Medicare Advantage vs. Medicare Supplement Plans: Which is Right for You?

-

Last Updated July 22, 2026

Deciding between Medicare Advantage and Medicare Supplement plans can be a challenge, especially with so many options and details to consider. Both plans offer unique benefits, and understanding the differences is key to choosing the right one for your healthcare needs. This guide will break down the features of each plan, helping you make a confident and informed choice about your Medicare coverage.

Understanding Original Medicare

Before diving into Medicare Advantage and Medicare Supplement plans, it’s crucial to understand the foundation: Original Medicare. Original Medicare consists of Part A (hospital insurance) and Part B (medical insurance). While it covers many healthcare services, it doesn’t cover everything. For instance, it doesn’t include most prescription drugs, dental, vision, or hearing care, and there are out-of-pocket costs such as deductibles, copayments, and coinsurance. Understanding what Original Medicare doesn’t cover is the first step toward deciding which supplemental coverage you need.

What is Medicare Advantage?

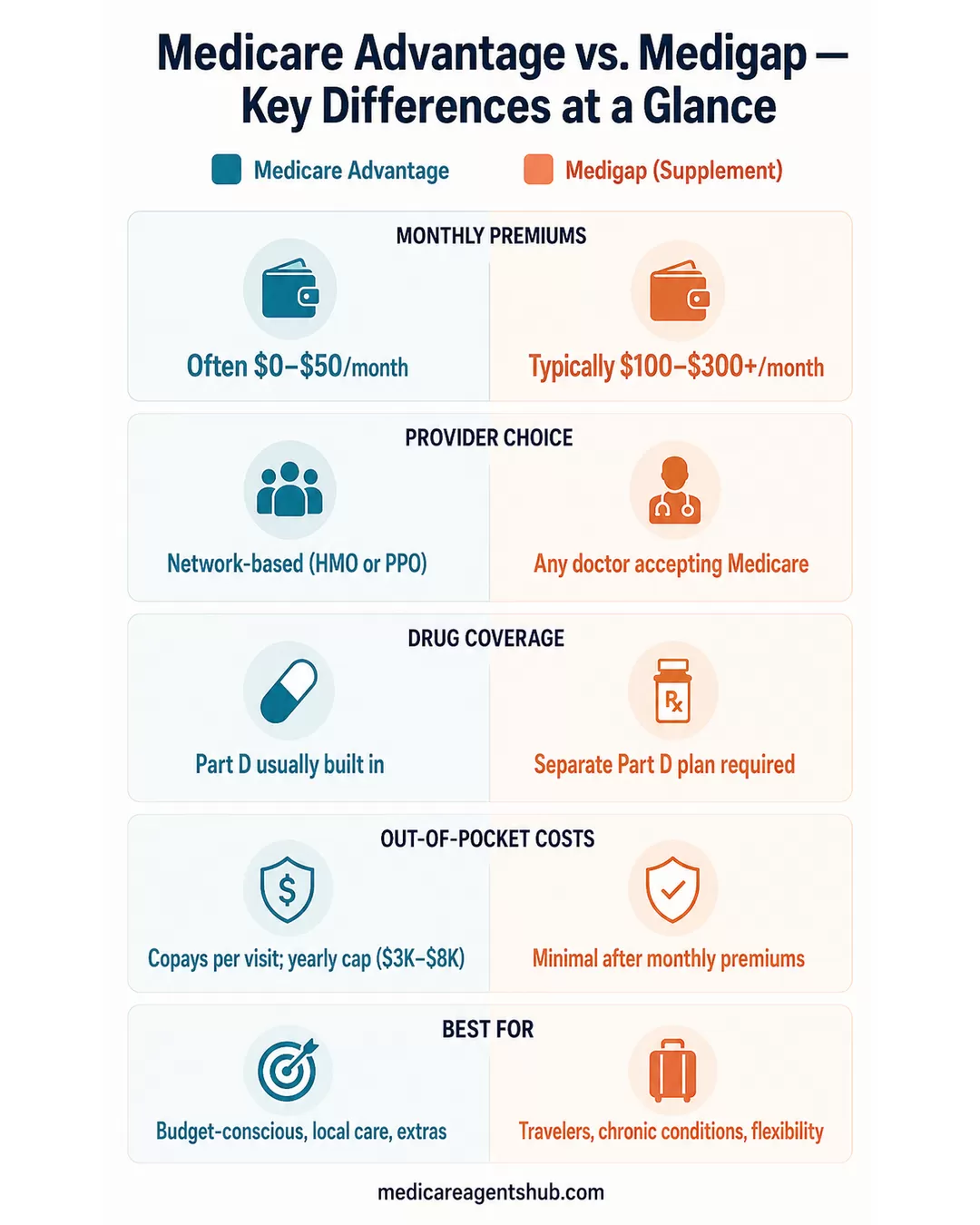

Medicare Advantage (MA), also known as Part C, is an alternative to Original Medicare offered by private insurance companies approved by Medicare. These plans bundle Part A, Part B, and often Part D (prescription drug coverage) into one plan. Many MA plans also provide additional benefits not covered by Original Medicare, such as dental, vision, hearing, and wellness programs.

