What Medicare Home Health Actually Pays For and the Custodial Care Line

-

July 8, 2026

Families keep discovering the same painful gap: Medicare will send a nurse or physical therapist into the home after a surgery or a fall, but it will not pay for the aide who bathes Mom, cooks her lunch, or watches her overnight. Agents on Medicare Agents Hub describe this misunderstanding as one of the most damaging assumptions their clients arrive with. The word "home health" sounds broad. The benefit is not.

Last updated July 2026. Medicare costs and plan benefits change annually.

Quick answer: Medicare home health may cover skilled nursing, therapy, medical social services, supplies, and limited aide services if you are homebound, need part-time or intermittent skilled care, and use a Medicare-certified home health agency. It does not cover 24-hour care, meal delivery, live-in aides, or custodial help like bathing and dressing when that is the only care needed.

What Medicare Home Health Care Actually Covers

Medicare covers medically necessary, part-time or intermittent home health services. Agents consistently name the same list of covered services in their answers:

- Skilled nursing care provided by a registered nurse or licensed practical nurse (wound care, IV therapy, injections, medication management, vital sign monitoring)

- Physical therapy, occupational therapy, and speech-language pathology

- Medical social services (counseling, help with community resources related to your illness)

- Home health aide services for personal care like bathing and dressing, but only if you are also receiving skilled nursing or therapy at the same time

- Medical supplies such as wound dressings and catheters

- Durable medical equipment (walkers, wheelchairs, hospital beds, oxygen equipment)

Medicare typically pays 100% of the approved cost for home health services. The exception is durable medical equipment, where you pay 20% of the Medicare-approved amount after meeting the Part B deductible.

