Medicare Part A Explained: What It Covers, What It Costs, and How to Enroll

-

March 15, 2026

Medicare Part A is the foundation of your Medicare coverage. Often called "hospital insurance," Part A covers inpatient care, skilled nursing, hospice, and some home health services. Most people qualify for Part A at no monthly premium, but that doesn't mean there are no costs involved.

Whether you're approaching 65, helping a parent navigate Medicare, or just trying to understand how the pieces fit together, this guide breaks down everything you need to know about Part A: what it covers, what it costs, how to enroll, and the mistakes that can cost you money down the road.

What Does Medicare Part A Cover?

Part A covers medically necessary care that involves an inpatient stay or admission. Here's how it breaks down:

Inpatient Hospital Care

This is the core of Part A. When you're admitted to a hospital as an inpatient, Part A helps cover:

- A semi-private room and meals

- Nursing care and monitoring

- Medications administered during your stay

- Lab tests, imaging, and diagnostic services

- Surgeries and procedures performed during admission

- Mental health care provided on an inpatient basis

Important distinction: If you're at the hospital but classified as under "observation status" rather than formally admitted, you're technically an outpatient, and that care falls under Medicare Part B instead. This matters more than most people realize, especially when it comes to what happens after your hospital stay.

Skilled Nursing Facility (SNF) Care

After a qualifying inpatient hospital stay of at least 3 consecutive days, Part A covers care in a skilled nursing facility:

- Days 1–20: Covered in full (no coinsurance)

- Days 21–100: Covered with a daily coinsurance amount ($204.50/day in 2025)

- After day 100: You pay all costs

This is not the same as long-term custodial care (like a nursing home for daily living assistance). Part A only covers skilled care that requires licensed professionals: things like physical therapy after a hip replacement or wound care after surgery.

Hospice Care

Part A covers hospice care for terminally ill beneficiaries who choose comfort-focused care over curative treatment. This includes:

- Medical care and pain management

- Nursing visits

- Medical equipment and supplies

- Counseling, both for the patient and family members

- Short-term respite care for caregivers

- Medications related to the terminal diagnosis

Hospice benefits have no time limit as long as the hospice medical director recertifies the illness. Most hospice services have no cost to the beneficiary.

Home Health Services

Part A covers certain home health services when all of these conditions are met:

- A doctor certifies that you need skilled care at home

- You are homebound (leaving home requires considerable effort)

- The care is provided by a Medicare-certified home health agency

Covered home health services include skilled nursing, physical therapy, occupational therapy, speech therapy, and medical social services. Notably, home health care under Medicare has no coinsurance and no deductible.

What Part A Does NOT Cover

Understanding the gaps is just as important as knowing what's covered:

- Long-term custodial care: Assistance with daily activities (bathing, dressing, eating) in a nursing home or at home is not covered unless skilled care is also needed

- Private rooms: Unless medically necessary

- Personal comfort items: Television, phone, private-duty nursing

- Care outside the U.S.: With very limited exceptions

- Outpatient services: Doctor visits, lab work as an outpatient, and emergency room visits fall under Part B

Does Medicare Part A cover outpatient surgery, or is that strictly under Part B?

Medicare Part A: does not pay for outpatient surgery. Part A covers inpatient services to include inpatient hospital care up to 150 days and inpatient skilled nursing care for up to but no more than 100 days per stay. Part A has a modest deductible of $1676 for 2025, and is subject to per day coinsurance begining after day 60 of inpatient hospital care and day 20 of in-patient skilled nursing care. Medicare Part A does not pay for Long Term Care services.Medicare Part B: pays for outpatient surgery and all other Medicare appoved outpatient services like like Doctor Visits, Lab Work, Outpatient Surgery, Physical Therapy, etc. Part B has a monthly cost to obtain coverage. The cost in 2025 for most Americans is $185 per month. If your Adjustable Gross Income (AGI) is higher than most, the premium for Part B is higher.

How Much Does Medicare Part A Cost?

Most people think Part A is "free," and for many, the premium is. But there are still costs to be aware of.

