Palliative Care vs. Hospice: The Medicare Pivot Families Don't See Until It's Too Late

-

June 11, 2026

Families facing a serious illness often hear two terms used almost interchangeably: palliative care and hospice. The assumption is that they're roughly the same thing, covered the same way, with the same paperwork. They're not. Medicare treats them as fundamentally different benefits, billed under different parts of the program, with different eligibility rules and potentially very different out-of-pocket costs. The pivot from one to the other can happen in a single conversation with a doctor, and most families don't understand what just changed until the bills arrive.

Two Types of Comfort Care, Two Very Different Coverage Rules

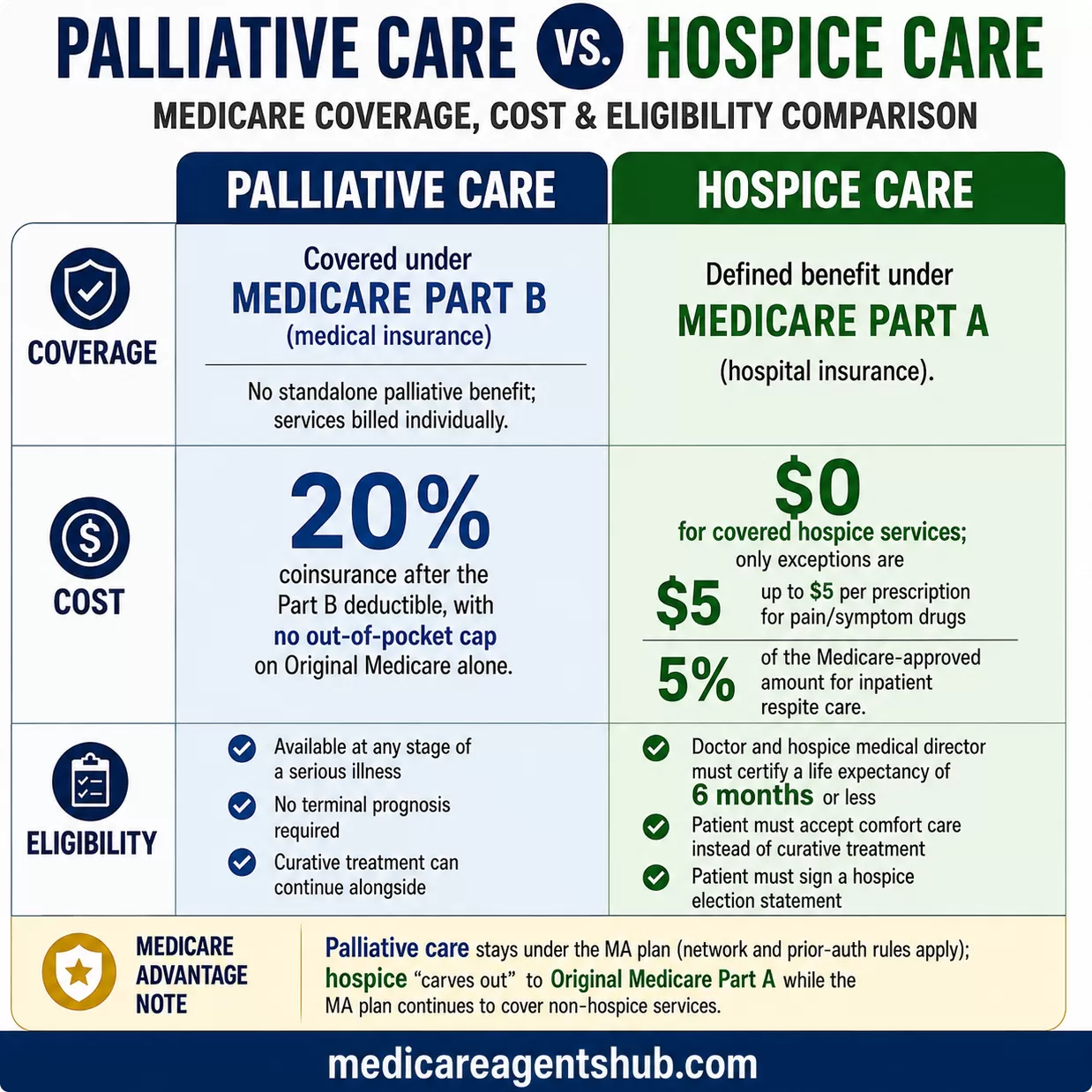

The first thing agents want families to understand is that palliative care and hospice care are not covered under the same part of Medicare. This single fact drives most of the confusion.