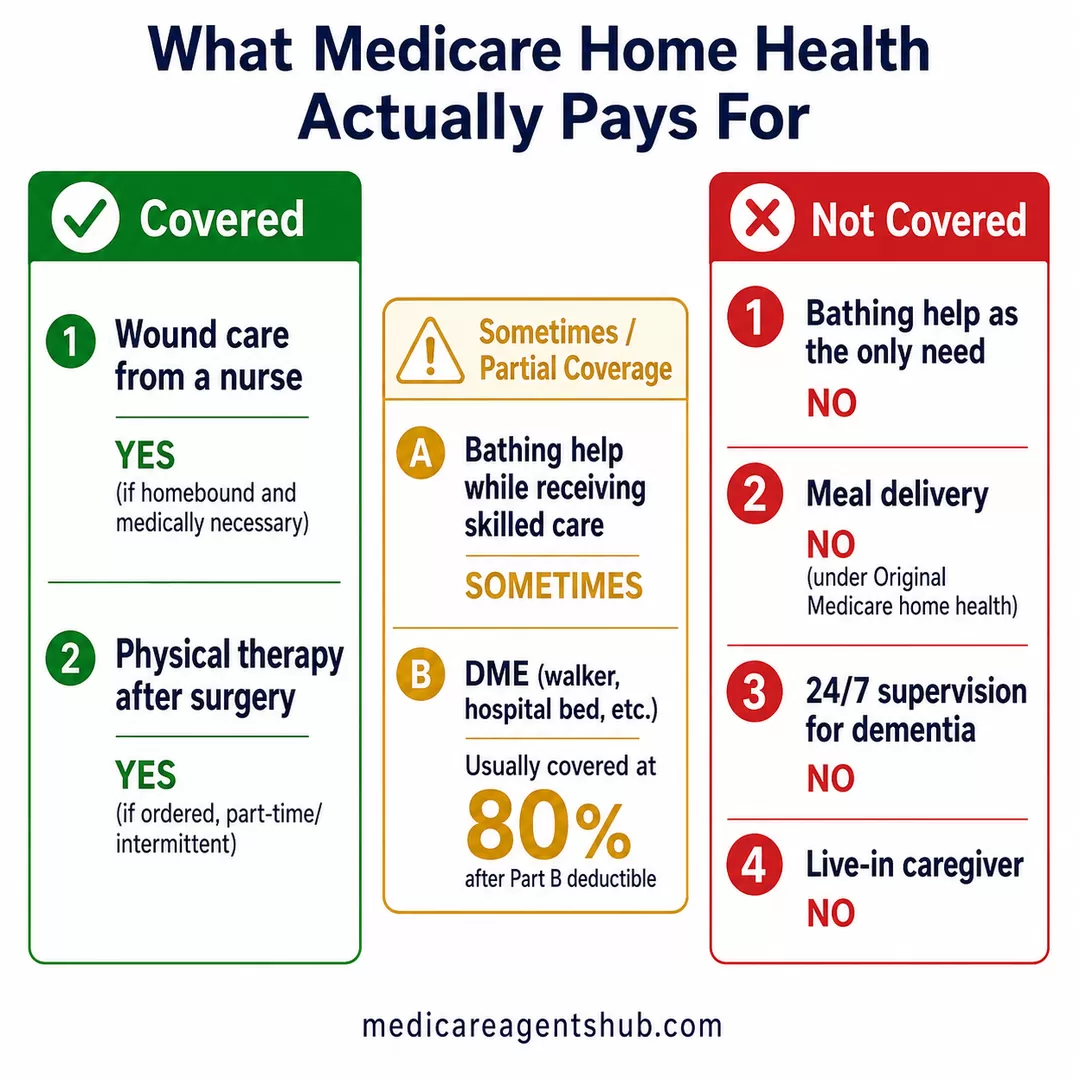

| Need at home | Does Medicare usually cover it? |

|---|---|

| Wound care from a nurse | Yes, if homebound and medically necessary |

| Physical therapy after surgery | Yes, if ordered and part-time/intermittent |

| Bathing help while receiving skilled care | Sometimes |

| Bathing help as the only need | No |

| Meal delivery | No under Original Medicare home health |

| 24/7 supervision for dementia | No |

| Live-in caregiver | No |

| DME like walker/hospital bed | Usually 80% after Part B deductible |

I've heard Medicare covers home health care, but what exactly does that include?

Medicare covers home health care under Part A and Part B when it’s medically necessary and ordered by a doctor. This can include part-time skilled nursing care, physical therapy, occupational therapy, speech therapy, and limited home health aide services. The care must be provided by a Medicare-certified home health agency, and you must be considered homebound. Medicare does not cover 24-hour care, meal delivery, or custodial (non-medical) care like help with bathing or dressing if that’s the only service needed.The Four Conditions You Must Meet

Not everyone who wants home health care qualifies for it. Agents point to four conditions that must all be in place before Medicare will approve the benefit:

- You must be homebound. This means leaving your home requires considerable effort (using a wheelchair, walker, or crutches, needing special transportation, or needing help from another person) or is medically inadvisable because of your condition.

- You need skilled care. You must require skilled nursing, physical therapy, speech therapy, or occupational therapy on a part-time or intermittent basis.

- A doctor must order your care. A physician or qualifying practitioner must document a face-to-face encounter within 90 days before (or 30 days after) home health services begin and establish a written plan of care.

- A Medicare-certified home health agency must provide the services.

"Part-time or intermittent" has a specific meaning under CMS rules. In most cases, it means skilled nursing care and home health aide services combined can total up to 8 hours per day, for a maximum of 28 hours per week. In some situations, your provider can request up to 35 hours per week for a short period if medical necessity supports it. If you need ongoing daily or around-the-clock help, Medicare's home health benefit will not cover that level of care. You may still qualify for covered intermittent skilled services, but extra custodial hours would need to be paid privately, covered through Medicaid if eligible, or addressed through other long-term care planning.

I need help at home after my surgery. Will Medicare cover a home health aide or am I on my own?

Short answer, Yes, if you meet all the criteria.Long answer: if you meet these four conditions, it may be covered:

1. Homebound status — leaving home requires considerable effort or is medically inadvisable

2. Skilled care need — you require skilled nursing, physical therapy, speech therapy, or occupational therapy

3. Medicare-certified home health agency must provide all services

4. Doctor’s face-to-face encounter documented within 90 days before or 30 days after services begin

If you have a Medicare Advantage your plan may cover it a little differently so I would advise calling them, consulting with your agent, or reviewing your evidence of coverage to verify.

