What Happens to Your Medicare Advantage Plan When You Enter Hospice

-

June 6, 2026

A family member just received a terminal diagnosis. You're trying to arrange hospice care, and somewhere in that fog of paperwork and phone calls, someone mentions that their Medicare Advantage plan won't actually be handling the hospice benefits. That can't be right, can it? They've been on this plan for years.

It is right. And almost nobody on Medicare Advantage knows about it until they're in the middle of a crisis.

When a Medicare Advantage enrollee elects hospice care, their hospice benefits don't come from the Advantage plan. They shift back to Original Medicare Part A. This is called the hospice carve-out, and understanding how it works can save families real confusion during one of the hardest moments they'll face. For a personal perspective on this process, read one family's firsthand experience with hospice and Medicare.

How the Hospice Carve-Out Works

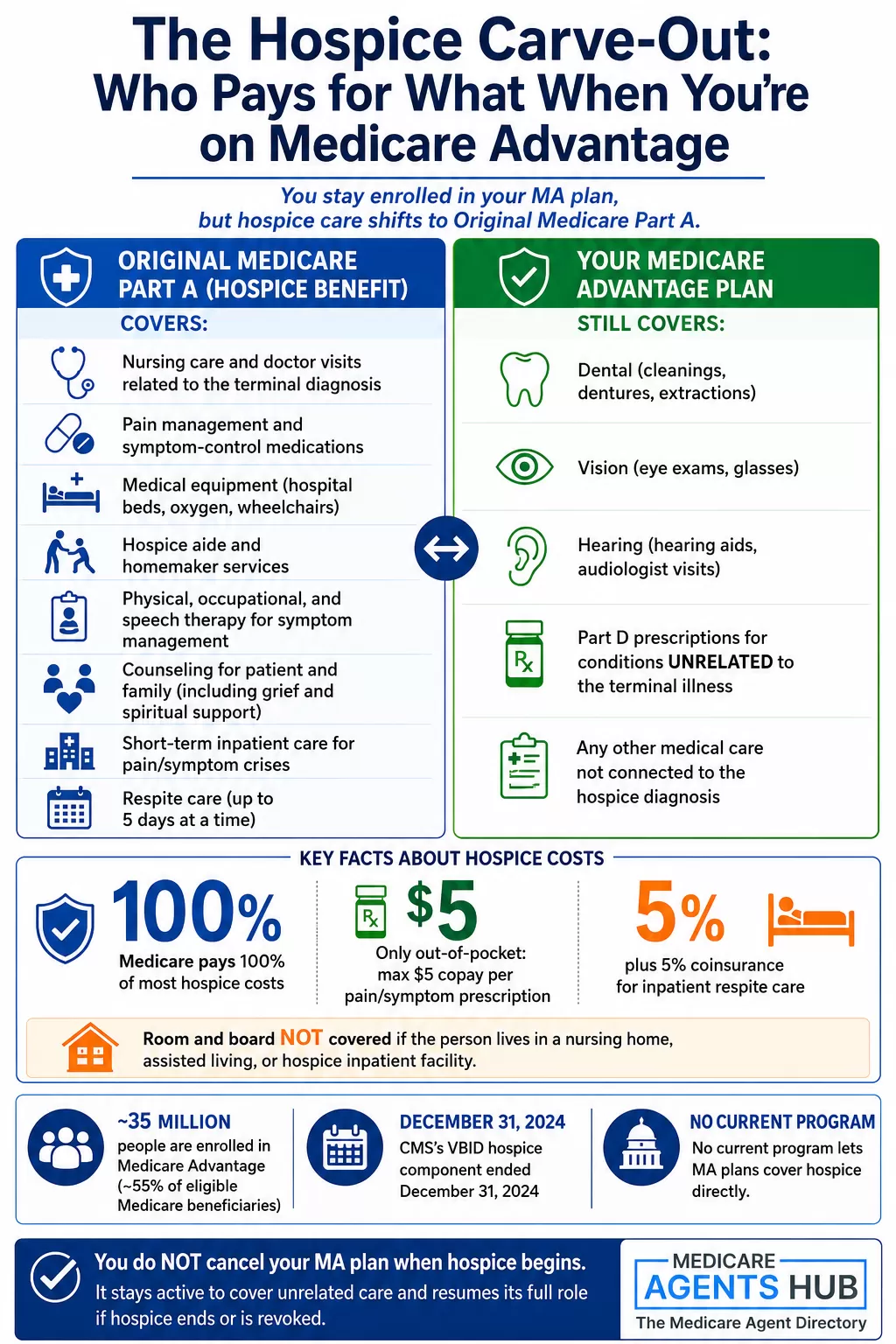

Medicare Advantage plans (Part C) bundle your Part A and Part B benefits into a single plan, usually with extras like dental and vision. But under current Medicare rules, hospice is carved out of the MA plan and paid through Original Medicare Part A.

CMS previously tested including hospice coverage in certain MA plans through the Value-Based Insurance Design (VBID) model, but that hospice component ended December 31, 2024. Standard carve-out rules now apply universally to all MA plans, and no current program allows MA plans to cover hospice services directly.