Key Features of Medicare Advantage

- Comprehensive Coverage: Combines hospital, medical, and often prescription drug coverage, along with additional benefits.

- Network Restrictions: Typically operates within a network of doctors and hospitals. HMO plans require you to use network providers, while PPO plans offer more flexibility — though out-of-network costs can still be significant.

- Cost Structure: Often has lower monthly premiums than Medicare Supplement plans but includes out-of-pocket costs such as copayments and coinsurance. All plans have a yearly limit on out-of-pocket expenses (called the MOOP — Maximum Out-of-Pocket). Be sure to understand the trade-offs that come with Medicare Advantage before enrolling.

- Managed Care: These plans often involve managed care, meaning you might need referrals for specialists and prior authorization for certain services. This distinction matters especially if you manage a chronic condition like COPD.

What is a Medicare Supplement Plan?

Medicare Supplement plans, also known as Medigap, are designed to work alongside Original Medicare. These plans help cover some of the out-of-pocket costs associated with Original Medicare, such as copayments, coinsurance, and deductibles. Unlike Medicare Advantage, Medigap plans do not include prescription drug coverage, so beneficiaries typically need a separate Part D plan.

Key Features of Medicare Supplement Plans

- Standardized Benefits: Medigap plans are standardized across most states, meaning the benefits for each plan type (e.g., Plan G, Plan N) are the same regardless of the insurer. This makes it easier to compare pricing between companies.

- Flexibility in Providers: Allows you to see any doctor or specialist that accepts Medicare, offering nationwide coverage — a major advantage for snowbirds and frequent travelers.

- Predictable Costs: Higher monthly premiums compared to Medicare Advantage, but fewer out-of-pocket expenses. Beneficiaries can budget for healthcare more predictably.

- Supplemental Coverage: These plans only supplement Original Medicare, so you retain all the rights and protections of Original Medicare.

Is Original Medicare or Medicare Advantage better? Why do you recommend one over the other?

Original Medicare offers greater freedom in choosing providers, while Medicare Advantage often includes extra benefits like dental, vision, and fitness coverage, and may have lower out-of-pocket costs.Comparing Medicare Advantage and Medicare Supplement Plans

Coverage and Benefits

- Medicare Advantage: Offers all-in-one coverage, often including extra benefits like dental, vision, and hearing. These extras vary widely by plan — some cover only routine cleanings and eye exams, while others include more meaningful benefits for major dental work or hearing aids. Coverage is typically limited to a network, which can be restrictive if you travel frequently or live in multiple locations throughout the year.

- Medicare Supplement: Focuses on filling the gaps in Original Medicare, offering broader provider flexibility and nationwide coverage. Does not include additional benefits like dental or vision unless you purchase separate plans.

Cost of Medicare Advantage vs. Medigap

- Monthly Premiums: MA plans often $0–$50/month; Medigap plans typically $100–$300+/month depending on plan type, location, and age

- Deductibles: MA plans vary by plan; Medigap Plan G requires paying the Part B deductible ($283 in 2026), then covers nearly everything else

- Out-of-Pocket Maximum: MA plans cap yearly costs (often $3,000–$8,000); Original Medicare with Medigap has no cap but out-of-pocket costs are minimal after premiums

- Copays/Coinsurance: MA plans charge copays at each visit; Medigap Plans G and F cover the 20% Part B coinsurance completely, while Plan N leaves small copays for office and ER visits

The real question is whether you prefer to pay now (higher Medigap premiums) or pay later (MA copays as you receive care). If you’re generally healthy and rarely see doctors, a low-premium MA plan might save you money. If you have chronic conditions or anticipate frequent medical care, the predictability of Medigap can be worth the higher premiums.

What's your go-to strategy for helping someone decide between Medicare Advantage and Medigap?

When explaining the differences between the two, I like to say the Medigap is the "prepay" option and Medicare Advantage is the "pay as you go" option. If a client knows they are going to have some serious health issues and lots of medical care, i would recommend the Medigap route. However if they are pretty healthy and especially if they are looking to save money, I usually recommend Medicare Advantage, so they can "pay as they go" instead of paying up front whether or not they need it.Provider Flexibility

- Medicare Advantage: Requires you to use a network of providers, which can be limiting if you prefer a wide choice of doctors or travel often. HMOs are more restrictive; PPOs offer some out-of-network coverage at a higher cost.

