What New Retirees Get Wrong About Medicare in Their First Year

-

January 21, 2026

Becoming eligible for Medicare is a major milestone. It can feel like a celebration, but it also comes with some complex rules and deadlines. If you’re new to Medicare and feeling lost, you’re far from alone. In the excitement of retirement, many people make mistakes that can cost them money or coverage later on. Here are some of the most common misunderstandings new retirees face and how to avoid them.

Thinking Coverage Starts Automatically

One of the first things new retirees often get wrong is assuming coverage begins without any action on their part. If you are already receiving Social Security benefits at least four months before you turn 65, enrollment may happen automatically. If you are not receiving those benefits yet, you may need to enroll yourself during a specific time window. It is important to check your situation early so you do not end up without coverage when you expect it.

Missing the Initial Enrollment Period

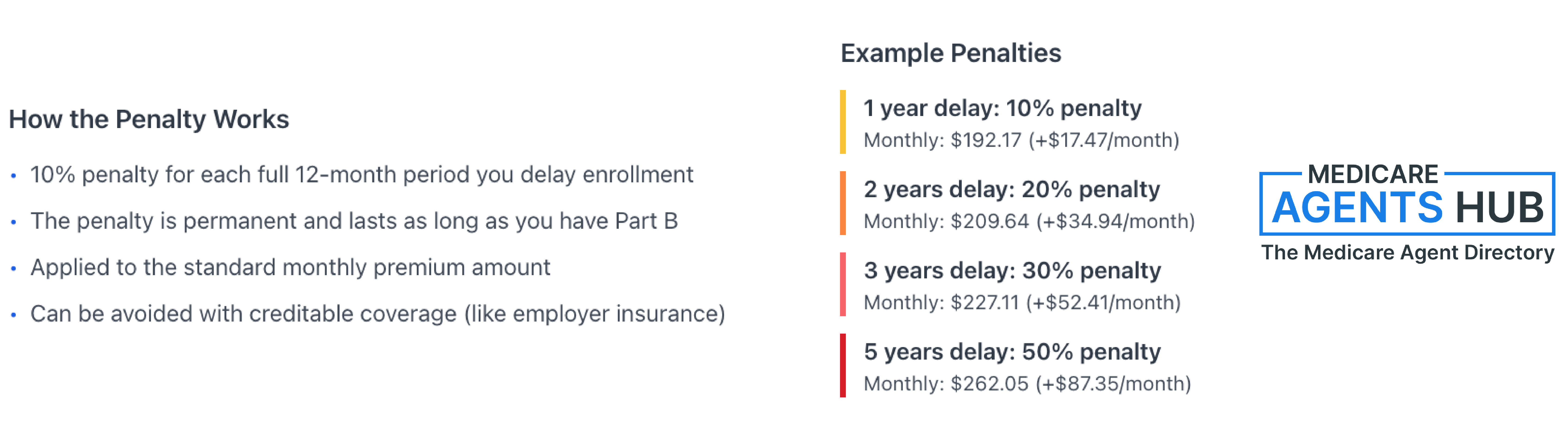

The Initial Enrollment Period is a key concept that causes a lot of confusion. This period usually starts three months before the month you turn 65 and continues for three months after, giving you a seven-month window to enroll. Missing this period can lead to penalties and gaps in coverage.

For Part B, which many people must actively enroll in, delaying enrollment without qualifying for a special exception can result in a permanent penalty added to your monthly premium. That penalty is calculated as a percentage of the standard premium for every full year you delayed signing up.

Assuming Employer Health Insurance Covers Everything

Some retirees think having employer health insurance means they do not need to enroll right away. Employer coverage can be different from Medicare coverage. If your employer coverage meets Medicare’s standards, it may allow you to delay enrollment without penalty. This is called creditable coverage. But not all employer plans are considered creditable, especially if the employer has fewer than twenty employees or the plan isn’t as comprehensive as Medicare requires. If your coverage is not considered creditable and you delay enrollment, you could face penalties or gaps in benefits.

It’s also important to get written proof that your employer plan is creditable before you delay enrollment. If you wait until later to provide documentation, you may lose your chance for a special enrollment period and have to wait for the next general enrollment period, usually early in the year.

Skipping Prescription Drug Coverage

Even if you are healthy and do not take medications now, skipping prescription drug coverage when you first become eligible can lead to a penalty. If you decide later that you need this coverage and you went more than 63 days without comparable drug coverage after your initial eligibility, a late enrollment penalty may be added to your monthly cost. This penalty is calculated as a percentage of the national base beneficiary premium for each month you were without coverage, and it stays with you as long as you keep the coverage.

Having employer or other drug coverage that Medicare considers creditable can help you avoid this penalty. If your employer plan includes drug benefits that are considered creditable, make sure you receive documentation each year so that you and Medicare know you had appropriate coverage.

Ignoring the Need to Review Coverage Annually

Once you are enrolled, many retirees assume they are done making decisions. It is actually a good idea to review your coverage each year during the annual enrollment period. Plans can change their benefits, drug formularies, and provider networks every year. Without reviewing your plan, you could end up with a provider you no longer see in your network or prescriptions that cost more than they should.

Taking a little time each fall to look at your plan materials and compare options can help you stay with the best coverage for your needs and budget.

Is it better to update your Medicare plan often, or to get a plan that will work long term?

It might not be better to update your plan often - JUST to update it. And selecting a plan that will work long-term is great, but..... Always at least review your Medicare plan every year.Relying Only on Online Tools Without Checking Details

Online tools and portals can be helpful when exploring coverage options, but they are not perfect. Information displayed for providers and plan details can sometimes be confusing or outdated. It is always wise to verify important details directly with your plan or a trusted Medicare advisor. This way you can avoid unexpected costs or surprises when you receive care.

Don't Make These Same Mistakes

Your first year of Medicare eligibility should be empowering, not overwhelming. Taking time to understand deadlines, how your employer coverage works with your new benefits, and the importance of enrolling in drug coverage can save you money and ensure you have the coverage you want when you need it.

Planning ahead and staying informed will help you enjoy your retirement years with confidence and peace of mind. For a deeper look at the kinds of issues that catch people off guard, read about 10 real frustrations seniors face with Medicare and how agents address them. And if you’re not sure what to ask, start with the questions most seniors don’t think to raise. If anything seems unclear, don’t hesitate to reach out to a trusted expert or call the official Medicare helpline for help.