Do Medicare Hospital Days Reset Every January? The Benefit-Period Rule Even Some Agents Get Wrong

-

July 5, 2026

Most health insurance plans reset on January 1. Your deductible goes back to zero, your out-of-pocket counter starts fresh, and everyone moves on. So when people ask whether their Medicare hospital days work the same way, the answer they expect is "yes." The actual answer, at least for Original Medicare, is "no, not exactly."

Bottom line: January 1 does not automatically give you a new set of Original Medicare hospital days.

This article is based on 318 answers from licensed Medicare agents responding to 89 related consumer questions on Medicare Agents Hub.

The Short Answer: Benefit Periods, Not Calendar Years

Under Original Medicare, Part A hospital days do not reset on January 1. They reset based on something called a benefit period. A benefit period starts the day you are admitted as an inpatient to a hospital or skilled nursing facility and ends only after you have been out of the hospital (or a skilled nursing facility) for 60 consecutive days. Once that 60-day clock runs out, a new benefit period begins, your hospital days reset, and a new Part A deductible applies.

This is a different system than most people are used to. If you are discharged from the hospital in November and readmitted in December (less than 60 days later), you are still in the same benefit period. You would not pay a new deductible, but you are also still drawing from the same pool of covered days. If you stayed out for a full 60 days and then went back, that would be a new benefit period with a fresh set of days and a new deductible of $1,736 for 2026.

Do my Medicare hospital days reset every year?

No. Medicare hospital days are based on a Benefit Period, not the calendar year. A benefit period starts the day you are admitted and ends when you've been out of the hospital (or SNF) for 60 consecutive days. Once you’ve gone 60 days without inpatient care, a new benefit period begins where you receive a new set of hospital days and a new deductible applies.| Medicare coverage type | Do hospital days reset Jan. 1? | What actually matters |

|---|---|---|

| Original Medicare Part A | No | Benefit periods and the 60-day rule |

| Medigap with Original Medicare | Medicare rules still apply | The supplement may pay many Part A costs |

| Medicare Advantage | Varies by plan | Plan-year MOOP + plan-specific hospital copays |

What Medicare Part A Actually Covers (and the Day Counts That Matter)

