Do I Need Long Term Care Insurance?

-

Last Updated July 21, 2026

As we age, everyday tasks that once seemed simple, like cooking a meal, taking a shower, or even going to the bathroom, can become challenging. This growing difficulty can lead to the need for additional support, which is where long-term care comes into play. Understanding long-term care and whether long-term care insurance is necessary can be crucial for securing a comfortable and worry-free future.

What Is Long-Term Care?

Long-term care is a form of assistance that helps individuals with daily living activities. This type of care ensures that basic needs are met, promoting a higher quality of life even when physical or cognitive abilities decline. Long-term care can be provided in several ways:

- Home Care: Professionals visit the individual's home for a specified number of hours per day, assisting with bathing, eating, medication management, and maintaining a clean living environment.

- Assisted Living Facilities and Nursing Homes: These facilities offer a full-time living arrangement for those needing more comprehensive support. For details on what Medicare covers after a hospital stay, see Medicare coverage for skilled nursing.

- Adult Day Care: Family members can drop off their loved ones at an adult day care center while they work, providing peace of mind that their loved ones are cared for during the day.

Essential Activities of Daily Living

To qualify for long-term care, individuals typically need help with at least two of the six activities of daily living:

- Bathing

- Incontinence care

- Dressing

- Eating

- Using the toilet

- Transferring (moving from one position to another, such as from a bed to a chair)

Long-term care providers aim to ensure that individuals are clean, comfortable, well-nourished, and able to enjoy their lives despite physical limitations.

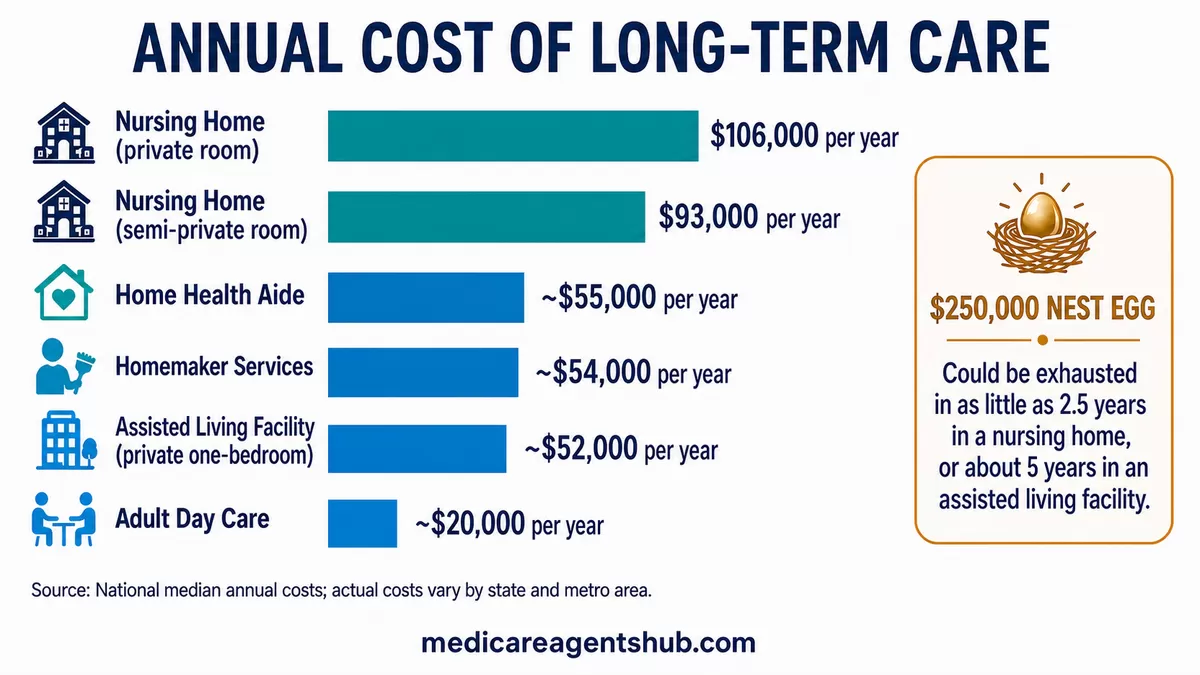

Long-Term Care Costs

Long-term care can be expensive, potentially depleting savings quickly. National median annual costs, based on the CareScout Cost of Care Survey (formerly Genworth), fall roughly in the following ranges. Actual costs vary significantly by state and metro area:

- Home Health Aide: around $55,000 per year

- Homemaker Services: around $54,000 per year

- Adult Day Care: around $20,000 per year

- Assisted Living Facility: around $52,000 per year for a private one-bedroom

- Nursing Home: $93,000 for a semi-private room and $106,000 for a private room

With numbers like these, a $250,000 nest egg could be exhausted in as little as two and a half years in a nursing home or about five years in an assisted living facility.

