How Medicare and Social Security Work Together at Age 65

-

March 4, 2026

Medicare and Social Security are two of the most important programs for Americans approaching retirement, and they're more connected than most people realize. Social Security determines when and how you're enrolled in Medicare, how much you pay for it, and even how your premiums are collected.

But they're not the same program, and the decisions you make about one can directly impact the other. Understanding how Medicare and Social Security interact helps you avoid penalties, plan your retirement income more effectively, and make sure you're not overpaying for coverage.

The Basic Relationship Between Medicare and Social Security

Medicare and Social Security are both federal programs, but they serve different purposes:

- Social Security provides retirement, disability, and survivor income benefits

- Medicare provides health insurance, primarily for people 65 and older

The connection between them comes down to three things:

- Work history. The same payroll taxes (FICA) that fund Social Security also fund Medicare Part A. If you've worked and paid taxes for at least 10 years (40 quarters), you qualify for both.

- Enrollment. Social Security handles Medicare enrollment. You sign up through the Social Security Administration, not through Medicare directly.

- Premium payments. If you're receiving Social Security benefits, your Medicare Part B and Part D premiums are automatically deducted from your Social Security check.

Auto-Enrollment: When Medicare Happens Automatically

One of the biggest points of confusion is whether you need to do anything to get Medicare. The answer depends on whether you're already receiving Social Security.

If You're Already Collecting Social Security at 65

If you started taking Social Security benefits before age 65, you'll be automatically enrolled in Medicare Part A and Part B when you turn 65. Your Medicare card will arrive in the mail about three months before your 65th birthday.

You don't need to apply. It just happens. However, you do have the option to decline Part B if you don't want it yet (for example, if you're still covered by an employer plan). If you don't actively opt out, Part B kicks in and the premium starts being deducted from your Social Security check.

What happens if I am already retired and collecting Social Security when I turn 65?

If you are already retired and collecting Social Security, you will automatically be enrolled in Medicare Part A and Part B. You will receive your Original Medicare Card in the mail 2-3 months in advance of your 65th birthday and your benefits will be effective with the first day of the month that you turn 65. If you turn 65 on the first day of the month, your Medicare benefits will be effective with the month before your 65th birthday.Once you receive your Medicare card, you should be in contact with a broker to help you decide what additional insurance needs you have. You will need to enroll in a Part D plan (prescription drug plan) at 65. To avoid penalties, you need to enroll in a Part D plan during your initial enrollment period (IEP), which is a seven month period- beginning with the three months before you turn 65, your 65th birthday month, and the three months following.

In addition to your Part D enrollment, you will want to consider whether a Medicare Supplement or Medicare Advantage plan is best for you. Everyone's needs are individual, so it is best to speak with an independent broker that can help you navigate the complexities of Medicare- ensuring you have the best possible health coverage for your personal needs.

If You're NOT Collecting Social Security at 65

If you've delayed Social Security, which many people do to maximize their monthly benefit, you will NOT be automatically enrolled in Medicare. You need to actively sign up during your Initial Enrollment Period (IEP), the 7-month window centered around your 65th birthday.

This is where people get tripped up. They assume Medicare will just start because they turned 65, but without Social Security triggering auto-enrollment, nothing happens unless you take action.

I'm planning to delay Social Security until age 70, but I'm turning 65 soon. How does this affect my Medicare enrollment?

Just because you delay drawing Social Security until 70 doesn't mean you can't enroll in Medicare at 65. You're still eligible for Medicare, and you should enroll during your Initial Enrollment Period to avoid potential penalties or delays in coverage.If your employer coverage is as good as Medicare coverage, you can delay accepting Medicare Part B, but you should still take Part A.

The only difference between taking Medicare Part B at 65 and waiting until you start drawing Social Security is that you have to pay the Part B premiums out-of-pocket until your Social Security begins. At that time, Medicare Part B premiums will be deducted from your Social Security before you receive your funds.

If You're on Social Security Disability

If you've been receiving Social Security Disability Insurance (SSDI) for 24 months, you're automatically enrolled in Medicare, regardless of age. When you turn 65, your coverage simply transitions from disability-based Medicare to age-based Medicare. There's nothing extra you need to do.

The exception: people with ALS (Lou Gehrig's disease) are enrolled in Medicare the same month their SSDI benefits begin, with no 24-month waiting period.

Delaying Social Security but Not Medicare

This is one of the most important things to understand: you can delay Social Security without delaying Medicare. They are independent decisions.

Many financial advisors recommend waiting until 67 (full retirement age) or even 70 to start Social Security, since your monthly benefit increases for every year you delay. But Medicare eligibility starts at 65 regardless of when you take Social Security.

The key takeaway: Even if you're delaying Social Security, you should still evaluate whether to enroll in Medicare at 65. If you don't have creditable employer coverage, failing to enroll on time can result in permanent late enrollment penalties.

If you delay both Social Security and don't have qualifying employer coverage, you could end up paying a Part B late enrollment penalty of 10% for every 12 months you were eligible but didn't enroll, and that penalty lasts for as long as you have Part B.