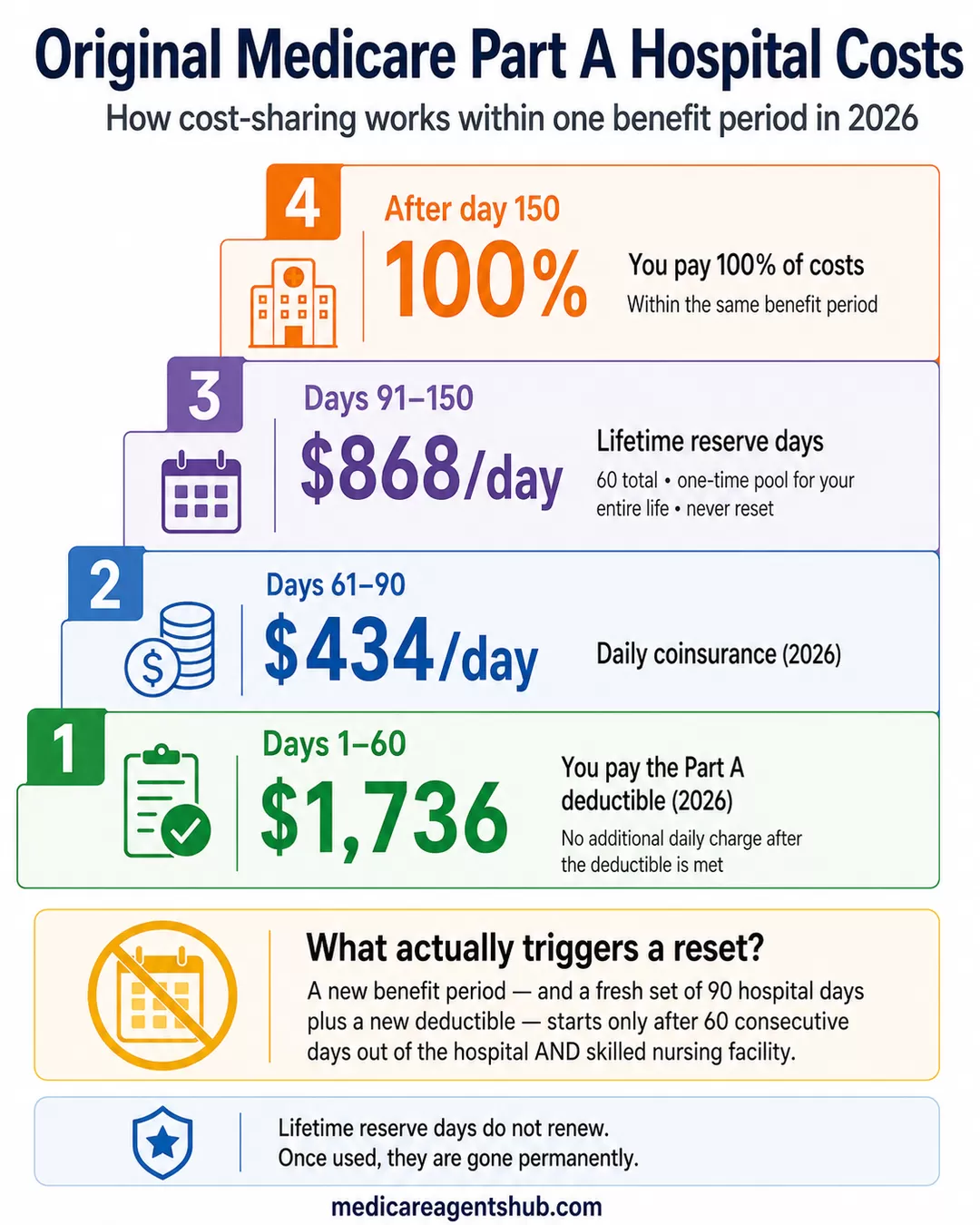

Within each benefit period, Medicare Part A covers inpatient hospital stays on a tiered schedule. For days 1 through 60, you pay only the Part A deductible. After that deductible is met, there is no additional daily charge during those first 60 days. From day 61 through day 90, a daily coinsurance kicks in at $434 per day in 2026. After day 90, you start drawing from your lifetime reserve days.

The 60 Lifetime Reserve Days

Every Medicare beneficiary gets exactly 60 lifetime reserve days. These are a one-time pool of extra hospital days that can be used after you have exhausted your 90 standard days within a single benefit period. The coinsurance for each reserve day is $868 per day in 2026. Once used, they are gone permanently. They do not renew, they do not reset at any point, and they cannot be replenished.

Agents consistently describe this as a "safety bank" or "backup supply." The 90 standard days renew with each new benefit period, but the 60 lifetime reserve days are a fixed pool for your entire life. After all 150 possible days (90 standard plus 60 reserve) are gone within a single benefit period, Medicare stops paying for that inpatient hospital stay under Part A for the rest of that benefit period, and the patient is responsible for 100% of costs.

A Medicare supplement broker told me something about "extra lifetime reserve hospital days". What are those and how do they work?

Every Medicare beneficiary gets a total of 60 lifetime reserve hospital days. Medicare covers hospital coverage for up to 90 consecutive days, per benefit period.Starting on the 91st consecutive day and each day thereafter, the beneficiary will begin drawing from their lifetime reserve days. After the lifetime reserve days are used, there is no additional coverage for hospitalization, and the beneficiary is responsible for 100% of the costs. Lifetime reserve days can be used once and after that they are gone.

That does not mean that Medicare won't cover hospital stays in the future, during a new benefit period, it just means that coverage after 90 days might be limited based on how many lifetime reserve days are left.

Medicare Supplement plans will cover an additional 365 days in the hospital after the lifetime reserve days are used, making that a key part of most seniors' Medicare strategy.

The Scenario That Catches Families Off Guard

Here is where the benefit-period system creates confusion. Picture this: a patient is hospitalized in November, discharged in early December, and readmitted to a different hospital (or the same one) in January. Many families assume January means a new year and a clean slate. It does not.

Because the patient has not been out of the hospital for 60 consecutive days between the November admission and the January readmission, they are still in the same benefit period. They do not pay a new deductible, which sounds like a benefit. But they are also continuing to draw from the same pool of covered days. If the November admission used 20 days and the January admission uses another 50, that is 70 days in one benefit period, and days 61 through 70 would each carry the $434 daily coinsurance.

For families dealing with a loved one who bounces between the hospital and a skilled nursing facility, this can be financially significant. The 60-day clock does not start until the patient is completely out of both the hospital and the SNF. Skilled care in a skilled nursing facility can keep the same benefit period open, so the 60-day clock does not necessarily start just because the person left the hospital.