You don't leave your Medicare Advantage plan. You stay enrolled. But for everything related to your terminal illness, Original Medicare takes over. Your MA plan steps aside for those services specifically.

This happens automatically when you elect hospice. There's no separate enrollment form for Original Medicare, no switching plans. The billing just routes differently behind the scenes.

If I need hospice care in the future, can my Medicare plan cover it?

Yes — and this is really important to understand.Hospice care is always covered under Original Medicare (Part A), no matter what type of Medicare plan you have.

Even if you’re enrolled in a Medicare Advantage plan (Part C), hospice benefits “carve out” to Original Medicare. That means:

Part A covers hospice directly (not the Medicare Advantage plan).

You can still stay in your Medicare Advantage plan for non-hospice care (like regular doctor visits or prescriptions), but hospice services are billed through Original Medicare.

Hospice includes things like pain management, counseling, medical equipment, and respite care for family caregivers.

Tip: Sometimes people assume their Advantage plan “handles everything,” but hospice is an exception. If that time comes, make sure your providers know you’re electing hospice under Original Medicare so claims go through correctly.

What Original Medicare Covers During Hospice

Once the carve-out kicks in, Medicare Part A pays for all hospice-related services. That includes:

- Nursing care and doctor visits related to the terminal diagnosis

- Pain management and symptom control medications

- Medical equipment like hospital beds, oxygen, and wheelchairs

- Hospice aide and homemaker services

- Physical, occupational, and speech therapy for symptom management

- Counseling for the patient and family, including grief and spiritual support

- Short-term inpatient care for pain or symptom crises

- Respite care (up to 5 days at a time to give family caregivers a break)

Medicare pays 100% of most hospice costs. There are only two small exceptions: a copay of no more than $5 for each prescription for pain and symptom management, and 5% coinsurance for inpatient respite care. For the vast majority of families, hospice under Part A means essentially zero out-of-pocket cost for end-of-life care.

One important exception: room and board is generally not covered if the person lives in a nursing home, assisted living facility, or hospice inpatient facility. The hospice benefit covers short-term inpatient stays and respite care arranged by the hospice team, but ongoing room and board costs in a residential facility remain the patient's responsibility.

What Your Medicare Advantage Plan Still Covers

Even though hospice care moves to Original Medicare, you keep your Medicare Advantage plan. And it still covers everything that isn't related to the terminal illness or the hospice benefit.

That means your MA plan continues to handle:

- Dental benefits (routine cleanings, dentures, extractions). If you've been relying on your Advantage plan for dental coverage, that doesn't go away.

- Vision benefits (eye exams, glasses). This stays with your MA plan as well. For more details on what these benefits typically include, see our breakdown of Medicare vision coverage.

- Hearing benefits (hearing aids, audiologist visits)

- Part D prescription drug coverage for medications unrelated to the terminal illness

- Any other medical care not connected to the hospice diagnosis

So if your parent is in hospice for lung cancer but also needs a filling or new glasses, the Advantage plan handles that. If they break a wrist in a fall and the hospice team determines the care is unrelated to the terminal illness or related conditions, the MA plan would typically be the payer rather than the hospice benefit.

This dual-coverage setup is one of the reasons the carve-out confuses families. Two different payers are active at the same time, splitting responsibility based on whether the service relates to the terminal condition.

If I need hospice care in the future, can my Medicare plan cover it?

Yes, if you need hospice care in the future, Medicare will cover it, including if you're enrolled in a Medicare Advantage plan. Under federal law, hospice services are always covered by Original Medicare (Part A), even if you are currently enrolled in a Medicare Advantage (MAPD) plan. This means that when you elect the Medicare hospice benefit, your hospice care—including pain management, symptom control, nursing, and support services—will be coordinated through Medicare Part A, not your Medicare Advantage plan. However, your MAPD plan will still continue to cover services unrelated to your terminal condition, such as dental, vision, or other supplemental benefits. It's important to ensure your providers are Medicare-certified for hospice care. Hopefully you will never need it, but if you do, it is there through part AHave questions about how your specific MA plan handles hospice?

Find a Local Medicare Agent who can review your plan details and walk you through what to expect.

How This Differs from Medigap

If the person entering hospice has Original Medicare with a Medigap supplement instead of Medicare Advantage, the process is simpler. Original Medicare already handles their Part A benefits, so there's no carve-out. Part A covers the hospice services directly, and Medigap picks up any remaining cost-sharing (which is minimal for hospice anyway).

The carve-out only matters for Medicare Advantage enrollees because MA plans normally replace Original Medicare's role in paying claims. Hospice is the exception where that replacement doesn't apply.

This is actually one of the trade-offs that come with Medicare Advantage that rarely gets discussed during enrollment. It's not necessarily a disadvantage, since the hospice benefit itself is the same either way, but the billing mechanics are different and the transition can feel abrupt if families aren't prepared for it.

