What Most Seniors Don't Ask About Medicare - But Should

-

Last Updated July 21, 2026

Every year, thousands of people turn 65 and start their Medicare journey. Most ask about premiums. Many ask about doctors. Almost everyone wants to know about dental and vision perks.

But the questions that actually protect you? The ones that could save you from financial surprises five, ten, or fifteen years down the road? Those rarely come up.

We asked licensed Medicare agents across the country a simple question: What do you wish every client would ask before choosing a plan? Their answers point to four blind spots that trip up beneficiaries over and over again. For a broader look at the questions agents think you should ask about Medicare, we have a companion piece that covers even more ground.

The HSA Trap: Why Taking Part A Can Cost You

If you're still working past 65 and contributing to a Health Savings Account through your employer, here's something that catches people off guard: the moment you enroll in any part of Medicare, you can no longer contribute to your HSA.

That includes Part A, which many people sign up for automatically when they file for Social Security. Even if you don't need Medicare yet because your employer plan is solid, taking Part A kills your HSA eligibility on the spot.

What's the most important question I should be asking about Medicare that I probably haven't thought of yet?

I would say, if someone is staying working on employer coverage that if they have HSA at work, not to take any Medicare because you can no longer contribute to HSA if you do. But if you do not have HSA you should take part A only at 65.The IRS is strict on this. If you contribute to an HSA after your Medicare coverage starts, you'll face tax penalties. And here's the wrinkle - Medicare Part A can be applied retroactively up to six months. So if you sign up for Part A in October, your coverage might be backdated to April, and any HSA contributions you made during that window become a problem.

If you're still working and have an HSA, talk to an agent or financial advisor before enrolling in anything. The savings you've been building in that HSA could be undermined by a single enrollment decision. For a deeper look at the timing involved, check out our guide on whether you need Medicare if you're still working past 65.

The Medigap Underwriting Window You Can't Get Back

When you first enroll in Medicare Part B, you get a six-month window called the Medigap Open Enrollment Period. During those six months, insurance companies must sell you any Medigap plan they offer - no health questions, no denial, no higher rates because of a pre-existing condition.

Once that window closes, the rules change completely. In most states, insurers can use medical underwriting. That means they can ask about your health history, charge you more, or flat-out refuse to sell you a policy.

What's the most important question I should be asking about Medicare that I probably haven't thought of yet?

One thing I see often is that people new to Medicare focus mainly on premiums or extra perks, but the long‑term impact of their choices is just as important. Many also never learn about their early Medigap opportunities, like their Guaranteed Issue window, state GI protections, or birthday rules until those options have already passed. These rules can make a huge difference in long‑term flexibility and affordability, which is why I focus on educating people upfront about both their immediate choices and how those decisions can affect them 5–10 years down the road.This is one of the most consequential decisions in all of Medicare, and most people don't even know the window exists until it's too late. If you pick a Medicare Advantage plan at 65 because the $0 premium looks attractive, and then five years later you develop a chronic condition and want to switch to Medigap for more predictable costs, you may face health questions that block the switch.

Agents see this play out constantly. The plan that looked great at 65 can become a trap at 75 if your health changes and your options have narrowed. For a side-by-side breakdown of how these two paths compare over time, read Pay Now or Pay Later: The Real Cost of Medicare Advantage vs. Medigap.