Still Working at 65? Here's Where It Gets Tricky

If you're still working at 65 and have health insurance through your employer (or your spouse's employer), the rules depend on the size of the employer:

- Employer with 20+ employees: Your employer plan is primary. You can safely delay Medicare Part B without penalty, as long as you enroll within 8 months of leaving the job or the coverage ending.

- Employer with fewer than 20 employees: Medicare is primary. You should enroll in Part B at 65 to avoid gaps in coverage and penalties.

Most people in this situation should still sign up for premium-free Part A at 65, since there's no cost. The one exception: if you're contributing to a Health Savings Account (HSA), enrolling in any part of Medicare makes you ineligible to contribute. You'll need to stop HSA contributions at least 6 months before enrolling in Part A to avoid tax penalties.

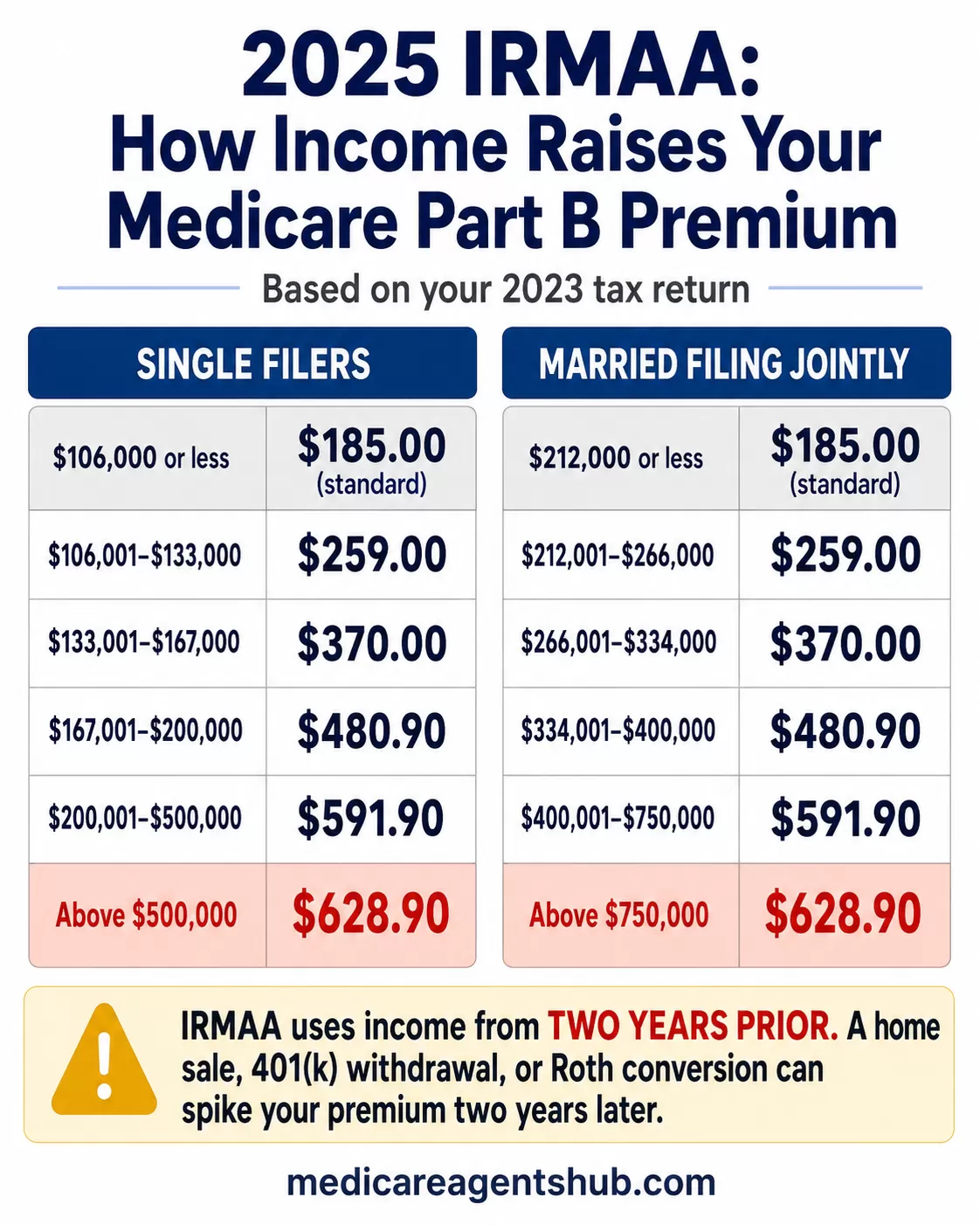

How Social Security Income Affects Your Medicare Costs (IRMAA)

Here's a connection that catches many retirees off guard: your income, including Social Security benefits, can increase your Medicare premiums.

It's called IRMAA (Income-Related Monthly Adjustment Amount), and it applies to both Part B and Part D. The Social Security Administration reviews your tax return from two years ago to determine whether you owe a surcharge on top of the standard premium.