What Families Need to Do

When a loved one elects hospice, there are a few practical steps that can prevent billing headaches:

Make Sure Providers Know About the Coverage Split

The hospice agency will bill Original Medicare directly. But other providers (the dentist, the eye doctor, a specialist treating an unrelated condition) need to keep billing the Medicare Advantage plan. If a provider accidentally bills the wrong payer, claims get denied, and sorting it out takes time nobody has during this period.

Keep the Medicare Card Accessible

The red, white, and blue Original Medicare card (or the person's Medicare number) is what the hospice provider needs. Many people on Medicare Advantage haven't used their Original Medicare card in years. Find it. If it's lost, you can request a replacement through Medicare.gov or by calling 1-800-MEDICARE.

Understand the Medication Split

Medications for pain and symptom management related to the terminal illness are covered by the hospice benefit (through Part A). But prescriptions for other conditions still go through the MA plan's Part D coverage. The hospice team and the pharmacy need to be on the same page about which drugs fall under which coverage.

| Type of Medication | Covered By |

|---|---|

| Pain and symptom management for the terminal illness | Hospice benefit (Original Medicare Part A) |

| Unrelated conditions (e.g., blood pressure, cholesterol, diabetes) | MA plan's Part D drug coverage |

Don't Drop the Medicare Advantage Plan

Some families assume they should cancel the MA plan once hospice starts. Don't. The plan continues to cover non-hospice services, and dropping it would leave the person with gaps in coverage for anything unrelated to their terminal diagnosis. If the person later revokes hospice (which is their right at any time), the MA plan is still there to resume full coverage.

Hospice Carve-Out Checklist

- Keep the red, white, and blue Medicare card handy

- Confirm the hospice agency is Medicare-certified

- Ask the hospice team which medications are hospice-related vs. unrelated

- Tell non-hospice providers to keep billing the MA plan for unrelated care

- Do not cancel the MA plan without speaking to Medicare, the plan, SHIP, or a licensed agent

How does Medicare cover palliative care for serious illnesses, and what’s the difference between palliative care and hospice care?

Palliative care helps manage pain, symptoms, and stress while you continue treatments aimed at fighting the disease.Medicare covers it through standard benefits, like Part A for hospital care and Part B for outpatient services, so you can access this care at any stage of an illness with just the usual coinsurance.

Hospice care is for when a doctor believes someone is in the final months of life and has chosen to focus entirely on comfort rather than curative treatments.

Medicare provides a special hospice benefit under Part A that covers nearly all costs, including medications, equipment, and emotional support, often at little to no expense.

What Happens If Hospice Ends

Hospice isn't always permanent. It can end for several reasons: the patient may revoke their hospice election (which they can do at any time), they might decide to pursue curative treatment again, or the hospice medical director may determine the patient is no longer certifiable as terminally ill. Medicare hospice coverage continues beyond six months only if a doctor recertifies the terminal illness. When hospice ends for any of these reasons, the coverage shift reverses. Original Medicare stops handling their care, and the Medicare Advantage plan picks back up as the primary payer for all services.

This is another reason not to drop the MA plan. It's designed to remain active throughout the hospice period, ready to resume its normal role if the situation changes. If you're considering switching from Medicare Advantage back to Original Medicare for other reasons, that's a separate decision with its own enrollment rules and timing.

Why This Matters More Than People Think

About 35 million people are enrolled in Medicare Advantage plans, representing roughly 55% of all eligible Medicare beneficiaries. And when someone in that group faces a terminal illness, the coverage mechanics change in a way that almost none of them were told about at enrollment.

The carve-out itself isn't a problem. Original Medicare's hospice benefit is generous and covers nearly everything. The problem is the surprise. Families already dealing with an overwhelming situation shouldn't also have to figure out on the fly why their insurance suddenly works differently.

If you or a family member is on Medicare Advantage, knowing about the hospice carve-out now, before you need it, is one of the most practical things you can do. And if you're comparing Medicare Advantage and Medigap options, this is a factor worth weighing. A local Medicare agent can walk you through the differences and help you understand how your coverage would work if hospice ever became necessary.

Hospice eligibility and claims decisions depend on the patient's diagnosis, hospice election, plan rules, and provider billing. Families should confirm details with the hospice provider, Medicare (1-800-MEDICARE), the MA plan, or their state SHIP counseling program.

Frequently Asked Questions

Do I lose my Medicare Advantage plan when I elect hospice?

No. You stay enrolled in your MA plan. Hospice-related care shifts to Original Medicare Part A, but your MA plan continues covering dental, vision, hearing, and prescriptions for conditions unrelated to the terminal illness.

Who pays for prescriptions during hospice?

It depends on what the medication is for. Pain and symptom management drugs for the terminal illness fall under the hospice benefit (Part A). Prescriptions for unrelated conditions go through the MA plan's Part D coverage.

Can I leave hospice and go back to regular Medicare Advantage coverage?

Yes. You can revoke your hospice election at any time, or hospice may end if the doctor determines you no longer meet the terminal illness criteria. Either way, the MA plan resumes its normal role as the primary payer for all covered services.