Many of the services that make up palliative care may be covered under Medicare Part B (medical insurance) when they are medically necessary. There is no standalone "palliative care benefit" in Medicare. Instead, palliative services like pain management, symptom control, and care coordination are billed as individual Part B services when provided by doctors, nurse practitioners, or specialists. Coverage can vary depending on the specific service, the care setting, the provider, and the patient's plan rules. If those services are provided during an inpatient hospital stay, they may fall under Part A instead. That means beneficiaries on Part B typically pay the standard cost-sharing: 20% coinsurance after meeting the annual Part B deductible.

Hospice care, by contrast, is a defined benefit under Medicare Part A (hospital insurance). Once a patient elects hospice, Part A covers nearly all costs related to the terminal condition, including medications, medical equipment, nursing, counseling, and respite care for family caregivers. The patient typically pays nothing for covered hospice services, with limited exceptions for prescription drug copays and inpatient respite care.

How does Medicare cover palliative care for serious illnesses, and what’s the difference between palliative care and hospice care?

Medicare does not have a specific “palliative care benefit” the way it does for hospice.Instead, palliative care is usually billed under Part B (medical insurance) when provided by doctors, nurse practitioners, or specialists.

This means beneficiaries typically pay 20% coinsurance (after the Part B deductible).

If palliative care services are provided during a hospital stay, they are covered under Part A (hospital insurance).

Coverage may include visits with palliative care specialists, counseling, symptom management (like pain or shortness of breath), and care coordination.

Palliative Care is essential and can be provided at any stage of a serious illness—not just at the end of life. It is designed to effectively relieve symptoms, manage stress, and significantly improve the quality of life, even while patients continue to receive curative treatments. There are no time limits; patients have the right to receive palliative care alongside standard medical care.

Hospice Care is a defined benefit covered under Medicare Part A. It specifically serves patients with a terminal illness who have a life expectancy of six months or less, assuming the disease progresses as expected. In hospice care, the focus decisively shifts from curing the illness to delivering comfort and support. This care includes necessary medications, equipment, and support services related to the terminal condition, usually at no cost to the patient.

That coverage gap between 20% coinsurance and $0 is significant. A family managing a loved one's serious illness under palliative care could see Part B cost-sharing add up considerably over months of treatment, especially without a supplemental plan. The moment that same patient transitions to hospice, most of those costs disappear.

Who Qualifies: Any Serious Illness vs. Terminal Diagnosis

The eligibility rules for each path are just as different as the billing.

Palliative care does not require the same terminal prognosis that hospice does. A patient can receive palliative services at any stage of a serious illness, whether that illness is newly diagnosed or has been managed for years, and there is no requirement to stop pursuing curative treatment. That said, each individual service still needs to meet Medicare's medical-necessity and plan-coverage rules. A patient undergoing chemotherapy, for example, can receive palliative care for pain and nausea management at the same time. There are no time limits.

Hospice care requires three things:

- A doctor and the hospice medical director must certify that the patient is terminally ill with a life expectancy of six months or less, assuming the disease runs its normal course.

- The patient must accept comfort care instead of curative treatment for the terminal condition.

- The patient must sign a hospice election statement choosing hospice care.

If I need hospice care in the future, can my Medicare plan cover it?

Hospice care is usually covered by your Part A of Original Medicare(your red, white and blue Medicare card).You qualify for hospice care if you meet all these conditions:

Your hospice doctor and your regular doctor (if you have one) certify that you’re terminally ill (with a life expectancy of 6 months or less).

You accept comfort care (palliative care) instead of care to cure your illness.

You sign a statement choosing hospice care instead of other Medicare-covered treatments for your terminal illness and related conditions.

That second requirement is where families struggle most. Electing hospice means agreeing to stop curative treatment for the terminal illness. Medicare will still cover treatment for conditions unrelated to the terminal diagnosis, but the shift from "fighting it" to "managing comfort" is an enormous emotional and medical pivot. Many families delay this decision, sometimes at real financial cost, because they aren't ready to stop treatment.