- Medicare Supplement: Offers the freedom to use any provider that accepts Medicare, providing flexibility and peace of mind, especially for those who split their time between different locations.

What's the key difference in how Medicare Advantage and Medigap handle out-of-network providers?

The key difference between Medicare Advantage and Medigap policies is that Advantage plans only pay for in-network providers, while a Medigap plan will allow you to see any doctor, specialist, or hospital that accepts Medicare.Prescription Drug Coverage

- Medicare Advantage: Most MA plans include Part D prescription drug coverage built in. This simplifies things — one card, one plan, one premium.

- Medicare Supplement: Does not include drug coverage. You’ll need to enroll in a standalone Part D plan separately, which means managing an additional premium and formulary. Skip Part D when you’re first eligible without other creditable drug coverage and you’ll face a lifetime late enrollment penalty added to your premium.

Long-Term Considerations

- Medicare Advantage: Plans change every year — networks, formularies, copays, and even plan availability can shift. You should review your plan annually to make sure it still meets your needs. Stay current with the latest Medicare Advantage trends and changes.

- Medicare Supplement: Benefits are locked in by plan type and don’t change, but premiums can increase over time. Switching Medigap plans later in life can be difficult because most states allow medical underwriting after your initial open enrollment period.

Who Should Choose Medicare Advantage?

A Medicare Advantage plan may be the right fit if you:

- Want an all-in-one plan with medical, drug, and extra benefits bundled together

- Are comfortable using a network of local doctors and hospitals

- Prefer lower monthly premiums and can handle copays as you receive care

- Don’t travel extensively or split time between states

- Want extras like dental, vision, hearing, and fitness programs included

Do Medicare Advantage plans include dental coverage?

Yes. Most Medicare Advantage plans include some level of dental coverage, while Original Medicare generally does not cover routine dental care. In recent years, about 98% of Medicare Advantage plans have offered dental benefits, but the amount and type of coverage vary significantly by plan and location.Common dental benefits may include:

* Routine exams

* Teeth cleanings

* Dental X-rays

* Fillings

* Extractions

* Crowns

* Root canals

* Dentures

* Sometimes implants (depending on the specific plan)

However, there are important limitations:

* Annual maximum benefit amounts often apply.

* Many plans require you to use network dentists.

* Major services may have copays or coinsurance.

* Benefits can change from year to year.

When speaking with Medicare beneficiaries, I would explain it this way:

“Many Medicare Advantage plans do offer dental coverage, but not all dental benefits are the same. One plan may only cover cleanings and exams, while another may also help pay for crowns, dentures, root canals, or even implants. That’s why it’s important to review the specific plan’s dental benefits rather than assuming all Medicare Advantage plans provide the same coverage.”

As an independent Medicare agent, this is also a good opportunity to remind clients that dental coverage should be just one factor in choosing a plan. Their doctors, hospitals, prescriptions, copays, and maximum out-of-pocket costs are often even more important considerations than the dental benefit alone.

We take the extra step to go through a thorough needs analysis to make sure we’re addressing all of your needs, including Dental vision, hearing, doctors, medications, hospitals, and essential needs to give you the clarity and transparency. You deserve a qualified Medicare agent with the aloha spirit. Contact us for non-Medicare assistance.

Who Should Choose Medicare Supplement?

A Medigap plan may be the right fit if you:

- Want the freedom to see any doctor or specialist that accepts Medicare, anywhere in the country

- Prefer predictable healthcare costs with minimal out-of-pocket surprises

- Travel frequently or live in multiple states during the year

- Have chronic health conditions that require frequent specialist visits

- Are willing to pay higher monthly premiums in exchange for comprehensive gap coverage

- Don’t mind enrolling in a separate Part D plan for prescription drug coverage

If Medicare Supplement (Medigap) plans are better for long-term coverage, why don't more people choose them?

Most people don't choose Medicare coverage based on what will serve them best 10 or 20 years from now. They choose based on what looks best today.Medicare Advantage plans often have lower premiums and include benefits like dental, vision, hearing, and prescription drug coverage. That's appealing, especially when you're first enrolling.

Medicare Supplement plans usually cost more each month, which causes many people to stop the comparison there.

The question I ask through my Protection for Life™ approach is simple:

*"What coverage is most likely to protect your future self?"*

As healthcare needs increase, many retirees value the flexibility, access to providers, and predictable costs that a Medicare Supplement plan can provide.

Medicare Advantage can be the right fit for many people. But if someone can afford a Medicare Supplement and qualifies for it, it's important to understand that getting one later may be more difficult if health issues develop.

Coverage and protection aren't always the same thing.

The best Medicare decision isn't always the one with the lowest premium today—it's the one that provides the strongest protection for the years ahead.