Monthly Premium

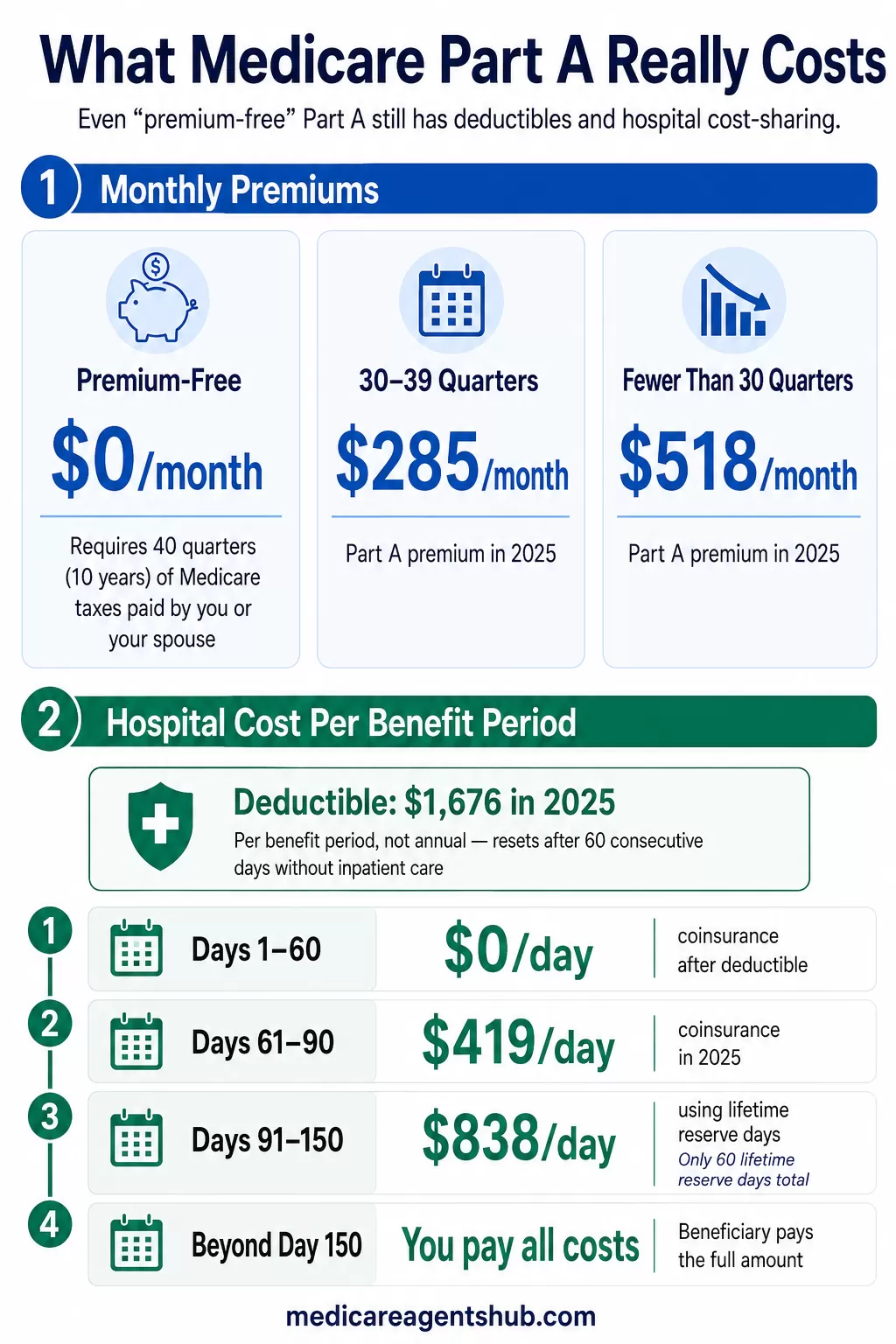

If you or your spouse paid Medicare taxes for at least 40 quarters (10 years), you qualify for premium-free Part A. This applies to the vast majority of beneficiaries.

If you don't meet that threshold:

- 30–39 quarters: $285/month in 2025

- Fewer than 30 quarters: $518/month in 2025

Deductible

Part A has a per-benefit-period deductible, not an annual deductible. In 2025, this is $1,676. Each time you're admitted to the hospital after a benefit period ends (60 consecutive days without inpatient care), the deductible resets.

This means you could potentially pay the Part A deductible multiple times in a single year if you have separate hospital stays.