2025 IRMAA Thresholds (Based on 2023 Tax Return)

- $106,000 or less$185.00/mo (standard)

- $106,001 – $133,000$259.00/mo

- $133,001 – $167,000$370.00/mo

- $167,001 – $200,000$480.90/mo

- $200,001 – $500,000$591.90/mo

- Above $500,000$628.90/mo

- $212,000 or less$185.00/mo (standard)

- $212,001 – $266,000$259.00/mo

- $266,001 – $334,000$370.00/mo

- $334,001 – $400,000$480.90/mo

- $400,001 – $750,000$591.90/mo

- Above $750,000$628.90/mo

Important: IRMAA uses your income from two years prior. So a large one-time event (selling a home, cashing out a 401(k), or a Roth conversion) can push you into a higher bracket two years later when you least expect it.

If your income has dropped significantly since the tax year being used (due to retirement, death of a spouse, divorce, or other life-changing events), you can appeal IRMAA by filing Form SSA-44 with the Social Security Administration.

How Medicare Premiums Are Deducted from Social Security

If you're receiving Social Security benefits, your Medicare premiums are automatically withheld from your monthly check. Here's how it works:

- Part B premium: Always deducted from Social Security (or billed directly if you're not collecting yet)

- Part D premium: Deducted from Social Security for standalone drug plans

- IRMAA surcharges: Also deducted from your Social Security check

If your Social Security benefit isn't large enough to cover the premiums, you'll be billed directly by Medicare.

One thing to be aware of: the “hold harmless” provision protects most beneficiaries from Part B premium increases that would reduce their Social Security check from one year to the next. If Social Security's cost-of-living adjustment (COLA) is small or zero, your Part B premium increase may be capped so your net Social Security payment doesn't go down. However, this protection does not apply to people subject to IRMAA or those who are new to Medicare.

Common Mistakes Where Medicare and Social Security Intersect

These are the most frequent, and costly, mistakes people make:

1. Assuming Medicare Will Start Automatically

If you're delaying Social Security, you must actively enroll in Medicare. No one is going to do it for you. Missing your Initial Enrollment Period can result in penalties and coverage gaps.

I thought I signed up for both Part A and B when I got my Social Security, but now I'm getting bills for Part B. Did I miss something during the enrollment period?

This is a common point of confusion, so you're not alone! Here's what's likely happening:Part A vs. Part B:

When you sign up for Social Security, you are automatically enrolled in both Medicare Part A and Part B — so you didn't miss an enrollment window. The key difference is the cost:

Part A:

generally premium-free for most people, because you paid into it through payroll taxes during your working years. That's why you may never see a bill for it.

Part B (medical insurance, doctor visits, outpatient care, etc.) has a monthly premium that most people pay. In 2026, the standard premium was $202.90/month, though it can be higher depending on your income (this is called IRMAA).

So the bills you're receiving for Part B are expected and legitimate, it doesn't mean something went wrong.

2. Not Realizing a 401(k) Withdrawal Will Spike Medicare Costs

Large retirement account withdrawals count as income for IRMAA purposes. A big Roth conversion or lump-sum distribution in one year can mean significantly higher Medicare premiums two years later.

3. Enrolling in Part A Too Early When You Have an HSA

Part A enrollment is retroactive up to 6 months. If you sign up for Social Security at 65 and are auto-enrolled in Part A, your HSA eligibility ends. Plan accordingly. Stop HSA contributions at least 6 months before enrolling.

4. Confusing Social Security Full Retirement Age with Medicare Eligibility

Social Security's full retirement age is 66–67 (depending on birth year). Medicare eligibility starts at 65. These are not the same milestone, and waiting until your Social Security full retirement age to enroll in Medicare is a common and costly mistake.

5. Not Reporting Life Changes to Social Security for IRMAA Relief

If you've retired, lost a spouse, or experienced another qualifying event that reduced your income, you don't have to wait for it to show up on your tax return. File Form SSA-44 with Social Security to request an IRMAA reduction based on your current income. For a closer look at what happens when a spouse dies, see our guide on how losing a spouse affects your Medicare and Social Security.

Key Dates and Timelines

- 3 months before turning 65: Initial Enrollment Period begins. If you're on Social Security, your Medicare card arrives around this time.

- Month you turn 65: Medicare coverage can start (depending on when in the month your birthday falls).

- 3 months after turning 65: Initial Enrollment Period ends. Missing this window without qualifying coverage triggers penalties.

- Every January: Social Security sends you a notice if IRMAA applies to your Medicare premiums for the year.

- Ongoing: Part B and Part D premiums are deducted from your Social Security check each month.

The Bottom Line

Medicare and Social Security are deeply intertwined: from how you enroll, to how you pay, to how your income affects your premiums. The biggest risk is making assumptions: assuming you're automatically enrolled when you're not, assuming your premiums are fixed when they're income-based, or assuming that delaying Social Security means delaying Medicare.

Getting this right means fewer penalties, lower costs, and a smoother transition into retirement. If you're approaching 65 and aren't sure how these pieces fit together for your specific situation, talking to an independent Medicare agent can help you build a plan that accounts for both your Social Security strategy and your healthcare needs.