Long-Term Care: The Gap Medicare Won't Fill

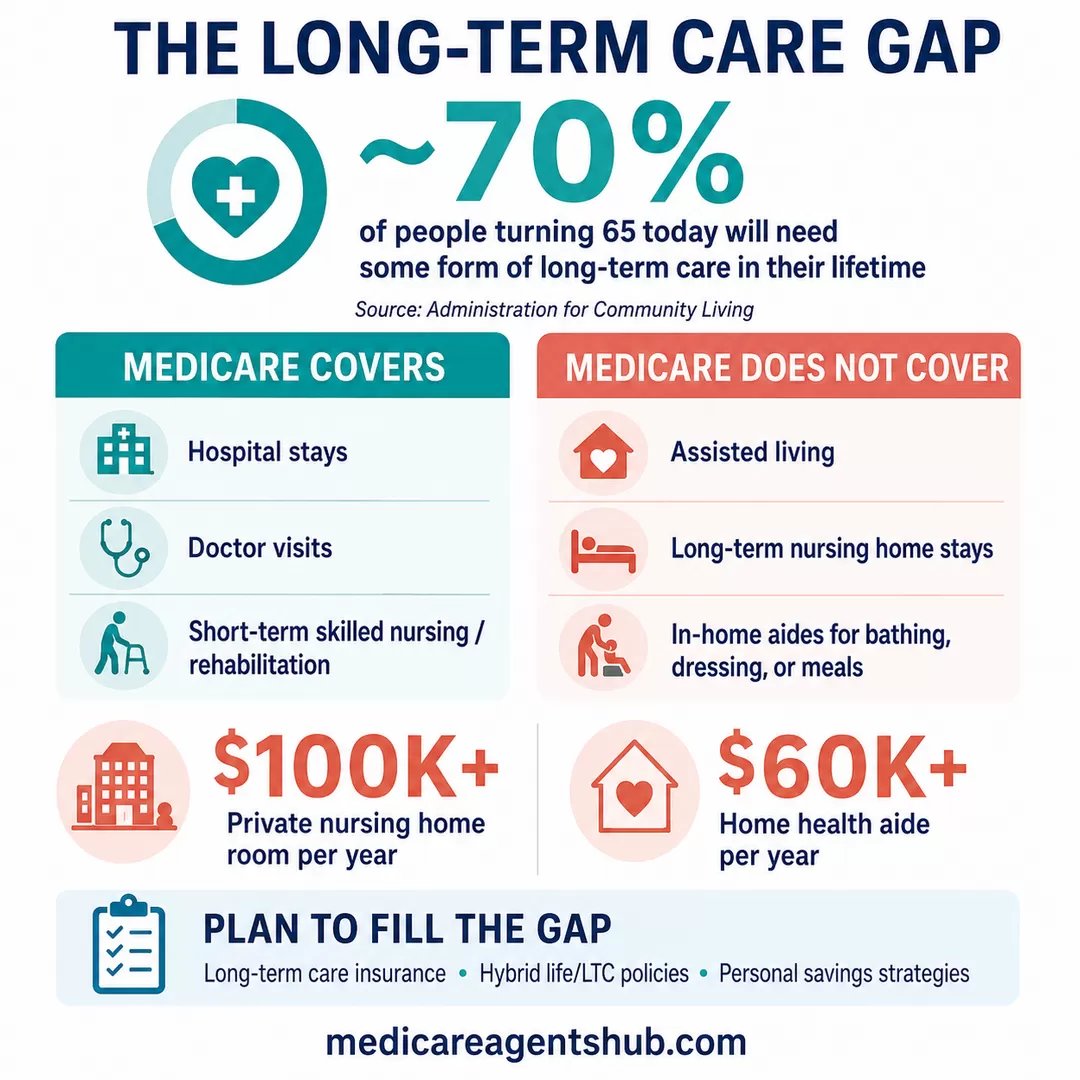

Here's a number that surprises most people: Medicare does not pay for long-term care. Not assisted living. Not nursing home stays beyond a short-term skilled nursing benefit. Not in-home aides who help with bathing, dressing, or meals.

The average cost of a private room in a nursing home runs over $100,000 per year. Home health aides cost $60,000+ annually. And roughly 70% of people turning 65 today will need some form of long-term care in their lifetime, according to the Administration for Community Living.

Yet most new beneficiaries never ask about it. They assume Medicare handles everything medical. It doesn't. Medicare covers hospital stays, doctor visits, and short-term rehabilitation. But the kind of care that drains retirement savings - the months or years of daily assistance - falls entirely outside Medicare's scope.

