Medicare & Alzheimer’s: A Guide for Sons, Daughters, and Caregivers

-

September 26, 2025

When a parent or loved one is diagnosed with Alzheimer’s disease or another form of dementia, families often find themselves thrown into a whirlwind of medical, emotional, and financial decisions. Among the most pressing questions is how Medicare will (or will not) cover the care your loved one needs. For sons, daughters, and caregivers, understanding Medicare’s role is critical to ensuring quality care while managing costs.

This guide will walk you through what Medicare covers, where the gaps exist, and how working with a Medicare agent or broker can help families make the most informed choices.

The Basics: What Medicare Covers for Alzheimer’s Care

Medicare is a federal health insurance program for people over 65 and for certain younger individuals with disabilities. While it provides vital health coverage, it was never designed to fully cover long-term care needs. Families dealing with dementia often discover this the hard way.

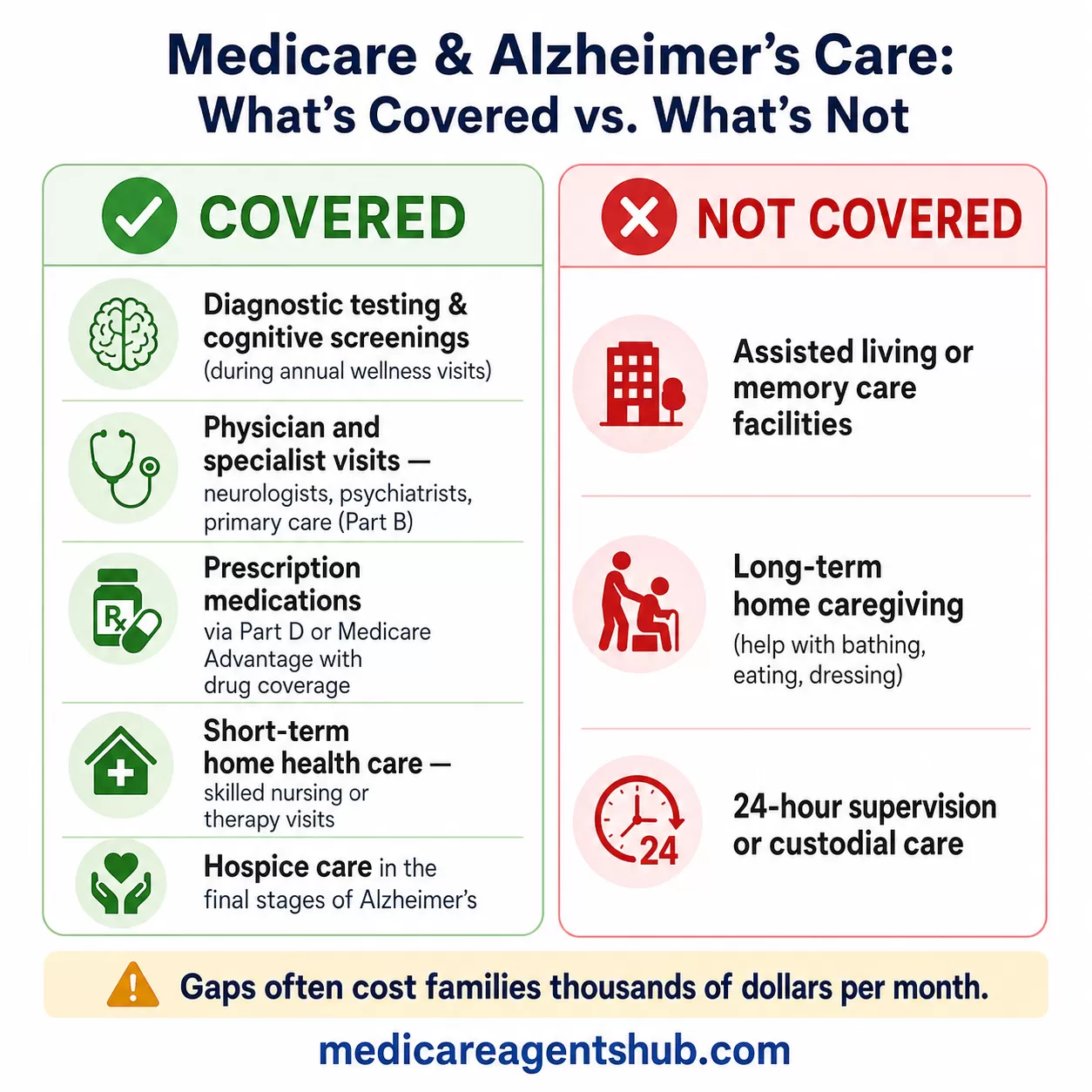

Here’s what traditional Medicare does cover:

-

Diagnostic testing and screenings - During annual wellness visits, Medicare covers cognitive assessments and referrals for further evaluation if memory issues are suspected.

