.

Medicare only covers short-term stays in a skilled nursing facility after a qualifying hospital stay (and even then, only up to 100 days). It does not cover custodial care (such as help with bathing, dressing, or eating) if those are the only services you need.

Long-term care can be very expensive, especially if it’s needed for months or years. Without long-term care insurance or Medicaid eligibility, you may have to pay for these costs out of pocket. Medicaid is a separate, means-tested program that many families rely on once savings run out, but qualifying takes planning.

5. Medical Care Outside the U.S.

If you’re planning to travel or retire abroad, you should know that Original Medicare offers very little coverage outside the U.S. In most cases, Medicare won't pay for:

-

Doctor visits in other countries

-

Emergency care while traveling

-

Prescription drugs purchased abroad

Some Medigap (Medicare Supplement) plans offer limited foreign travel emergency coverage, and it’s narrower than most people think: typically 80% of costs after a small deductible, capped at $50,000 over your lifetime, and only for emergencies that begin during the first 60 days of a trip. Under Original Medicare alone, you’d need to purchase separate travel insurance or pay entirely out of pocket for international care.

Why This Matters

While Medicare Parts A and B offer reliable coverage for hospital stays, doctor visits, lab work, and preventive care, they leave a lot of common healthcare needs uncovered. The costs for prescription drugs, dental work, vision care, hearing aids, and long-term care can add up quickly and if you’re not prepared, they can eat into your retirement savings fast.

This is why many people choose to enhance their coverage with:

-

Medicare Supplement (Medigap) insurance

-

Private dental, vision, or hearing policies

Some beneficiaries also consider add-on products like hospital indemnity, critical illness, and cancer plans to fill gaps that even supplemental coverage may not fully address.

What About Extra Benefits?

You’ve probably seen TV ads promoting over-the-counter allowances, grocery or food cards, and gym memberships like SilverSneakers. None of those come with Original Medicare. They’re extra benefits offered by some Medicare Advantage plans, and they vary widely by carrier and county. If any of these perks matter to you, you’ll want to compare Advantage plans in your ZIP code carefully, since the exact benefits and dollar amounts change every year. Just don’t pick a plan on the extras alone. If the doctor network or drug formulary doesn’t fit, an OTC card or gym membership won’t make up for it.

Each of these options has pros and cons, and the right combination depends on your health, budget, and lifestyle. But one thing is clear: relying on Original Medicare alone leaves serious gaps in your protection.

The Biggest Financial Risk: No Out-of-Pocket Maximum

In addition to these uncovered services, it’s important to know that Original Medicare only pays 80% of approved medical costs. That means you’re responsible for the remaining 20% out of pocket, with no cap on total spending. Unlike employer coverage or Medicare Advantage plans, there is no annual maximum that stops the bleeding once your bills get big. A single serious hospitalization or long chemotherapy course can leave you exposed to tens of thousands of dollars in coinsurance.

The short video below walks through how that 20% coinsurance actually plays out for someone on Original Medicare:

So even if Medicare does cover a service, like a hospital stay or doctor visit, you’re still on the hook for a portion of the bill unless you have supplemental coverage.

Can you just have A and B and not enroll in anything else and still have good coverage?

Having just part A and part B is not advisable because there are still a lot of holes in the coverage. The main hole in coverage would be there is no cap on your part B coinsurance. Part B covers 80% of the medical bill and you’re responsible for the 20% with no cap on the dollar amount. When you start looking at huge procedures that can cost many hundreds of thousands of dollars and you’re responsible for 20% of however, high the bill goes that’s the biggest hole in coverage.Final Thoughts

Original Medicare is a strong starting point for healthcare in retirement, but it’s not comprehensive. Understanding what it doesn’t cover, especially when it comes to prescriptions, dental, vision, hearing, long-term care, and international travel can help you avoid unexpected bills and make smarter choices about your healthcare planning.

If you're unsure which additional plans you may need, consider speaking with a local Medicare advisor. The better you understand your options, the better protected you'll be, both medically and financially.

You can also get free, unbiased Medicare help from your State Health Insurance Assistance Program (SHIP), or by calling 1-800-MEDICARE.