Planning options include long-term care insurance, hybrid life/LTC policies, and personal savings strategies. The key is starting the conversation early, ideally before health issues make coverage harder or more expensive to obtain. For a detailed look at what Medicare actually covers and where the gaps are, see Medicare's Role in Long-Term Care Coverage. You can also explore what seniors often misunderstand about Medicare and long-term care on our question pages.

"What's My Total Out-of-Pocket in a Bad Year?"

Most people shop for Medicare plans the same way they shop for car insurance - find the lowest monthly payment and move on. But the monthly premium tells you almost nothing about what a plan will cost if something goes seriously wrong.

A $0 premium Medicare Advantage plan might have a Maximum Out-of-Pocket (MOOP) of $8,300 or more. That means a single hospital stay, surgery, or cancer diagnosis could cost you thousands before the plan picks up 100% of covered services. Meanwhile, a Medigap Plan G with a higher monthly premium might leave you responsible for only the Part B deductible - around $257 in 2026 - no matter what happens.

What's the most important question I should be asking about Medicare that I probably haven't thought of yet?

“What is my total out-of-pocket risk for the year if something serious happens?”Most people focus on:

$0 premiums

Extra benefits

…but miss the big picture cost.

What this question uncovers:

Your maximum out-of-pocket (MOOP)

Hospital and specialist costs

How your plan handles worst-case scenarios

Why it matters:

The right plan isn’t just about saving money when you’re healthy—it’s about protecting you financially if you’re not.

Bottom line:

Don’t just ask “What’s the premium?”

Ask “What could this cost me in a bad year?”

That’s where the real differences between plans show up.

This is the question that separates informed Medicare decisions from risky ones. Instead of asking "What's the cheapest plan?" ask "What could this plan cost me if I have a heart attack, a cancer diagnosis, or a major surgery this year?"

Agents call this the "bad year" question, and it's the single fastest way to understand whether a plan truly protects you or just looks good on paper. If you want to see more of the costs that catch first-time enrollees off guard, take a look at 5 Hidden Medicare Costs That Blindside First-Time Enrollees.

How Will My Coverage Handle Me at 80, Not Just 65?

At 65, most people are relatively healthy. They're thinking about today's doctors, today's medications, today's budget. And that makes sense - you want a plan that works right now.

But Medicare is a decision you live with for decades. The plan you choose at 65 shapes what's available to you at 70, at 80, at 90. And as agents repeatedly point out, roughly 80% of lifetime healthcare spending happens after age 60. Your needs at 80 won't look anything like your needs at 65.

Do I really need help in figuring out what's best for me as for as Medicare Planning?

Decisions you make now regarding Medicare have consequences for the rest of your life. Certain decisions you make now can preclude you from participating in all the options available to you in the future. Medicare broker's services are free to you, why not consult with a professional that knows all of the rules and regulations, so that the choices you make now won't haunt you down the road.The agents who answered our questions came back to this theme again and again: think long-term. Your plan should protect you not just on a good day, but on your worst day. Not just this year, but in the years when your health is less predictable and your options for switching may be limited.

The Checklist You Didn't Know You Needed

Based on what agents told us, here are the questions worth asking before you lock in any Medicare plan:

- Am I contributing to an HSA? If yes, understand exactly when to stop contributions relative to your Medicare enrollment date.

- Do I understand my Medigap Open Enrollment window? Those six months after Part B starts are your one guaranteed shot at getting a supplement plan without health screening.

- What's my plan for long-term care? Medicare won't cover it. Have you looked into LTC insurance, hybrid policies, or other funding strategies?

- What's my total out-of-pocket in a bad year? Look at the MOOP, not just the premium. Compare what you'd owe under different plan types if you had a major health event.

- How will this plan work for me at 80? Consider whether you'll have the flexibility to change plans later if your health changes and your needs grow.

None of these questions are complicated. But they're the ones that most people skip - and the ones that agents say make the biggest difference in whether a beneficiary ends up protected or exposed.

If you're not sure where to start, connect with a local Medicare agent who can walk through these scenarios with you. The conversation is free, and it could be the most valuable 30 minutes you spend before making a decision that lasts the rest of your life.