Now That You've Turned 65: How to Choose Medicare Coverage That Protects Your Health and Your Budget

Turning 65 often brings a flood of Medicare mailers, plan summaries, and conflicting advice. That can make it tempting to focus on the most obvious number, the monthly premium, but a strong Medicare decision usually depends on the full picture. A plan that looks inexpensive at first can become costly if your doctors are out of network, your prescriptions fall into expensive coverage tiers, or you face high copays when you actually need care.

The key question is not simply, "What is the premium?" but rather, "What am I likely to spend over the course of the year if I use this coverage?" Looking at total value means comparing provider access, prescription coverage, deductibles, copays, coinsurance, and the plan's annual spending limits. When you understand how those pieces work together, you can make a choice that better protects both your health and your budget.

What to Evaluate Before You Choose a Medicare Plan

Provider Networks and Access to Your Doctors

Start with the provider network. In many Medicare Advantage plans, routine care is most affordable when you use doctors, specialists, hospitals, labs, and pharmacies that participate in the plan's network. If an important physician or hospital is outside that network, you may pay more, or you may not have coverage for non-emergency care at all, depending on the plan type.

That is why it helps to check more than just your primary care doctor. Think about the specialists you already see, the hospital system you prefer, nearby urgent care centers, and any facilities you might realistically use during the year.

I signed up for a Medicare Advantage HMO, and I'm wondering if I can see a cardiologist out of network without paying everything myself.

With a Medicare Advantage HMO, you generally cannot see an out‑of‑network cardiologist unless it’s an emergency and if you go anyway, you’ll usually pay the full cost yourself. HMOs are Health Maintenance Organizations and require you to stay in‑network and get referrals, so the safest way to see a cardiologist is to choose one who’s contracted with your plan. If staying with your current cardiologist is important, we can look at PPO or HMO‑POS plans that allow out‑of‑network visits at a lower cost.Drug Tiers, Formularies, and What You'll Pay at the Pharmacy