The Custodial Care Wall

This is where the gap hits families hardest. Custodial care is help with activities of daily living: bathing, dressing, eating, toileting, transferring from a bed to a chair, and general supervision. When that is the only type of care someone needs, Medicare does not pay for it. Not under Original Medicare, not under a Medicare Supplement, and not under most Medicare Advantage plans.

Medicare also does not cover:

- 24-hour care at home

- Meal delivery

- Homemaker services (shopping, cleaning, laundry) unrelated to your care plan

- Live-in aides or overnight sitters

Agents draw a bright line: if a registered nurse or therapist is doing something that requires clinical training, Medicare may cover it. If someone is doing tasks that a family member could safely perform, Medicare calls that custodial and will not pay. The distinction has nothing to do with how much help you need. It has everything to do with whether the help requires a skilled professional.

What type of Medicare coverage do I need to cover in-home caregivers?

With Medicare Advantage plans, you'll have some costs with it. More likely, though, you might be asking about in-home caregivers, like just a home health aide, someone to help around the house with what's called custodial care. So unfortunately, Medicare does not pay for any custodial care, really anywhere. It used to many years ago, but they don't have that built in anymore.

That's why it's important when you're able to qualify health-wise that you purchase either a home health care policy or a short-term or long-term care plan. Care here has gotten really expensive for the past three years. There are new ways of doing it to make it more cost-effective and better overall. Short-term care can really suffice for a lot of situations. It’s relatively inexpensive, and home health care as well is even less costly.

It can provide what you need, so it's important to look for those things before you actually need care. If there's any question about this, I'm happy to help out. Here at Grand Church,

After Surgery: What Home Health Looks Like in Practice

The most common entry point for home health is recovery after a surgery, a cardiac event, or a fall. If your doctor determines you are homebound and need skilled care at home, Medicare can cover a visiting nurse for wound care, a physical therapist to rebuild strength and mobility, and a home health aide to help with bathing or dressing while you are also receiving that skilled care.

For post-surgical recovery, the benefit often runs several weeks. Your doctor sets the plan of care, and if recovery takes longer than initially estimated, the doctor can extend it. But the care must remain skilled and medically necessary. In some cases, Medicare home health can also help maintain your current level of function or slow the rate of decline from a chronic condition, as long as the care remains skilled and meets the homebound and care-plan rules. Once the skilled services end, the home health aide benefit ends with them.

If you need skilled nursing facility care before going home, Medicare Part A covers up to 100 days of skilled nursing facility care per benefit period if you meet the qualifying rules. Days 1 through 20 are $0 after the Part A deductible. Days 21 through 100 require a $217 daily coinsurance in 2026. After day 100, Medicare pays nothing.

Will Medicare cover my recovery after surgery?

Usually yes. BUT it does depend on what kind of recovery care you need and where you get it.Hospital stay after surgery:

- If you're admitted as an inpatient, Part A covers your room, meals, nursing care, and medications during the stay. You'll owe the Part A deductible ($1,736 per benefit period in 2026), and after 60 days there are daily coinsurance charges.

Skilled nursing facility (SNF):

- If your doctor sends you to a skilled nursing facility to continue recovering say, for physical therapy or wound care. Part A can cover up to 100 days, but only if you had a qualifying inpatient hospital stay of at least 3 days first. Days 1–20 are fully covered. Days 21–100 have a daily copay.

Home health care:

- If you're homebound and need skilled nursing or therapy at home, Part A or Part B covers it at no cost to you, as long as a Medicare approved home health agency provides the care and your doctor orders it.

Outpatient follow-up:

- Doctor visits, physical therapy, lab work, and durable medical equipment (like a walker or wheelchair) fall under Part B. You'll pay 20% of the Medicare approved amount after meeting your Part B deductible ($283 in 2026).

What Medicare won't cover:

- Long term custodial care (help with bathing, dressing, eating) isn't covered if that's the only care you need. Same with 24 hour home care or meal delivery.

