What an HSA Can and Can't Pay For Once You're on Medicare and the Medigap Exception Almost Everyone Misses

-

May 17, 2026

Your Health Savings Account was one of the best tax tools you had while you were working. Tax-deductible going in, tax-free coming out for medical expenses, and the balance rolls over forever. Then you sign up for Medicare, and the rules change overnight. Not all of them, though, and that partial shift is where the confusion lives.

Across more than 80 agent answers on HSA use after retirement, a clear consensus emerges: you can still spend your existing HSA dollars on most Medicare costs, but you cannot add another dime to the account once any part of Medicare kicks in. And one specific expense, Medigap premiums, is carved out entirely.

The Contribution Cutoff: Why It Hits the Moment Medicare Starts

This is the rule that trips people up more than any other. The day you enroll in any part of Medicare, including Part A alone, you lose eligibility to contribute to your HSA. It does not matter that Part A is free for most people. It does not matter that you are still working full-time with an HDHP through your employer. Enrollment is the trigger, not premiums or claims.

The restriction is absolute: once you enroll in Medicare, you can no longer contribute to your HSA. And there is a retroactive wrinkle that makes timing critical. Medicare Part A is often retroactive by up to six months, so if you contributed to your HSA during that lookback window, those contributions become excess and trigger a 6% tax penalty for each year they remain in the account.

That retroactive piece deserves its own section, because it is where high earners and people who delayed enrollment get burned.

The 6-Month Retroactive Part A Trap

When you sign up for Medicare after age 65, Social Security can backdate your Part A coverage by up to six months. If you were contributing to an HSA during that retroactive window, every one of those contributions is now an over-contribution subject to a 6% excise tax for each year the excess stays in the account.

The timing of when to stop HSA contributions depends on your situation. If you are applying for Medicare after age 65, particularly through a Special Enrollment Period after leaving employer coverage, stop HSA contributions at least six months before you apply. Premium-free Part A can be backdated up to six months from your application date, so any contributions during that retroactive window become excess. If you are enrolling during the Initial Enrollment Period around age 65, stop contributions before your Medicare coverage effective date. In either case, the key is knowing your Medicare start date and working backward from there.

I’m 67, working full time, and previously had a 4-month job gap. I enrolled in Medicare A and B to avoid penalties, but SSA won’t let me disenroll from A. I haven’t claimed Social Security and don’t need Part A, which blocks my HSA. What can I do?

Medicare Part A is like a one-way door.Once you walk through it after age 65, the government doesn’t let you walk back out unless you also give up your right to Social Security.

Since you haven’t claimed Social Security yet, you wouldn’t owe anything back — but you’d also be giving up your future right to premium‑free Part A.

Most people decide it’s not worth it. The simpler option is to keep Part A and stop HSA contributions going forward.

This is a particularly painful trap for people who enrolled in Part A during a job gap and then went back to work. As multiple agents explained in response to a question about disenrolling from Part A to restore HSA eligibility, dropping Part A after age 65 generally requires withdrawing your entire Medicare application, and if you have claimed Social Security, repaying every benefit you received. For most people, that is not a realistic option. The practical answer is to keep Part A and stop contributing to the HSA going forward.