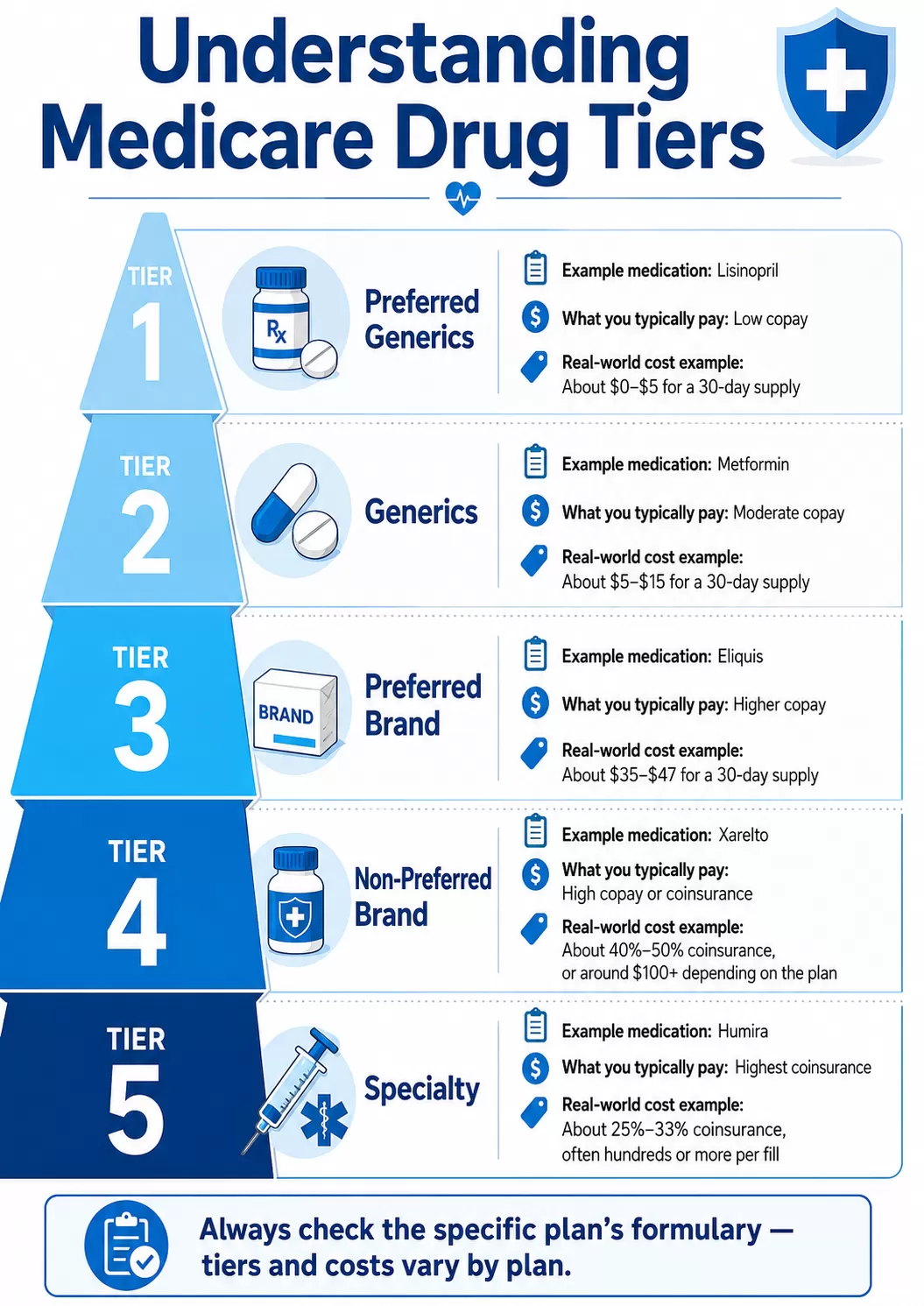

Look closely at the formulary and drug tiers. A formulary is the plan's list of covered prescription drugs, and each covered drug is usually placed into a pricing category called a tier. The tier tells you a great deal about what you are likely to pay. In many plans, the lowest tiers are used for lower-cost generic drugs, which often come with the smallest copays. A middle tier may include preferred brand-name drugs, which are covered but usually cost more than generics.

Higher tiers often include non-preferred brands or specialty medications, and those drugs may require either a large copay or coinsurance, which means you pay a percentage of the drug's price rather than a flat dollar amount. That difference matters because coinsurance can make costs much less predictable, especially for expensive medications.

A simple way to read this is to imagine one medication appearing on two different plans. On Plan A, the drug might be listed as a preferred brand on a mid-level tier with a manageable copay. On Plan B, that same drug could sit on a higher non-preferred tier with coinsurance instead. Even though both plans technically cover the medication, your actual cost at the pharmacy could be very different.

That is why it is not enough to ask whether a drug is covered. You also want to know its tier, whether the cost is a flat copay or a percentage, and whether the plan imposes extra rules such as prior authorization, step therapy, or quantity limits. Prior authorization means the plan wants approval before it will cover the drug. Step therapy means you may need to try a lower-cost medication first. Quantity limits cap how much of a drug the plan will cover during a certain time period. These rules can affect both cost and convenience, even when the medication appears on the formulary.

One more detail many readers miss is that tier names and structures are not perfectly standardized from one insurer to another. A Tier 3 drug in one plan is not automatically priced the same way in another, and a generic medication can sometimes be treated more favorably in one formulary than in the next.

The practical takeaway is to look up each of your medications one by one and compare the full picture: tier placement, pharmacy type, copay versus coinsurance, and any coverage rules or exception processes that might apply. Medicare also allows certain exception requests, including requests to waive some formulary rules or seek a lower cost-sharing tier when medically appropriate.

Supplemental Benefits: Dental, Vision, Hearing, and More

Review supplemental benefits with a practical eye. Benefits such as dental, vision, hearing, transportation, meal support, or over-the-counter allowances can be useful, but their value depends on how the rules are written. One plan might include preventive dental care only, while another offers a broader annual allowance but restricts which providers you can use. The same is true for vision or hearing benefits: the headline benefit may sound generous, but the annual maximum, reimbursement method, and provider network can determine whether it actually helps with your real-world costs.

