Your HSA and Medicare: The Six-Month Rule Almost Nobody Warns You About

Richard turns 66, still working, still happy with his employer health plan. He decides to keep contributing to his health savings account because the tax break is too good to pass up. A year later he finally retires and signs up for Medicare. A few months after that, his tax preparer delivers some unwelcome news. Several thousand dollars of his HSA contributions were never allowed, and the IRS wants a penalty on top of it.

This is one of the most common and most painful surprises that lands on people who delay Medicare past 65. The rules are not hidden, but they are scattered across HSA law and Medicare timing rules that almost never get explained together. Many beneficiaries are surprised to learn that the trap springs from a Medicare feature designed to help them.

Here is what is actually going on, and how to stay out of trouble.

Medicare and HSAs Don't Perfectly Mix

A health savings account has one strict requirement. To put money in, you must be covered by a qualifying high deductible health plan and you must have no other disqualifying coverage. Medicare counts as disqualifying coverage. The day any part of your Medicare begins, even just the free Part A that most people get at no premium, your HSA eligibility ends.

Notice the careful wording. Medicare does not stop you from owning an HSA or spending the money in it. You can use the balance tax free for qualified medical costs for the rest of your life. What ends is your ability to add new money. Once you are enrolled in Medicare, the contributions stop. Period.

For someone who signs up for Medicare at 65 and walks away from work, this is simple. They stop contributing, they enroll, life goes on. The people who get burned are the ones who keep working past 65 and try to hold onto both the employer plan and the HSA.

Working Past 65 Changes the Story

If you have qualifying employer coverage through a company with 20 or more employees, you are allowed to delay Medicare without penalty. Plenty of people do exactly that. They like their plan, they want to keep funding the HSA, and the law lets them wait.

The problem is what happens when they finally decide to enroll. Most people assume Medicare starts the month they sign up. For Part A, that is often not true.

If a senior is turning 65 but still working, should they enroll in Medicare or delay it?

Enroll in Part A; it's usually free. Delay Part B only if your employer/spouse's plan has 20 or more employees. There's no late penalty that way and you have an 8-month SEP to enroll after your employer coverage. If under 20 employees, I would enroll fully at 65.The Six-Month Rule