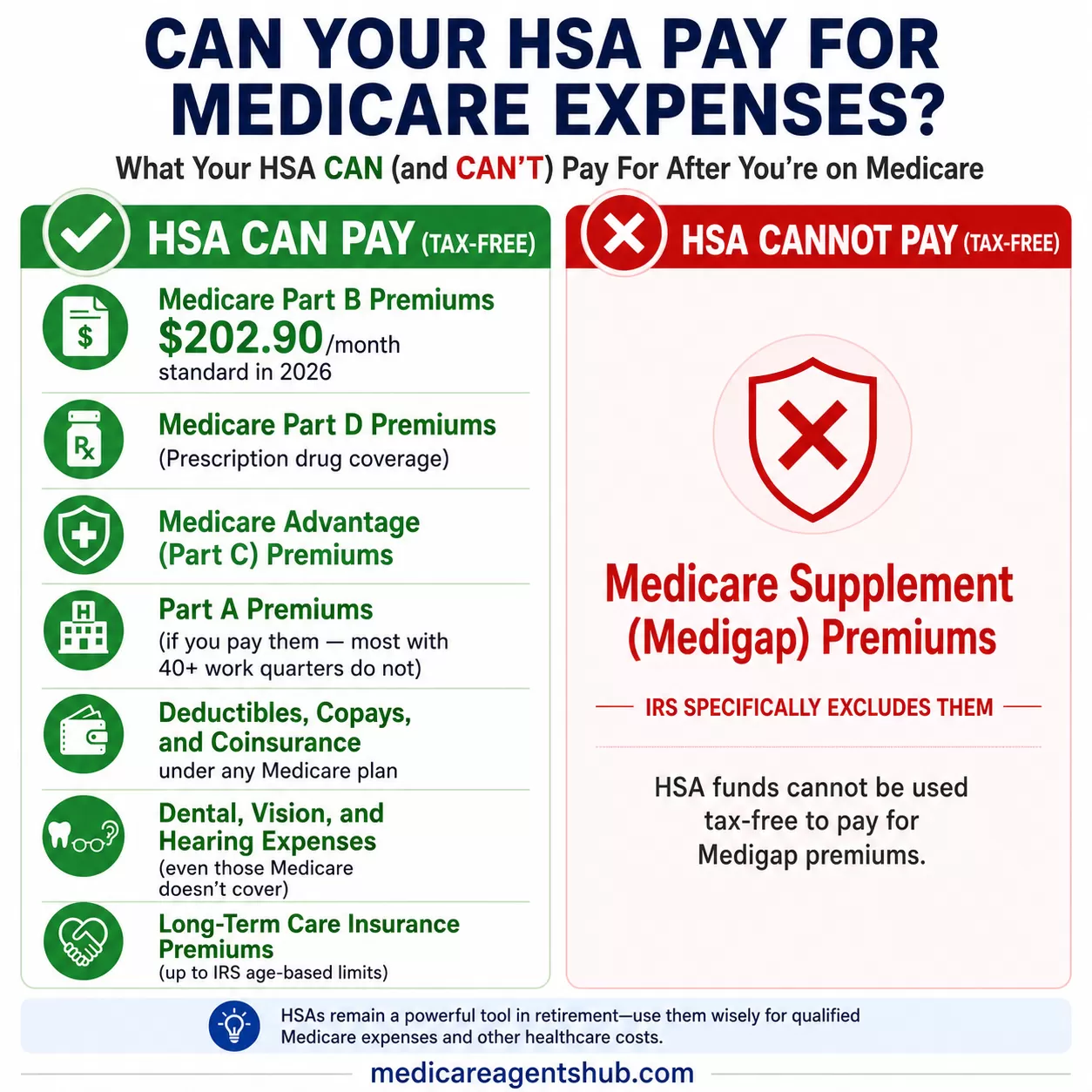

What Your HSA Can Still Pay For

Once you are on Medicare, you cannot add to the account, but the money already in it remains yours and retains its tax-free status for qualified medical expenses. Agents across the board agree on what qualifies:

- Medicare Part B premiums (the standard $202.90/month in 2026, or more if you are subject to IRMAA surcharges)

- Medicare Part D premiums (prescription drug coverage)

- Medicare Advantage (Part C) premiums

- Part A premiums, if you pay them (most people with 40+ quarters of work history do not)

- Deductibles, copays, and coinsurance under any Medicare plan

- Dental, vision, and hearing expenses, even those Medicare does not cover

- Long-term care insurance premiums, up to IRS age-based limits

After age 65, you can also withdraw HSA funds for non-medical expenses without the 20% penalty that applies to younger account holders. You will owe income tax on those withdrawals, but no penalty. That flexibility makes an HSA function like a traditional IRA once you hit 65, with the added benefit that medical withdrawals remain completely tax-free.

Can I use a health savings account (HSA) to pay Medicare premiums after I retire?

Yes, you can use your Health Savings Account (HSA) to pay for Medicare premiums andother qualified medical expenses tax-free after you retire.

Eligible expenses include premiums for Medicare Parts A, B, C (Advantage) and D, as well

as deductibles and co-pays. However, you cannot use your HSA for Medical Supplement

(Medigap) premiums.

Key Rules for Using and HSA with Medicare:

Stop Contributions: Once you enroll in Medicare, you can no longer contribute to your HSA.

Qualified Expenses: Funds must be used for qualified medical expenses, which include

Medicare Premiums (excluding Medigap), long-term care insurance, and dental/vision

services.

Tax-Free Usage: You can pay for these expenses tax-free, even if you are over 65.

Non-Qualified Expenses: If you use finds for non-qualified expenses after age 65, you

will pay income tax on the withdrawal, but no penalty.

Retroactive Penalty Warning: Medicare Part A of often retroactive by up to 6 months. If

you contribute to your HSA during this retroactive period, you may fact a 6% tax penalty

on the excess.

The Medigap Exception: Why Supplement Premiums Don't Qualify

Here is where nearly every agent lands on the same answer, and it catches retirees off guard. You cannot use HSA funds tax-free to pay Medicare Supplement (Medigap) premiums. The IRS specifically excludes them from the list of qualified medical expenses.

This creates an odd asymmetry. You can pay your Medicare Advantage premium with HSA dollars, but not your Plan G or Plan N premium. You can pay your Part D premium, but not the Medigap premium that sits alongside it. For retirees doing the math on Medigap vs. Medicare Advantage, this tax treatment difference is a real factor that rarely shows up in plan comparison tools.