The Cost Difference Families Miss

When a patient is receiving palliative care under Part B, the family is responsible for the 20% coinsurance on every covered service. Doctor visits, specialist consultations, pain management procedures, symptom control medications administered in office settings, counseling sessions: all billed at 80/20 after the deductible. If the patient has a Medicare Supplement plan, that plan may cover some or all of the 20%. If the patient is on Original Medicare alone, that 20% has no cap.

Once hospice is elected, Part A takes over. The hospice benefit covers medications for pain and symptom management, durable medical equipment like hospital beds and oxygen, nursing visits, hospice aide services, physical and occupational therapy, social work services, grief counseling for the family, and up to five days of inpatient respite care so caregivers can take a break. The only patient costs are small copayments for prescription drugs (no more than $5 per prescription) and 5% of the Medicare-approved amount for inpatient respite care.

How does Medicare cover palliative care for serious illnesses, and what’s the difference between palliative care and hospice care?

Hospice comes under Medicare Part A, regardless of whether a person is on original Medicare, or an Advantage plan. In both cases, Hospice is free. It's typically offered when end-of-life is determined to be less than 6 months by the PCP. The service varies according to the needs of the person. Palliative care is not free, but follows the co-pays or co-insurance of their plan.The Medicare Advantage Wrinkle: Hospice Carves Out, Palliative Doesn't

For families whose loved one is enrolled in a Medicare Advantage plan, there's an additional layer of complexity that agents say catches people off guard.

When a Medicare Advantage enrollee elects hospice, coverage for hospice-related services shifts to Original Medicare Part A. This is called the hospice carve-out. The patient stays enrolled in their Advantage plan, and the plan continues to cover non-hospice services like dental, vision, hearing, and prescription drugs. But all hospice care is billed directly through Original Medicare.

Palliative care, on the other hand, stays under the Medicare Advantage plan. That means the plan's network rules, prior authorization requirements, and cost-sharing structure all apply. If a patient's palliative care specialist is out of network on an HMO plan, the plan may not cover those visits at all. If the plan requires prior authorization for certain pain management procedures, the family has to navigate that process while managing a serious illness.

If I need hospice care in the future, can my Medicare plan cover it?

Yes. Hospice care is covered by Medicare, no matter what type of Medicare plan you have.If you have Original Medicare (Parts A & B) hospice is covered under Part A when your doctor and the hospice medical director certify that you’re terminally ill with a life expectancy of six months or less.

If you have a Medicare Advantage (Part C) plan, hospice care is still covered by Original Medicare, not by your Advantage plan. You’ll continue to get your hospice services through Medicare Part A, and your plan will still cover other non-hospice benefits (like dental, vision, or prescription drugs, depending on your plan).

This difference matters for provider access. Under hospice, the patient can see any Medicare-certified hospice provider regardless of their Advantage plan's network. Under palliative care, they're bound by whatever network and authorization rules their plan imposes.

"Medicare Does Not Cover Palliative Care" and Why That's Wrong

One point of confusion that appears even among some agents: the claim that Medicare does not cover palliative care at all. This is incorrect, and families who hear it may delay or avoid palliative services they're entitled to.

The confusion comes from the fact that Medicare does not have a dedicated "palliative care benefit" the way it has a defined hospice benefit. There is no box to check, no election form to sign, no single billing code called "palliative care." Instead, the individual services that make up palliative care, such as specialist visits, pain management, counseling, and care coordination, are each covered under Part B as medically necessary services.

Saying "Medicare doesn't cover palliative care" conflates "no dedicated benefit" with "no coverage." The practical difference for families is significant: if you hear this from any source, push back. Your loved one's palliative care services are billable under Part B, and Medicare will pay 80% of the approved amount after the deductible.

What Signing the Hospice Election Actually Means

The hospice election is not a one-way door. A patient can revoke hospice at any time and return to curative treatment under their regular Medicare coverage. If they later decide to re-elect hospice, they can do so. But while hospice is in effect, Medicare will not pay for curative treatments related to the terminal condition.