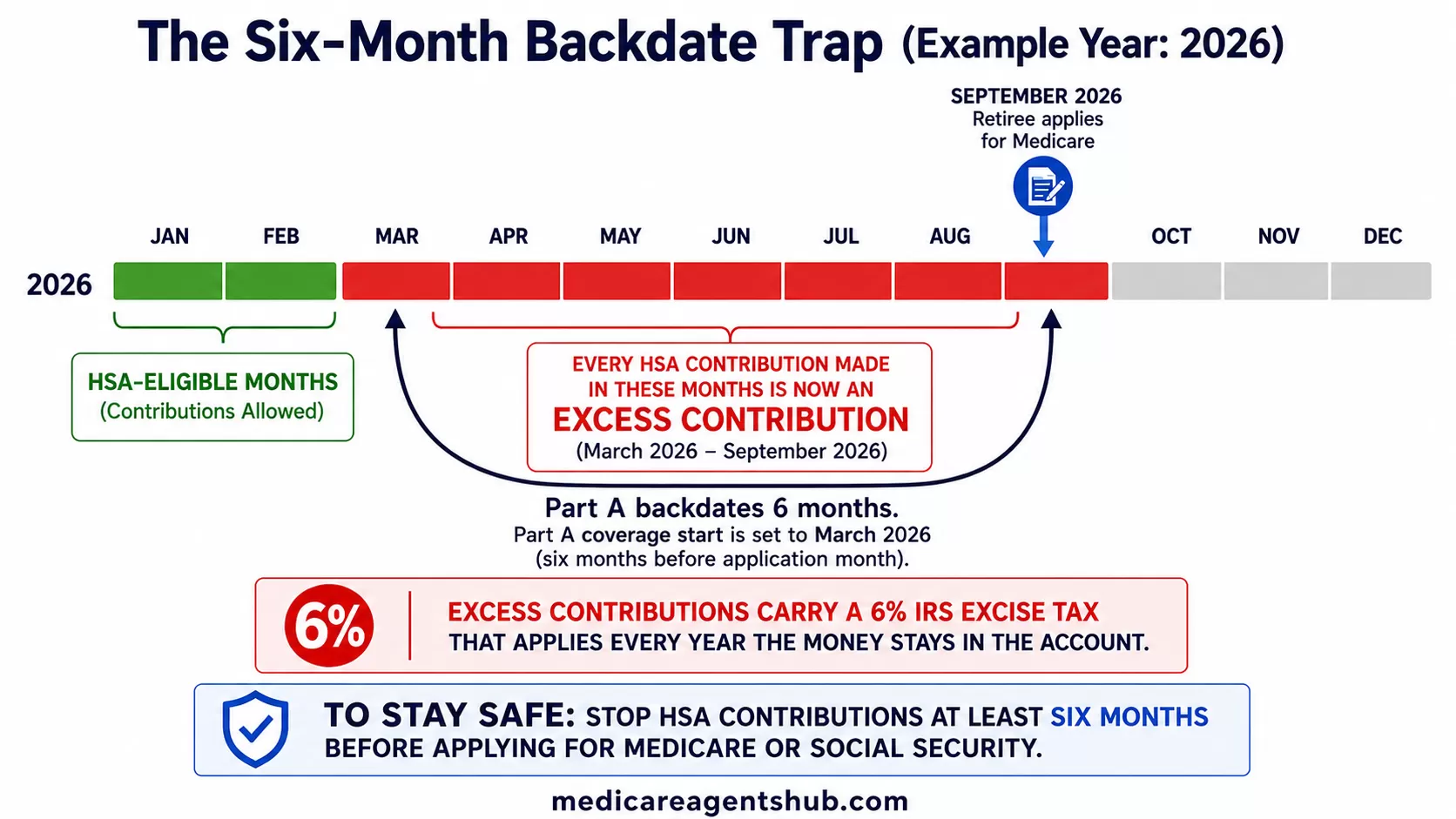

When you apply for Medicare Part A after age 65, the government does not start your coverage on your application date. It backdates it. Part A coverage begins up to six months before the month you apply, though never earlier than the month you turned 65.

The reason behind this is reasonable. The rule exists so that someone leaving a job does not end up with a gap in coverage during the handoff from employer insurance to Medicare. In most situations the retroactive start is a quiet benefit nobody even notices.

For an HSA holder, that same retroactive start is a landmine. Your HSA eligibility does not end on the day you applied. It ends on the day your backdated Part A actually began, which could be six months earlier. Every dollar you contributed during those backdated months was contributed while you were technically enrolled in Medicare, which means you were not eligible to contribute at all.

Say you keep working and contributing to your HSA through the spring of 2026. In September 2026 you retire and apply for Medicare. Social Security looks at your application, backdates your Part A six months, and sets your coverage start date to March 2026.

From the HSA point of view, you were only eligible to contribute in January and February. Everything you put in from March through September is now an excess contribution. It should not have gone in, and the IRS treats it as a mistake that needs to be cleaned up.

What the Penalty Looks Like

Excess HSA contributions carry a six percent excise tax. That tax is not a one time hit. It applies every single year the excess money stays in the account. If you ignore it, the penalty quietly compounds while you are not looking.

There is also the matter of any employer contributions and any tax deduction you took on the money you put in. Those have to be unwound too. The cleanup is doable, but it usually means pulling the excess out along with any earnings it generated and reporting the correction on your tax return. None of it is fun, and all of it is avoidable with a little forward planning.

How to Protect Yourself

The fix is mostly about timing, and it comes down to one habit. If you are over 65 and still contributing to an HSA, stop your contributions at least six months before the month you plan to apply for Medicare or for Social Security benefits.

That last point trips people up, so it is worth saying plainly. Claiming Social Security after 65 automatically enrolls you in Medicare Part A. You do not get to keep one without the other. So the six month clock applies not just to a deliberate Medicare application, but to the day you decide to start your Social Security checks.

A few practical steps make this manageable. Map out your retirement date first, then count backward six months and mark that as your contribution cutoff. If your contributions come straight out of your paycheck, tell your payroll or benefits office to shut them off in time, since those deductions will keep running until someone stops them. If you have already contributed too much, talk to your HSA custodian and a tax professional about a corrective distribution before the filing deadline, which removes the excess and the earnings before the penalty digs in.

One more thing worth knowing. The contribution limit for the year you become Medicare eligible is prorated. You only get to contribute for the months you were actually HSA eligible, not the full annual amount. People who front load their entire yearly contribution in January often discover later that they were only entitled to a fraction of it.

The Bigger Lesson

The HSA and Medicare collision is a perfect example of why the timing of Medicare matters as much as the choices inside it. Two rules that each make sense on their own combine into a trap when nobody is watching the calendar. The money you saved in your HSA is still yours and still valuable. The goal is simply to stop adding to it at the right moment so a helpful piece of Medicare design does not turn into a tax bill.

If you are still working at 65 and funding an HSA, the single smartest move is to flag this years before you retire. Put the six month buffer on your calendar now. Future you will be grateful.

About the Author: Taylor Langlois is an independent Medicare broker and the owner of Trinity Assurance Group, based in Wichita, Kansas. Taylor works with Medicare beneficiaries as well as clients across ACA health plans, life insurance, and annuities. Much of that work involves untangling the timing and coordination questions that confuse people most as they approach and enter retirement. Taylor writes to help beneficiaries understand the rules that rarely make it into the standard Medicare overview.