How to Talk to Your Parents About Medicare: A Guide for Adult Children

-

Last Updated July 21, 2026

Watching your parents approach Medicare eligibility can feel like stepping into unfamiliar territory. They may be overwhelmed by the options, unsure of deadlines, or reluctant to talk about it at all. And you, as their adult child, may not know where to start either.

This guide walks you through how to bring up Medicare with your parents, what you should both understand about how it works, and how to get them connected with the right help. The goal is to make this process less stressful for everyone involved.

Why This Conversation Matters

Medicare decisions have long-term financial and health consequences. Choosing the wrong plan, missing enrollment windows, or misunderstanding coverage gaps can lead to costly penalties and coverage gaps that last for years. Many seniors don't realize how many moving pieces are involved until they're already behind.

The reality is that most people approaching 65 haven't spent much time thinking about Medicare. They may assume it covers everything, or that their employer insurance will just roll over. Starting the conversation early gives your parents time to learn, ask questions, and make a thoughtful decision rather than a rushed one.

This process can also trigger real Medicare fatigue, where the sheer volume of information and mail becomes paralyzing. Having a trusted family member involved can break through that paralysis.

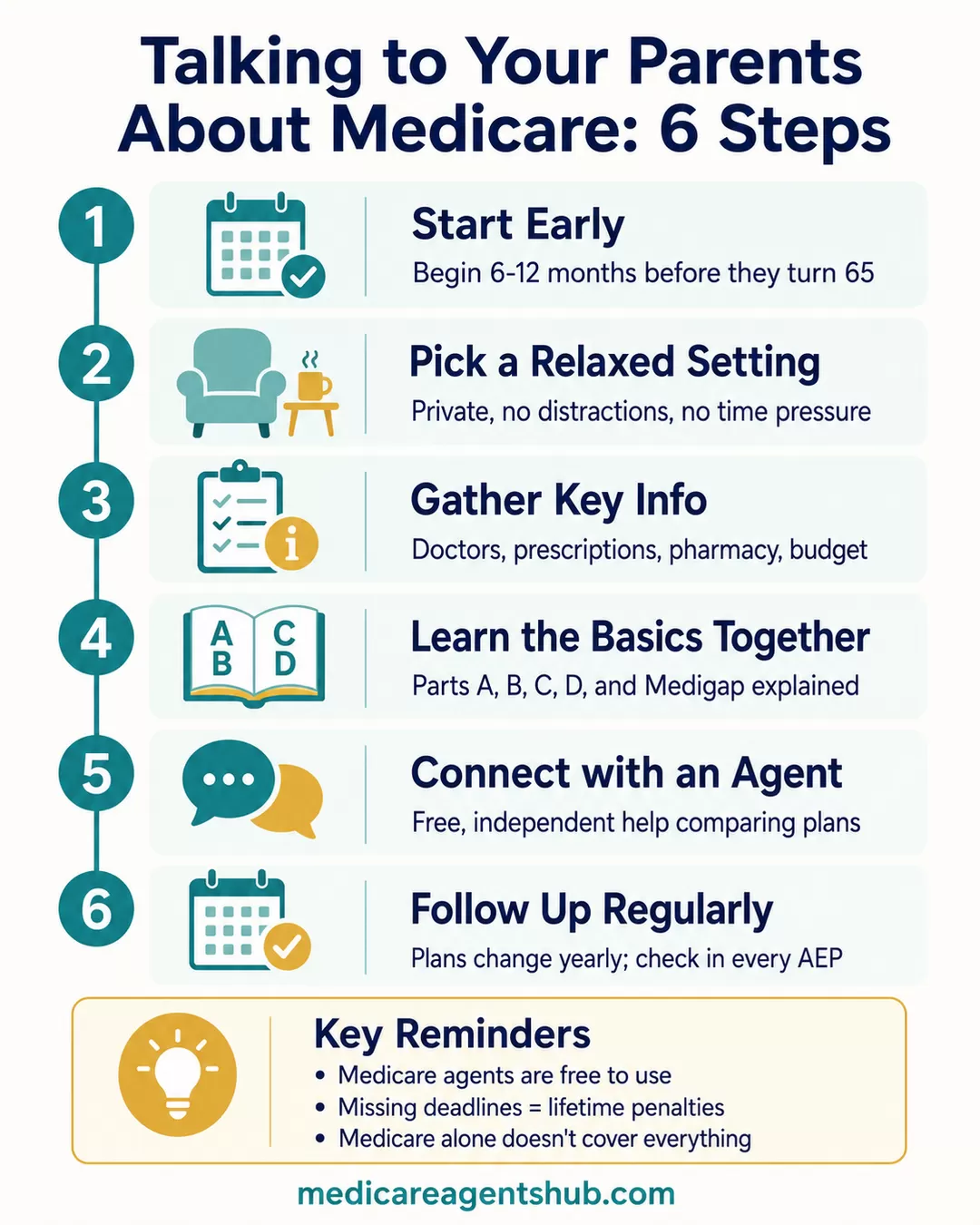

When to Start the Medicare Conversation

The Initial Enrollment Period (IEP) begins three months before your parent turns 65 and ends three months after their birthday month. That's a seven-month window, and missing it can mean late enrollment penalties that stick around permanently.