Agents consistently emphasize that families should understand what continues to be covered during hospice. Medicare still pays for:

- Treatment of conditions unrelated to the terminal diagnosis

- Regular doctor visits for non-hospice medical needs

- Emergency care for conditions not related to the terminal illness

What Medicare does not cover during hospice:

- Curative treatment aimed at the terminal condition

- Care from a hospice provider that wasn't set up by the hospice medical team

- Room and board in a nursing home or residential facility (unless short-term inpatient or respite care)

If I need hospice care in the future, can my Medicare plan cover it?

If using a hospital for your hospice, it must be due to a terminal illness and a determination that your life span is less than 6 months. You are not expecting curative treatments, but comfort and ease through a life-ending transition.Otherwise, for Home hospice treatment, it would cover things like pain management, through nursing and skilled care, medications, spiritual care, etc. Even Bereavement counseling. But once you step back to a Curative type treatment the hospice coverage stops, and standard medical fees and service rates would apply. There is no Long-Term Care, or any services non related to the hospice care that would be covered.

When Palliative Care Is the Right Call

Not every serious illness leads to hospice. Palliative care can run for months or years alongside active treatment, and for many patients it's the right path. Agents point to several situations where palliative care is the better fit:

- The patient is still pursuing curative treatment and wants symptom relief alongside it

- The prognosis is uncertain or longer than six months

- The patient isn't ready to stop treatment but needs help managing pain, nausea, fatigue, or emotional distress

- The family needs care coordination support while the patient is still actively being treated

For families caring for a loved one with a chronic condition like advanced heart failure, COPD, or dementia, palliative care can bridge the gap between standard medical treatment and the eventual hospice conversation. That bridge might last weeks or years, and during that entire time, Part B covers the services with standard cost-sharing.

Caregivers themselves may also need support. Medicare Part B covers mental health services, including therapy and counseling, for beneficiaries experiencing stress, anxiety, or depression. And if the patient is already on hospice, the hospice benefit includes up to five days of respite care so the primary caregiver can take a break.

The Conversation to Have Before the Crisis

The worst time to learn about the palliative-to-hospice pivot is in the middle of it. Agents consistently advise families to have this conversation early, while there's still time to understand the options, compare costs, and make decisions without the pressure of an imminent transition.

Key questions to ask your doctor or care team:

- Is my loved one receiving palliative care, hospice care, or neither? What's being billed and under which part of Medicare?

- If we're on palliative care now, what would trigger a hospice conversation?

- If we have a Medicare Advantage plan, which providers can we see under each path?

- What happens to our current medications and equipment if we elect hospice?

A licensed Medicare agent can help families understand how their specific plan handles both palliative and hospice coverage, what the out-of-pocket exposure looks like under each path, and when it makes sense to start planning for the transition.

Official Medicare Sources

This article is informed by licensed Medicare agent expertise and official CMS guidance. For the most current coverage details, refer to these primary sources:

- Hospice care coverage: Medicare.gov - Hospice Care (covers eligibility, costs, and what's included under Part A)

- Medicare Part B coverage: Medicare.gov - What Part B Covers (the basis for palliative service coverage)

- Medicare Advantage and hospice: CMS - Value-Based Insurance Design Model (background on the MA hospice carve-out and the VBID hospice test that ended December 31, 2024)

Frequently Asked Questions

Does Medicare cover palliative care?

Medicare does not have a dedicated palliative care benefit, but many of the services that make up palliative care are covered under Part B as medically necessary outpatient services. These include pain management, symptom control, specialist visits, and care coordination. Patients pay the standard 20% coinsurance after meeting the Part B deductible.

Is hospice always free under Medicare?

Nearly. Once a patient elects hospice, Medicare Part A covers almost all costs related to the terminal condition. The only patient costs are small copayments: up to $5 per prescription for pain and symptom management medications, and 5% of the Medicare-approved amount for inpatient respite care.

Can you leave hospice and go back to treatment?

Yes. A patient can revoke their hospice election at any time and return to curative treatment under their regular Medicare coverage. If they later decide to re-elect hospice, they can do so.

What happens to Medicare Advantage when hospice starts?

When a Medicare Advantage enrollee elects hospice, coverage for hospice-related services shifts to Original Medicare Part A. The patient stays enrolled in their Advantage plan, which continues to cover non-hospice services like dental, vision, hearing, and prescription drugs. All hospice care is billed through Original Medicare.