Coinsurance for Extended Stays

- Days 1–60: $0 coinsurance (after the deductible)

- Days 61–90: $419/day coinsurance in 2025

- Days 91–150 (lifetime reserve days): $838/day — and you only get 60 of these in your lifetime

- Beyond 150 days: You pay all costs

These out-of-pocket costs are exactly why many beneficiaries pair Original Medicare with a Medicare Supplement (Medigap) plan; most Medigap plans cover the Part A deductible and coinsurance in full.

Who Is Eligible for Medicare Part A?

You're eligible for Part A if you meet any of these criteria:

- Age 65 or older and you or your spouse paid Medicare taxes for at least 10 years

- Under 65 with a qualifying disability, after receiving Social Security Disability Insurance (SSDI) for 24 months

- Any age with End-Stage Renal Disease (ESRD), permanent kidney failure requiring dialysis or a transplant

- Any age with ALS (Lou Gehrig's disease), eligible from the first month of SSDI benefits

How to Enroll in Part A

Automatic Enrollment

If you're already receiving Social Security benefits when you turn 65, you'll be automatically enrolled in Part A (and Part B). Your Medicare card will arrive in the mail about three months before your 65th birthday.

Manual Enrollment

If you're not yet receiving Social Security, you'll need to sign up during your Initial Enrollment Period (IEP), the 7-month window that starts 3 months before your 65th birthday month and ends 3 months after.

You can enroll through:

- The Social Security Administration website (ssa.gov)

- Your local Social Security office

- By phone at 1-800-772-1213

If you're still working and covered by an employer plan, you may be able to delay enrollment without penalty. But the rules around this are specific. Our article on whether you need Medicare if you're still working past 65 explains when delaying makes sense and when it doesn't.

Part A Late Enrollment Penalty

If you don't qualify for premium-free Part A and you don't enroll when first eligible, you may face a late enrollment penalty. The penalty is 10% added to your Part A premium, and you'll pay it for twice the number of years you were eligible but didn't enroll.

For those who qualify for premium-free Part A, there is no penalty; you can enroll anytime after age 65 without consequences, since there's no premium to penalize.

How Part A Fits Into the Bigger Medicare Picture

Medicare has four parts, and understanding how they work together is key:

- Part A (Hospital Insurance): Inpatient care, skilled nursing, hospice, home health

- Part B (Medical Insurance): Doctor visits, outpatient care, preventive services, durable medical equipment

- Part C (Medicare Advantage): An alternative to Original Medicare that bundles Parts A and B (and usually Part D) through a private insurer

- Part D (Prescription Drug Coverage): Standalone drug plans for those on Original Medicare

Parts A and B together make up "Original Medicare." Most beneficiaries either stick with Original Medicare and add a Medigap plan plus Part D, or they choose a Medicare Advantage plan that wraps everything into one.

Common Part A Questions

Does Part A cover emergency room visits?

Not directly. Emergency room services are covered under Part B. However, if you're admitted to the hospital through the ER, your inpatient stay is covered under Part A.

Does Part A cover ambulance services?

Ambulance services are covered under Part B, not Part A, even if the ambulance takes you to a hospital where you're admitted as an inpatient.

Can I have Part A without Part B?

Yes. Since most people get Part A premium-free, some choose to enroll in Part A only and delay Part B, especially if they're still covered by an employer plan. Just be aware of Part B late enrollment penalties if you delay without qualifying coverage.

What's a "benefit period" under Part A?

A benefit period begins the day you're admitted as a hospital inpatient and ends when you've gone 60 consecutive days without inpatient hospital or skilled nursing care. Once a new benefit period starts, the Part A deductible applies again.

The Bottom Line

Medicare Part A provides essential hospital coverage that most Americans qualify for at no monthly premium. It’s the insurance vehicle you paid into throughout your working years, and it delivers real value for short-term hospitalization, skilled nursing, and hospice. But between the per-stay deductible, coinsurance for longer stays, and the limits on skilled nursing and hospice, Part A alone doesn't cover everything. Understanding exactly what it does — and doesn't — pay for puts you in a much stronger position to plan your coverage and avoid surprises.

If you're unsure how Part A fits into your overall Medicare strategy, an independent Medicare agent can help you evaluate your options and build a plan that covers your actual needs, not just the basics.