A small number of agents described the Medigap exclusion as a "gray area," but the majority, and the IRS guidance itself, are clear: Medigap premiums are not a qualified HSA expense. If you withdraw HSA money to pay them, you will owe income tax on the withdrawal (though no penalty after age 65).

Can I use a health savings account (HSA) to pay Medicare premiums after I retire?

You can use a HSA to pay for some Medicare expenses but not all.You can use HSA funds to pay for:

Medicare Part B premiums (medical insurance)

Medicare Part D premiums (prescription drug coverage)

Medicare Advantage (Part C) premiums

Out-of-pocket medical expenses like deductibles, copays, and coinsurance under Medicare

You cannot pay for Medigap supplements out of your HSA.

What Agents Actually Tell Clients to Do

The strategic advice agents give around HSAs and Medicare is consistent across dozens of answers:

Stop Contributions Before Medicare Kicks In

Do not wait until your Medicare start date to figure this out. If you are applying for Medicare after age 65 (for example, through a Special Enrollment Period after leaving employer coverage), stop HSA contributions at least six months before you apply, because premium-free Part A can be backdated up to six months from the application date. If you are enrolling during the Initial Enrollment Period around age 65, stop contributions before your coverage effective date. And if you are working past 65 with employer coverage and plan to delay Medicare, you can keep contributing as long as you have not enrolled in any part of Medicare, including Part A.

Maximize the Balance Before Medicare

In the years before enrollment, contribute the maximum allowed. For 2026, that is $4,400 for self-only coverage and $8,750 for family coverage, plus a $1,000 catch-up contribution if you are 55 or older. Every dollar in the account becomes a tax-free medical spending resource for the rest of your life.

Use HSA Funds Strategically in Retirement

Agents recommend using HSA dollars for the expenses that hit hardest: Part B premiums (especially if IRMAA pushes yours higher), out-of-pocket costs that surprise new enrollees, dental and vision work that Original Medicare does not cover, and Part D copays on expensive medications. Save non-HSA retirement funds for Medigap premiums and other non-qualified expenses.

Coordinate with a Spouse

If one spouse is on Medicare and the other is still working with an HDHP, the working spouse can continue contributing to their own HSA. The funds can later be used for either spouse's qualified medical expenses. This is a common scenario for couples with an age gap, and agents flag it as one of the most underused planning strategies.

Can I use a health savings account (HSA) to pay Medicare premiums after I retire?

Yes you can! You can use an HSA to pay for Medicare part B premiums, Medicare Advantage premiums (if you have any), Medicare part D premiums, as well as any out of pocket co-pays, deductibles, or co-insurance that you might have. You can also use it for Dental, Vision, Hearing expenses. The one thing you CAN'T use an HSA for is Medicare Supplement premiums.A Proposed HSA Change That Did Not Make the Final Bill

During the drafting of the One Big Beautiful Bill Act, one proposal drew significant attention from Medicare-eligible savers: a change that would have allowed HSA contributions to continue after Medicare Part A enrollment.

That specific change did not survive the final version of the legislation. The proposal to allow HSA contributions after Medicare Part A enrollment was ultimately dropped from the bill before it was signed into law. The HSA-related provisions that did make it into the final law focused on other areas: allowing telehealth and remote care services to be covered before meeting HDHP deductibles, permitting bronze and catastrophic health plans to qualify as HDHPs, and expanding HSA-eligible expenses to include direct primary care arrangements.

Can I use a health savings account (HSA) to pay Medicare premiums after I retire?

Yes. HSA expenses can be withdrawn tax-free for eligible medical expenses after age 65.Note, there are additional changes included in the recently passed “Big Beautiful Bill” that will soon affect HSAs. For example, up until recently, the rule has always been that you may only make HSA contributions until you enroll on Medicare. That rule will be changing.

The current rule stands: once you enroll in any part of Medicare, you cannot contribute to an HSA. Talk to a licensed Medicare agent and your tax advisor if you have questions about how this affects your retirement planning.

The Bottom Line for Your HSA and Medicare

| Expense | HSA Eligible (Tax-Free)? |

|---|---|

| Medicare Part B premiums | Yes |

| Medicare Part D premiums | Yes |

| Medicare Advantage premiums | Yes |

| Part A premiums (if applicable) | Yes |

| Medigap/Medicare Supplement premiums | No |

| Copays, coinsurance, deductibles | Yes |

| Dental, vision, hearing | Yes |

| Long-term care insurance premiums | Yes (up to age-based IRS limits) |

| New HSA contributions after Medicare enrollment | Not allowed (current law) |

An HSA does not stop being useful the day Medicare starts. It stops growing, but the balance you built while working can cover a significant chunk of your healthcare costs in retirement. The key is knowing the rules, stopping contributions on time, and spending the money on the right expenses. For help putting the pieces together, find a Medicare agent near you who can walk through the numbers alongside your financial advisor.