Ideally, you should start talking about Medicare six to twelve months before your parent's 65th birthday. This gives you both time to:

- Learn the basics of how Medicare works

- Gather their current medications, doctors, and pharmacy preferences

- Understand whether their employer coverage (if any) counts as "creditable coverage"

- Explore plan options in their area

- Connect with a licensed Medicare agent who can walk through the specifics

If your parent is already past 65 and on Medicare, the conversation is still worth having. Plans change every year, and what worked two years ago may no longer be the best fit. The Annual Enrollment Period (October 15 through December 7) is a natural time to revisit coverage together.

How to Approach the Conversation

Talking about Medicare with your parents can be awkward. For many seniors, the conversation feels like an acknowledgment that they're aging or losing independence. Approach it as a partnership, not a takeover.

Choose the Right Setting

Find a private, relaxed setting where you can talk without interruptions. The kitchen table after dinner, a quiet weekend morning, or a walk around the neighborhood all work better than squeezing it in during a holiday gathering or doctor's visit.

Lead with Questions, Not Answers

Start by asking what they already know. "Have you thought about what happens with your health insurance when you turn 65?" opens the door without being pushy. Let them share their concerns first. You might be surprised by what's actually worrying them.

Be Empathetic

Put yourself in their shoes. They may be dealing with the emotional weight of aging on top of confusing insurance decisions. Listen more than you talk. Acknowledge that Medicare is genuinely complicated and that it's normal to feel lost. Your reassurance that you're in this together goes a long way.

How can you create a comfortable environment for discussing Medicare with your parents?

There are several mood and environment enhancers to consider when addressing such issues with parents. One is recognizing you are switching places with them, going fromdaughter or son to adult to adult. So set up a professional setting, away from their usual place where they are the parent. Dress accordingly, if you are an agent, where a logoed shirt/blouse and nice pants/skirt. (adult cloths).

Create a check list or outline of the presentation you want to have with them, educational and informative. Gather materials ahead of time and become familiar with them. Create a folder for the materials for each of them ahead of time. There are good information materials available form providers or from Medicare. Into to Medicare, basics of Medicare Advantage planes, basics or Medicare Supplement, outlines of Prescription drug plans.

find a location away from where they hold "court," such as the dinning room table, or at a quiet coffee shop where you can offer them a cup of coffee, tea, or beverage.

Use graphics to demonstrate your major points. ask if they have questions along the way.

Make sure you reiterate they have decisions to make. You can offer to help, but they are the deciders. The bottom line is what gives them the best peace of mind at an affordable amount, that still provides good coverage for their needs.

allow time for them to absorb the information. If there is time, give them a chance to mull over or think about the information before circling back for a decision.

Understanding the Parts of Medicare

Before you can help your parents compare plans, you both need a basic understanding of how Medicare is structured. Here's the short version:

Your parents don't need to memorize all of this. The key takeaway for them is that Medicare alone doesn't cover everything, and they'll need to make choices about supplemental coverage.

If your parents live on a fixed income, don't skip this part of the conversation. Many families don't realize their parents qualify for help with premiums and drug costs. Medicare Savings Programs and Extra Help can reduce or eliminate Part B and Part D costs for those who qualify, and seniors on limited incomes may be dual-eligible for Medicare and Medicaid together. Bring up income and assets when speaking with an agent so nothing gets left on the table.

The Big Decision: Medicare Advantage vs. Medigap

This is where most families get stuck. Your parents will need to choose between two paths:

Path 1: Original Medicare + Medigap + Part D. This combination gives your parents the freedom to see any doctor or hospital that accepts Medicare (which is most of them), anywhere in the country. Medigap covers most out-of-pocket costs, so there are few financial surprises. The trade-off is higher monthly premiums.

Path 2: Medicare Advantage (Part C). These all-in-one plans often have lower premiums (sometimes $0) and may include extras like dental and vision. The trade-off is that most plans require using in-network providers and may have higher costs when care is actually needed.

The right choice depends on your parent's health, budget, doctors, medications, and lifestyle. There's no universal answer.

How to Help Your Parents Compare Plans

Once you understand the basics, the next step is comparing specific plans available in your parent's area. Here's a practical approach:

- Gather their information. Make a list of their current doctors, specialists, hospitals, prescription medications (including dosages), and preferred pharmacy. This is the foundation for any meaningful comparison.