Cost Sharing Beyond the Monthly Premium

Pay attention to cost sharing, not just the premium. Monthly premiums matter, but they are only one part of the equation. You should also compare deductibles, office visit copays, specialist copays, hospital costs, imaging charges, and coinsurance for services such as outpatient procedures or durable medical equipment. A lower-premium plan may still be the more expensive option overall if you expect regular care and the plan shifts more of the cost to you when you use services.

I picked a Medicare Advantage plan based on the low premium, but now I'm facing high copays. Did I make a mistake?

Not necessarily you didn’t “make a mistake,” but you did choose a plan that traded a low monthly premium for higher copays when you actually use your benefits. Many Medicare Advantage plans keep premiums low by shifting more of the cost to doctor visits, tests, hospital stays, and medications, so it’s very common to feel the pinch once you start using the plan.What I do is help you look at the whole picture your doctors, prescriptions, health needs, and budget and see whether your current plan still makes sense or if there’s a better fit with lower out‑of‑pocket costs. I also help you apply for Medicaid and LIS if we can determine that you may qualify. That would greatly reduce your out of pocket costs.

The Maximum Out-of-Pocket Limit

Understand the maximum out-of-pocket limit. Medicare Advantage plans include an annual maximum out-of-pocket limit for covered Part A and Part B services, which can help protect you from unlimited medical spending if you have a difficult health year. That number does not mean your care will be inexpensive, but it does tell you the ceiling on certain covered medical costs before the plan begins paying more fully for the rest of the year. This is an important contrast with Original Medicare, which does not include the same built-in spending cap unless a person has supplemental coverage.

Questions That Can Help You Compare Plans More Effectively

When you compare plans, it helps to move beyond general marketing language and test each option against your own likely needs. For example, instead of asking only whether your doctor is included, ask whether your plan covers the full care system you use. A doctor may be in network while the hospital where that doctor admits patients is not, or your preferred imaging center may fall outside the plan's contracted providers. Looking at your full pattern of care gives you a more realistic picture of access.

Prescription coverage deserves the same level of detail. If you take medications regularly, compare not only whether they appear on the formulary but also what tier they occupy, whether the plan uses copays or coinsurance, and whether there are utilization rules such as prior authorization. Higher-tier drugs may expose you to significantly larger out-of-pocket costs, especially when plans rely more heavily on coinsurance rather than flat copays.

Recent Medicare drug design changes have added stronger financial protections for Part D enrollees, including an annual out-of-pocket cap for covered prescriptions in 2026, but the way a specific plan structures drug coverage still matters for your month-to-month costs.

It is also wise to think in scenarios. If you see a specialist several times a year, need an MRI, or expect outpatient treatment, what would that plan require you to pay? If you are generally healthy now, what would happen financially if your needs changed midyear? Questions like these can reveal whether a plan is sturdy enough for both routine care and unexpected events.

Choose Coverage With the Whole Year in Mind

Choosing Medicare coverage at 65 is not just an enrollment task. It is an exercise in understanding how insurance actually works in daily life. The most useful comparison is rarely the one with the flashiest extras or the lowest premium at first glance. Instead, it is the one that helps you estimate what care will cost when you use it, whether the doctors and pharmacies you rely on are available to you, and how much financial protection the plan offers if your health needs increase.

For many readers, the best next step is simply to slow the decision down enough to compare plans carefully and ask better questions. By understanding provider networks, formularies, tier placement, utilization rules, cost sharing, and annual spending limits, you can evaluate Medicare options with much greater confidence and avoid surprises later in the year.

About the Author: Françoise (Fran) Mueller is the founder of Ohana Medicare in South Jordan, Utah, and a licensed Medicare broker in over 38 states. With more than 26 years of healthcare experience spanning public and private sectors, Fran guides seniors and veterans through Medicare, disability benefits, and vital resources. She brings the Aloha Spirit from her Kailua, Hawaii roots to every client interaction.