Why Some Agents Get This Wrong (and Why They Are Not Entirely Wrong)

When Medicare Agents Hub asked agents whether hospital days reset every year, several answered "yes." One wrote flatly: "The Medicare Hospital days reset every year. The answer is yes." Another said: "Yes they do, and that can change from year to year so always check your Medicare booklet."

Those answers are not correct for Original Medicare, though they may reflect how some agents are thinking about Medicare Advantage plan-year cost sharing. But they are not made up out of thin air. The confusion has a source, and it is worth understanding.

Medicare Advantage plans operate on a plan year. When a beneficiary enrolls in a Medicare Advantage plan (Part C), their hospital cost-sharing follows the Advantage plan's rules, not Original Medicare's benefit-period structure. Most Advantage plans use a calendar-year cycle where cost-sharing resets on January 1. Some agents work primarily with Advantage plans and may be describing the system they know best without distinguishing it from Original Medicare.

One agent captured this perfectly: "Original Medicare resets based on time out of the hospital (60 days). Advantage and Supplement plans reset every plan year." That is the distinction many people miss.

Do my Medicare hospital days reset every year?

No, your Medicare hospital days do NOT reset every year.How it actually works:

Medicare uses a benefit period, not a calendar year

A benefit period starts the day you’re admitted and ends after 60 days in a row without inpatient care

What that means:

You get up to 90 hospital days per benefit period

If you go back in after 60 days out, your days reset

If not, you continue using the same benefit period.

How Medicare Advantage Handles Hospital Days Differently

On a Medicare Advantage plan, the Part A deductible from Original Medicare ($1,736 in 2026) generally does not apply. Instead, the Advantage plan sets its own hospital cost-sharing, which varies by plan. A common structure agents describe is a daily copay for the first 5 to 7 days of a hospital stay, followed by $0 per day after that.

For example, a plan might charge $350 per day for days 1 through 7. A three-day stay would cost $1,050 instead of the $1,736 deductible under Original Medicare. But a seven-day stay would cost $2,450, which is more than the Original Medicare deductible.

The benefit-period concept still exists within some Advantage plans, but the financial exposure is capped differently. All Medicare Advantage plans are required to have a maximum out-of-pocket (MOOP) limit, which Original Medicare does not have. Once you hit that cap in a plan year, the plan covers 100% of covered services for the rest of the year.

This is the trade-off agents frequently describe: Original Medicare has no annual out-of-pocket limit, but its benefit-period structure means your 90 days renew once you are out for 60 days. Medicare Advantage caps your total annual spending but follows plan-year rules. The right choice depends on how frequently someone is hospitalized and what other coverage they carry.

Part A Inpatient Hospital deductible $1,676 but if I have Part C Advantage Plan, the hospital $350 copay per day 1-7 so how does this work?

Many of the details of how Parts A and B operate by themselves become irrelevant once you enroll into an actual Medicare plan through a carrier.In this example, it is exactly that, you would owe a copay of $350 for each day you were admitted into the hospital as an inpatient, up to a maximum of 7 days. So if you were hospitalized for 12 days, your inpatient hospitalization bill would be $2,450 ($350 x 7 day cap).

What is less known is that if you leave the hospital and return within 60 days, this benefit does not restart because you are in the same "benefit period". So if you were in the hospital for 12 days, discharged for 45 days and then hospitalized for another 12 days, the inpatient hospitalization bill would still be $2,450 ($350 x 7 day cap).

Inpatient hospitalization on a Medicare Advantage plan is one of the larger bills you can receive. This is why I will often quote clients a type of ancillary policy called a Hospital Indemnity plan along with Medicare Advantage plan options which can reimburse inpatient hospitalization copays to fill this gap in coverage.

The Part A Deductible Can Hit More Than Once a Year

Because the Part A deductible is tied to benefit periods rather than calendar years, it is possible to pay it multiple times in a single year. Agents frequently flag this as one of the most misunderstood cost mechanics of Original Medicare.

Here is how it works: if you are hospitalized in February, pay the $1,736 deductible, recover, stay out of the hospital for at least 60 consecutive days, and then are hospitalized again in July, you pay the deductible a second time. In a worst-case scenario with repeated hospitalizations separated by at least 60-day gaps, one agent noted a beneficiary could theoretically face the Part A deductible up to six times in a single year.