- Check Medicare.gov. The Medicare Plan Finder lets you enter prescriptions and providers to see which plans cover them and at what cost.

- Look beyond the premium. A plan with a $0 monthly premium can still cost thousands in copays and deductibles if your parent has significant health needs. Compare total estimated annual costs, not just the monthly number.

- Verify their doctors are in-network. If your parent is considering a Medicare Advantage plan, confirm that their preferred doctors and hospitals participate. This matters more than almost anything else.

- Consider future needs. A parent who is healthy today may need more care next year. Think about whether the plan gives flexibility for changing health situations.

What is the best way to compare Medicare plans for my parents?

The easiest way to compare Medicare plans for your parents is to start with the basics: their meds (with dosages), doctors, and pharmacy. That info helps you quickly narrow down which plans actually fit. From there, I’d recommend you have an independent agent pull side-by-side comparisons of multiple insurance carriers —don’t just look at premiums, but also networks, drug costs, specialist copays, and the max out-of-pocket.If they want predictable costs, Medigap can give them peace of mind; if they’re comfortable with networks and copays, Medicare Advantage can work too.

There’s also a new, super simple guide coming out 12/2 called Helping Your Parents Navigate Medicare that walks through all of this in plain language.

When to Involve a Medicare Agent

You don't have to figure all of this out on your own. Licensed Medicare agents and brokers do this every day, and their services are free to you. They're paid by the insurance companies, not by the consumer.

A good independent agent can:

- Run side-by-side plan comparisons based on your parent's specific medications and doctors

- Explain the differences between plan types in plain language

- Handle the enrollment paperwork

- Be available year-round for questions, not just during enrollment season

The key word is independent. An independent agent or broker works with multiple insurance carriers, so they can show your parents options from different companies rather than pushing a single carrier's products. You can find a local Medicare agent who serves your parent's area and schedule a no-obligation consultation.

Your parent can also involve you in meetings with their agent. Most agents welcome family members, and having a second set of ears helps everyone feel more confident about the decision.

Common Mistakes Families Make with Medicare

Even well-intentioned adult children can stumble when helping parents with Medicare. Here are the pitfalls to watch for:

Assuming what worked for you will work for them. If you've helped one parent or relative with Medicare, that experience is useful but not transferable. Plans, costs, and coverage vary by location, health status, and what drugs someone takes. Each person needs their own evaluation.

Waiting until the last minute. The IEP doesn't pause because your family wasn't ready. Late enrollment in Part B or Part D can result in permanent premium penalties that compound over time.

Choosing a plan based on premium alone. The cheapest monthly premium almost never tells the full story. A $0 Medicare Advantage plan might cost more overall than a $150/month Medigap plan if your parent has ongoing health needs.

Not reviewing coverage every year. Medicare plans change their formularies, provider networks, and costs annually. A plan that covered everything last year might drop your parent's medication or doctor. Check the Annual Notice of Change (ANOC) letter every September and review options during the Annual Enrollment Period.

Taking over instead of collaborating. Your parents are adults making decisions about their own healthcare. Offer help and information, but let them stay in the driver's seat. Frame it as "let's figure this out together" rather than "I'll handle this for you."

Following Up After the Conversation

One conversation isn't enough. Medicare decisions benefit from ongoing check-ins, especially during key windows.

After your initial talk, follow up to make sure your parents:

- Enrolled on time and received their Medicare card

- Understand what their plan covers (and what it doesn't)

- Know how to use their benefits, including where to go for care and how to fill prescriptions

- Have their agent's contact information saved for questions that come up later

Set a reminder for yourself each fall to check in during AEP. Ask if they've received their ANOC letter, whether their doctors are still in-network, and if their medications are still covered. This annual review takes an hour and can save thousands of dollars.

Why is it helpful to follow up with your parents after discussing Medicare?

Retirees are bombarded with Call Center Sales agents everyday. Even if they signed up for a plan on or after Oct 15, they could unintentionally sign up for a new plan (change plans) and be unaware of the change. Check in with your parents periodically throughout the AEP Oct 15 - Dec 7th to ensure they receive any "new enrollment forms" or paperwork. Make one more check with them to ensure they didn't change any plans on Dec 7th.Lastly, help them to set up a spam call blocker on their phones and tell them to ignore any phone numbers they do not know. If their doctor or other official call comes in, a voicemail will be left for them to return.

You Don't Have to Do This Alone

Helping your parents with Medicare is one of the most meaningful things you can do as they age. You don't need to become a Medicare expert yourself. You just need to get them started, stay involved, and connect them with someone who knows the system.

Working with a local Medicare agent costs nothing and takes the guesswork out of plan selection. Any licensed specialist will be happy to sit down with your parents (and you, if you'd like to be there) to walk through their options with no cost or obligation.