-

Physician visits and specialist care - Neurologists, psychiatrists, and primary care providers are covered under Medicare Part B.

-

Prescription medications - Medicare Part D plans, or Part C (Medicare Advantage) plans with drug coverage, help pay for many dementia-related medications, though coverage varies.

-

Home health care (short-term) - If your loved one needs skilled nursing or therapy at home, Medicare may cover limited visits, but not long-term custodial care.

-

Hospice care - When Alzheimer’s reaches its final stages, Medicare covers hospice services including nursing, medications, and caregiver support.

The Gaps Families Should Know About

While the coverage above is valuable, there are significant gaps that sons, daughters, and caregivers must plan for. Medicare does not pay for:

-

Assisted living or memory care facilities

-

Long-term home caregiving (help with bathing, eating, dressing)

These costs, which can reach thousands of dollars monthly, often fall to families to manage. This is where supplemental strategies such as Medicaid long-term services and supports, long-term care insurance, or out-of-pocket savings come into play. A Medicare broker can help explain how Medicare interacts with these other programs so you don’t leave critical benefits on the table.

Can Medicare help cover in-home care for dementia patients who wander or need supervision 24/7?

Medicare generally doesn't cover 24/7 in-home care for dementia patients who wander or need constant supervision, but it can cover part-time, intermittent care for those who are "homebound" and need skilled nursing or therapy. Medicare may cover home health services, including skilled nursing, physical therapy, and speech therapy, if a doctor deems these services medically necessary and the person is "homebound". However, Medicare doesn't cover personal care like bathing or dressing, or homemaker services like laundry and shoppingMedicare Advantage & Supplemental Options

Many families explore Medicare Advantage (Part C) plans, which are offered by private insurers. Some Advantage plans include extra benefits that may help dementia caregivers, such as adult day care programs, respite care, or transportation services. The availability and quality of these benefits vary widely by plan and location, so it’s essential to compare options carefully.

Medigap (Medicare Supplement) plans are another consideration. These plans help pay deductibles, coinsurance, and copayments under Original Medicare. While Medigap does not expand coverage to include custodial care, it can significantly reduce out-of-pocket costs for hospitalizations, skilled nursing, or specialist visits related to dementia care.

Why Caregivers Should Work With a Medicare Agent or Broker

For adult children suddenly taking on caregiving roles, the Medicare system can feel overwhelming. Enrollment deadlines, penalties, plan comparisons, and fine print can create unnecessary stress during an already emotional time. This is where Medicare agents and brokers provide invaluable support.

A good Medicare broker will:

-

Review your parent’s current coverage to identify gaps or unnecessary costs.

-

Compare Medicare Advantage and Part D plans to find ones that fit dementia-related needs, such as medication coverage or caregiver support services.

-

Explain supplemental options like Medigap and help determine whether they make financial sense.

-

Guide you through enrollment and deadlines so you don’t miss key opportunities to secure coverage.

By leaning on the expertise of a local Medicare agent, sons and daughters can focus more on their loved one’s care and less on complex paperwork.

Supporting Caregivers in the Journey

Caring for someone with Alzheimer’s is more than a medical challenge, it’s an emotional journey that often leaves caregivers feeling isolated and overwhelmed. While Medicare won’t solve every challenge, understanding its coverage helps families plan ahead, reduce stress, and avoid financial surprises. If you’re helping a parent navigate this process, here are 8 questions every caregiver should ask a Medicare agent to make sure nothing falls through the cracks.

Caregivers should also seek community support. Local Alzheimer’s Association caregiving resources, senior centers, and caregiver respite programs can help ease the burden. For free, unbiased Medicare counseling in your state, you can also contact your local State Health Insurance Assistance Program (SHIP). Pairing these resources with the guidance of a Medicare broker ensures you are using every available tool to support your loved one.

Final Thoughts

For families facing Alzheimer’s or dementia, Medicare is both a lifeline and a limitation. It covers critical medical care but leaves large gaps in custodial and long-term services. Sons, daughters, and caregivers who understand these distinctions are better equipped to make informed choices about care and costs.

Partnering with a Medicare agent or broker provides clarity during one of life’s most difficult transitions. With the right information and professional guidance, you can help your loved one receive the care they deserve, while protecting your family’s financial well-being.