Common Misconceptions

There are several myths that can lead people to make the wrong choice:

- “Medicare Advantage is free.” Zero-premium doesn’t mean zero-cost. You still pay Part B premiums, plus copays and coinsurance every time you receive care.

- “Medigap is too expensive.” While premiums are higher, total yearly healthcare spending can actually be lower for people with significant medical needs because out-of-pocket costs are minimal.

- “I can switch to Medigap anytime.” Your best opportunity to enroll in a Medigap plan without medical underwriting is during your 6-month Medigap open enrollment period (starting when you turn 65 and enroll in Part B). After that window, insurers in most states can deny you or charge more based on health conditions. A handful of states (Connecticut, New York, Massachusetts, Maine) have year-round guaranteed issue rules, and states like California, Oregon, and Missouri have birthday or anniversary rules that give you a limited annual window to switch plans without underwriting.

- “All Medicare Advantage plans are the same.” Plans vary dramatically by network size, formulary, copay structure, and extra benefits. Choosing the right MA plan requires careful comparison.

Why do some agents push Medicare Advantage plans over Medigap-should I be skeptical?

Most of the time, it’s a math problem. With Medigap, you pay a monthly premium. But, you must also qualify medically for a Medigap Plan. You also continue paying your Part B premium. You don’t get dental and vision, so you pay extra for an outside plan. And you don’t get prescription coverage with Medigap, which you must have or be penalized. Prescription coverage has gone way up in price. What people like is, with Medigap, you can go to any doctor that takes Medicare- no networks. And if you get a good plan (higher premium) you’ll only pay your deductible and Part B premium, and all other medical expenses will be covered at 100%. And you may have some overseas coverage. The bottom line is you will pay between $300-$500 per month to be fully covered with a Medigap Plan, Dental, Vision, and Prescriptions- whether you use it all or not, or you you can have a Medicare Advantage Plan, which covers all of that for usually no premium, (some even give back the Part B Premium!) and pay copays as you go along, with usually a $3,000-$6,000 maximum out of pocket you would ever pay in one year in the worst case scenario! (hmm… that’s $250/$500 per month worst case scenario) And many Medicare Advantage plans give free gym membership, out of hospital meals, and some other benefits. Or, you use very little benefits per year and have very little cost out of your pocket. The Medigap Plan forces you to pay that monthly cost whether you use it or not. See, mainly a math problem.Medicare Advantage vs. Medigap: Pros and Cons

A quick rundown of the trade-offs on each side.

Pros: Low or $0 monthly premiums, drug coverage bundled in, extras like dental and vision, yearly out-of-pocket cap.

Cons: Network restrictions, referrals and prior authorization common, benefits and networks can change every year, out-of-pocket costs accumulate as you use care.

Pros: See any doctor that accepts Medicare, predictable costs, no referrals, standardized benefits (Plan G, Plan N), nationwide coverage.

Cons: Higher monthly premiums, no drug coverage (separate Part D required), no dental/vision/hearing extras, medical underwriting after your initial enrollment window in most states.

Which Is Better: Medicare Advantage or Medigap?

The decision between Medicare Advantage and Medicare Supplement plans ultimately depends on your individual healthcare needs, lifestyle, and financial situation. Here are some questions to consider:

-

How often do you travel?

- If you travel frequently or live in multiple states, a Medigap plan might be more suitable due to its nationwide coverage.

-

Do you prefer lower monthly premiums or lower out-of-pocket costs?

- Medicare Advantage plans often have lower monthly premiums but higher out-of-pocket costs when receiving care. Medigap plans have higher premiums but lower out-of-pocket expenses.

-

Do you need additional benefits?

- If dental, vision, and hearing coverage are important to you, a Medicare Advantage plan may be the better choice as these benefits are often included.

-

How important is the freedom to choose healthcare providers?

- Medigap plans offer more flexibility in choosing healthcare providers, which can be crucial if you have specific doctors or specialists you want to continue seeing.

-

What does your health look like going forward?

- If you have chronic conditions or anticipate needing frequent care, the cost predictability of Medigap is often worth the higher premiums. If you’re relatively healthy, a well-chosen MA plan can save you money.

Conclusion

Choosing between Medicare Advantage and Medicare Supplement plans requires careful consideration of your healthcare needs, financial situation, and personal preferences. Both options provide valuable coverage, but they cater to different lifestyles and health requirements. By understanding the key differences and evaluating your priorities, you can make an informed decision that ensures comprehensive and cost-effective healthcare coverage.

For personalized assistance and expert guidance, consider consulting a licensed Medicare agent. They can help you weigh the trade-offs and find a plan that fits your needs. You can also get free, unbiased help from your state’s SHIP (State Health Insurance Assistance Program) counselors, or compare plans directly on Medicare Plan Finder. Use our comprehensive directory at Medicare Agents Hub to connect with trusted agents in your area today.