Compare that to the Part B deductible ($283 in 2026), which is a true annual deductible that resets once on January 1. The difference between these two systems catches people off guard every year.

Is Medicare Part A enough for hospital coverage?

Having "enough" coverage is 100% subjective. Every person is different: different resources, different health situations, different needs, etc. I am going to highlight the facts of how Part A works--then you can decide if that is enough coverage for your needs.Part A has a deductible of $1,736 if you're admitted to the hospital. That isn't an annual deductible like most people are used to. It works on a 60-day benefit period--meaning if you are hospitalized in the spring, meet your deductible, and are re-admitted in the fall (or possibly summer), you will pay that deductible again. That means in the absolute worst-case scenario, you could be billed that deductible up to six times in a year. If your hospital stay is continuous past 60 days, you start to accrue copays over $400 per day. This is not including Skilled Nursing costs, if those may arise as well.

Part A is generally free monthly if you or your spouse have 40 quarters (10 years) working, paying FICA taxes. It seems unusual that one would pay for Part B, but not enroll in premium-free Part A. Original Medicare has no annual maximum out of pocket. There's no cap on the amount of medical bills you can receive. If the Medicare premiums are unaffordable, work with your local Social Security office to file an appeal. I would never recommend someone have Parts A and/or B by themselves. There are plenty of options to protect you from exhausting your retirement funds on medical expenses!

What the Part B Deductible Reset Actually Means

When agents are asked "why did my Medicare deductible reset in January," they are almost always talking about the Part B deductible. That one genuinely does reset on January 1, like most health insurance deductibles. Once you meet the $283 annual threshold, Medicare pays 80% of approved Part B services for the rest of the year. On January 1, it starts over.

The Part A system works on a completely different schedule. Agents describe it as a "per occurrence" or "per benefit period" deductible rather than an annual one. Both deductible amounts tend to increase slightly each year based on healthcare cost trends, and CMS announces the new figures each fall. But the fundamental structure (when you pay them) is different between Part A and Part B.

How Medigap Changes the Math

For beneficiaries on Original Medicare with a Medigap (Medicare Supplement) plan, much of this benefit-period anxiety disappears. Agents overwhelmingly describe Medigap as the solution to the financial exposure of Original Medicare's hospital cost structure.

A Plan G supplement covers the Part A deductible, the daily coinsurance for days 61 through 90, and the coinsurance on lifetime reserve days. Standardized Medigap plans generally include Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are used, though exact availability and rules can vary in Massachusetts, Minnesota, and Wisconsin. With a Plan G in place, the benefit-period structure still exists (it is built into Medicare itself), but the financial impact of bouncing between benefit periods is drastically reduced.

The trade-off is the monthly premium. Medigap premiums vary by state, age, and insurer, and they tend to increase over time. But agents consistently point out that the premium math usually favors the supplement for anyone who expects even one significant hospitalization.

What You Should Do With This Information

If you are on Original Medicare, the benefit-period system means your hospital coverage is not as simple as "90 days a year." It is 90 days per benefit period, with the period defined by when you go in and how long you stay out. Your Part A deductible can repeat multiple times in a year. And your 60 lifetime reserve days are a finite resource that never comes back.

If you are on Medicare Advantage, your costs are governed by your plan's Evidence of Coverage, not Original Medicare's standard Part A deductible schedule. Many Medicare Advantage costs and maximum out-of-pocket limits are tracked by plan year, but inpatient hospital copays can vary by plan. Some plans may still use per-admission or benefit-period-style rules, so you should check your plan documents before assuming a January 1 reset applies to hospital stays.

Either way, the answer to "do my hospital days reset every January?" is more nuanced than a simple yes or no. Understanding which system you are in, and how the 60-day clock works, is the difference between being financially prepared and being caught off guard.

Frequently Asked Questions

Do Medicare hospital days reset every year?

No. Under Original Medicare, hospital days reset by benefit period, not by calendar year.

How long is a Medicare Part A benefit period?

It starts when you are admitted as an inpatient and ends after 60 days in a row without inpatient hospital care or skilled SNF care.

Can you pay the Medicare Part A deductible more than once in a year?

Yes. A new benefit period can trigger another Part A deductible.

Do lifetime reserve days reset?

No. You get 60 lifetime reserve days total.

A local Medicare agent can walk you through how your specific coverage handles hospital stays, including whether a supplement or Advantage plan better fits your situation.