One important note: if you have a Medicare Advantage plan or a Supplement, your out of pocket costs will look different, and often much lower. That's worth a quick conversation so we can map out what your recovery would actually cost based on the plan you're on.

The critical thing to understand: once your condition stabilizes and skilled care is no longer needed, you are responsible for any ongoing help. If you still need someone to help you get dressed, prepare meals, or move around the house safely, that falls on you or your family to arrange and pay for privately.

The Dementia Scenario

Dementia and Alzheimer's disease create one of the most painful collisions with the custodial care line. Medicare may cover medically necessary skilled nursing or therapy at home for someone with dementia if they are homebound and meet the home health rules. Medicare Part B may also cover cognitive assessments and related medical care. But Medicare will not pay for the 24/7 supervision that most dementia patients eventually need: the wander-watch, the overnight monitoring, the constant presence to keep someone safe.

Agents consistently name this as one of the most difficult conversations they have with families. A dementia diagnosis does not trigger a Medicare benefit for around-the-clock in-home care. When families ask what their options are, agents point to several paths outside of Medicare:

- Medicaid home and community-based services (HCBS) waivers can cover in-home custodial care, but eligibility depends on income and asset limits that vary by state

- VA Aid and Attendance benefits for veterans or surviving spouses who need help with daily activities

- Long-term care insurance purchased before the diagnosis, which can cover in-home care, assisted living, or nursing home costs

- PACE (Program of All-Inclusive Care for the Elderly) for people who qualify for both Medicare and Medicaid and live in a PACE service area, which coordinates medical and custodial care including home care, personal care, adult day services, and transportation when approved by the PACE team

- Hospice care under Medicare Part A in advanced stages, when Alzheimer's is recognized as a terminal condition

My mom has dementia and needs in-home dementia care. What Medicare plan will cover this?

Medicare does not directly pay for long-term, non-medical in-home custodial care (bathing, dressing) for dementia, but it covers medically necessary intermittent skilled care via Part A or B, and more comprehensive support through Medicare Advantage (Part C) plans. Key options include Special Needs Plans (SNPs) for dementia, the GUIDE Model for care coordination, and hospice for advanced stages.Key Medicare Coverage for Dementia Care:

Medicare Part B (Medical Insurance): Covers doctor visits, cognitive assessments, and some outpatient therapy.

Medicare Home Health Care (Part A or B): Covers skilled nursing or therapy (Physical, Occupational, Speech) if the patient is homebound and needs part-time, intermittent care.

Medicare Advantage (Part C): These private plans often provide extra benefits, such as in-home support, respite care, and meal delivery.

Special Needs Plans (SNPs): Specialized Advantage plans designed for people with specific chronic conditions, including dementia.

GUIDE Model: A new Medicare program that provides care navigation and supports caregivers, aiming to help seniors stay in their homes longer.

Hospice Care: Covered by Part A for patients with a terminal prognosis of 6 months or less, which can include in-home care.

Do Medicare Advantage Supplemental Benefits Close the Gap?

Some Medicare Advantage plans have started offering supplemental in-home benefits that go beyond what Original Medicare provides. These can include limited caregiver hours, meal delivery after a hospital discharge, transportation to medical appointments, and adult day care services. Some chronic-condition Special Needs Plans (C-SNPs) offer additional care coordination for conditions like dementia or heart failure.

Agents flag two important caveats about these benefits. First, they vary wildly by plan, county, and year. A plan that offers 80 hours of in-home support in one zip code may offer nothing in the next county over. Second, these supplemental benefits can be changed or eliminated during the Annual Notice of Change (ANOC) each fall. A benefit you relied on this year may not exist next year.

The consensus among agents is clear: Medicare Advantage supplemental in-home benefits are not a substitute for long-term care planning. They can help bridge a short gap after a hospitalization, but they will not cover the kind of sustained, daily custodial care that a progressive condition like dementia eventually demands.

Does Medicare Advantage cover home health care?

If that is the case, typically, the situation would be that you would be homebound. Most of the time, this happens post-surgery or post-hospitalization. You may not be able to come into the doctor's office to receive services such as checking vitals, changing bandages for wound care, or things of that nature, where they would send out a skilled practitioner.