How can I plan for Medicare costs if I expect to need long-term custodial care in a nursing home or assisted living facility?

Medicare covers short-term skilled care, not long-term custodial care in nursing homes or assisted living, so don’t rely on it for those costs. Instead, consider long-term care insurance or a hybrid life/LTC policy, earmarked savings or annuities, and early Medicaid/asset-protection planning with an elder-law attorney (mind the five-year lookback), plus check VA benefits if eligible.Chances of Needing Long-Term Care

Contrary to common belief, most people will need some form of long-term care in their lifetime. According to the federal Administration for Community Living (which now hosts the former LongTermCare.gov resources), roughly 70% of Americans aged 65 and older will require long-term care services. Men typically need these services for an average of 2.2 years, while women need them for about 3.7 years. About 20% of individuals will need long-term care for more than five years.

How can I plan for Medicare costs if I expect to need long-term custodial care in a nursing home or assisted living facility?

As 70% of us will need some form of extended care, and Medicare does not cover this, working with your Agent/Broker to plan the best options based on your situation is highly recommended. It is the #1 reason for bankruptcy over age 65, therefore a very important topic to discuss!Ways to Pay for Long-Term Care

Given the high costs, planning how to pay for long-term care is essential. Common options include:

- Personal Resources: Savings and investments can cover long-term care costs.

- Medicare and Major Medical Health Insurance: Medicare does not cover long-term custodial care, and it does not pay for assisted living. See our article on Medicare's role in long-term care coverage for details on what Medicare does and doesn't pay for.

- Medicaid: Often provides coverage for long-term care, but requires spending down assets to qualify. Learn more at Medicaid.gov's long-term services and supports page.

- Long-Term Care Insurance: Specifically designed to cover long-term care costs.

- Life Insurance Policies or Annuity Contracts: These can sometimes be leveraged to pay for long-term care. Learn more in how annuities play a role in Medicare planning.

- Hybrid/Combination Policies: Life insurance or annuity contracts that include long-term care benefits. See also: Decoding Your Dream Retirement: Medicare, Life Insurance, and Annuities.

How can I plan for Medicare costs if I expect to need long-term custodial care in a nursing home or assisted living facility?

There are 3 options:1. If you have sufficient assets $1 million+, you can self fund.

2. Spend down your assets and go on Medicaid.

3. Purchase Long Term Care insurance.

Also remember, care can be in your home or at an Adult Day care facility.

What Is Long-Term Care Insurance?

Long-term care insurance is a policy designed to cover expenses related to long-term care. By finding a local insurance agent, individuals can determine the coverage amount needed and find the most affordable premiums. Before purchasing a policy, it's essential to understand the available options, tax advantages, and overall costs.

Long-Term Care Insurance Options

There are two primary types of long-term care insurance:

-

Traditional Long-Term Care Insurance Policies: These are becoming less common but involve paying a set premium for life. They cover long-term care expenses if needed. Key considerations include the policy amount, length of coverage, and waiting period before benefits can be accessed. Note that the cost of these policies may rise over time due to inflation and increasing care costs.

-

Hybrid Long-Term Care Insurance Riders: These combine long-term care benefits with other financial products, such as life insurance or annuities. There are two main types:

- Life Insurance Hybrid: Allows accelerating the death benefit for long-term care expenses. If the benefit is not used for care, it goes to the heirs.

- Annuity Hybrid: Involves a lump-sum investment or regular payments, providing income throughout retirement and covering long-term care costs if needed. These funds grow tax-free and are tax-exempt when used for long-term care.

Tax Advantages of Long-Term Care Coverage

Long-term care insurance premiums are partially tax-deductible, and the deduction limit increases with age. For the 2025 tax year, the IRS caps the eligible premium amount (per person) as follows, per Revenue Procedure 2024-40:

- Age 40 and under: up to $480 per year

- 41 to 50: up to $900 per year

- 51 to 60: up to $1,800 per year

- 61 to 70: up to $4,810 per year

- 71 and over: up to $6,020 per year

These limits are adjusted annually. Check the current IRS revenue procedure or ask a tax professional for the year that applies to you.

How Much Does Long-Term Care Insurance Cost?

The cost of long-term care insurance varies based on several factors:

- Age: Older individuals pay higher premiums due to increased risk.

- Gender: Women generally pay more because they live longer and are more likely to need long-term care.

- Marital Status: Married individuals often pay lower premiums.

- Coverage Amounts: Higher coverage amounts result in higher premiums.

As one illustration, a 55-year-old male in good health might pay around $950 per year for a policy valued at $165,000, while a 55-year-old female might pay about $1,500 for the same coverage.

How to Buy Long-Term Care Insurance

Purchasing long-term care insurance involves several steps:

- Contact a Reputable Insurance Agent: Find an agent who can guide you through the process.

- Discuss Your Needs and Financial Situation: Determine the coverage amount and affordable premiums.

- Compare Options: The agent will find the best policies that meet your needs.

- Complete the Purchase: Follow the agent's guidance to finalize your policy.

How can I plan for Medicare costs if I expect to need long-term custodial care in a nursing home or assisted living facility?

You want to apply as early as possible to try to qualify for long-term care policies. They are carefully underwritten, so you have to be in reasonably good health in order to buy long-term care policies!They are quite easy to calculate the cost for because you really only need about three pieces of information to fill out an application and get a quote on what those will cost. About all you need to know is the amount of money needed per month, and the period of time that you want the Benefits to run, and finally What waiting period to use before your benefits begin after you qualify to start receiving benefits. Typically. Those would be 60 or 90 days, and it acts like a deductible!

State Medicaid Programs for Long-Term Care Insurance

Medicaid can help cover long-term care costs, but typically you must spend down your assets to qualify. For more on this, see how Medicare and Medicaid work together. States have a five-year lookback period to review asset transfers made before you apply. Improper transfers during that window can trigger a penalty period of Medicaid ineligibility, and many states also participate in estate recovery after the recipient's death to recoup costs.

How can I plan for Medicare costs if I expect to need long-term custodial care in a nursing home or assisted living facility?

If you are already certain that you will need Long Term Care, it is too late to purchase coverage. Speak with an Estate Planning attorney about a Medicaid Trust that can protect your assets and still enable you to qualify for Medicaid. Medicaid does currently provide coverage for LTC.Frequently Asked Questions

What's the best age to buy long-term care insurance?

Most agents suggest shopping between ages 55 and 65. Premiums are still reasonable at that age, and applicants are less likely to have a health condition that would trigger a denial or a rate-up (a higher premium tier assigned during medical underwriting).

Is long-term care insurance worth it if I have substantial savings?

It depends on how much you're willing to spend down. A private nursing home room runs about $106,000 a year, so even large portfolios can be drawn down quickly by a multi-year care event. A policy can protect that savings for a surviving spouse or heirs.

What happens if I'm denied for coverage?

Traditional long-term care policies use medical underwriting, and denials do happen. If you're turned down, hybrid life insurance policies with a long-term care rider are usually easier to qualify for. A short-term care policy, which covers care for up to a year rather than multiple years, is another option worth asking about.

Does Medicare pay for long-term care?

No. Medicare covers short stays in a skilled nursing facility after a qualifying hospital admission, but it does not pay for extended custodial care or assisted living. See Medicare's role in long-term care coverage for the full breakdown.

What happens to my Medicare coverage if I enter a skilled nursing facility for rehab but then need long-term care?

Medicare and most health insurance, including Medicare Supplement Insurance (Medigap), don’t pay for long-term care. This type of care (also called “custodial care” or “long-term services and support”) includes medical and non-medical care for people who have a chronic illness or disability.Most long-term care isn’t medical care. Instead, most long-term care helps with basic personal tasks of everyday life, sometimes called “activities of daily living.” This may include:

Help with personal care assistance (like dressing, bathing, and using the bathroom)

Home-delivered meals

Adult day health care

You might qualify for long-term care through Medicaid, or you can choose to buy private long-term care insurance.

You can get non-medical long-term care services at home, in the community, in an assisted living facility, or in a nursing home. It’s important to start planning for non-medical long-term care now to maintain your independence and make sure you get the care you may need, in the setting you want, now and in the future. If you’re an American Indian or Alaska Native, contact your local Indian health care provider for more information.

Conclusion

Long-term care insurance can provide peace of mind and financial security, ensuring you receive the necessary care without burdening your family. As the chances of needing long-term care increase with age, it's wise to explore your options early. Speak with an insurance agent to discuss your needs and find a policy that offers the best protection for your future. For a broader view of how insurance products work together, read Planning Ahead: What Medicare Covers vs. What Your Life Insurance Can Help With.