It is not somebody coming in to help with cooking and cleaning and doing all of those things, but it can cover things such as if you are not able to perform one of the activities of daily living, like feeding, toileting, bathing, grooming, and things of that nature. There are six activities of daily living, so if you're not able to perform those, then you may qualify for someone to come in to help you receive those services on a part-time or intermittent basis.

So it is not long-term care. Just to be very clear, Medicare does not cover long-term care, but they will cover short-term rehabilitative types of care. So it could also include physical therapy. If you're not in a skilled nursing facility or something like that post-surgery, it could apply.

So I hope that answers your question, and keep them coming. Take care. Bye-bye.

What Agents Tell Families to Do Now

The agents who answered these 15 questions returned to the same planning advice over and over: understand what Medicare does not cover, and make arrangements before you need care. The options they most frequently recommend:

- Long-term care insurance. Traditional policies cover custodial care at home, in assisted living, or in a nursing home. The younger and healthier you are when you apply, the lower the premiums and the easier the underwriting. Waiting until you need care usually means it is too late to qualify.

- Hybrid life insurance or annuity products with LTC riders. These let you access a portion of the death benefit or annuity value for care needs. If you never use the care benefit, the money passes to your beneficiaries.

- Medicaid planning. For those with limited assets, Medicaid can cover long-term custodial care. But eligibility rules are strict, vary by state, and include a five-year lookback period on asset transfers. An elder-law attorney can help navigate this path.

- Personal savings and self-funding. Some agents note that individuals with assets above roughly $1 million may be positioned to self-fund care, but even then, nursing home costs of $8,000 to $10,000 per month can deplete savings faster than expected.

Around 70% of Americans who reach age 65 will need some form of long-term care. Agents urge families to start planning in their 50s or early 60s, well before a health crisis forces the conversation.

If I need long-term care in the future, how does Medicare fit into that plan, and what should I be doing now to prepare?

It's true that around 70% of Americans who are 65 today will need long-term care at some point. Medicare, unfortunately, will not cover true long-term care needs such as nursing homes or custodial care. Medicare will continue to help pay for inpatient and outpatient medical services, but it will not help pay for your stay at a nursing home. To prepare, I recommend working closely with your trusted insurance agent and your financial planner to come up with a plan.Even though it seems far off in the future, I recommend starting these conversations when you are in your 50s to early 60s. Too many people wait until they are facing a long-term care need to start planning, which leaves them very few options. Unfortunately, many people who leave it until then will likely be forced to see how quickly they can qualify for Medicaid to help them pay for long-term care. It's certainly worth it to plan early.

Frequently Asked Questions

Does Medicare pay for a caregiver to sit with an elderly parent?

Usually no. Medicare does not cover companion care, supervision, or custodial help when that is the only care needed.

Does Medicare cover a home health aide for bathing?

Sometimes, but only on a part-time or intermittent basis and generally only when you are also receiving skilled nursing or therapy through a Medicare-certified home health agency.

Does Medicare cover 24-hour home care?

No. Medicare does not cover 24-hour-a-day care at home.

Does Medicare cover dementia care at home?

Medicare may cover medically necessary skilled care or therapy for someone with dementia if they meet the home health rules, but it does not cover ongoing supervision or long-term custodial dementia care.

Does Medicare Advantage cover more home care than Original Medicare?

Some plans offer limited supplemental benefits, but they vary by plan, county, and year and should not be treated as a substitute for long-term care planning.

Know the Line Before You Need the Care

Medicare home health is a real benefit. It can support recovery after an illness, surgery, or fall, and in some cases it may help maintain function or slow decline. But it is still limited to medically necessary, part-time or intermittent skilled care for people who meet the homebound and care-plan rules. It was never designed to replace a live-in aide, fund ongoing supervision for dementia, or cover daily help with cooking, cleaning, and bathing when that is the only care needed.

The families who navigate this best are the ones who learn the rules before the crisis hits. Talk to a local Medicare agent about what your plan covers, and if long-term care is even a remote possibility, explore coverage options while health and age are still on your side. The gap between what Medicare pays for and what families actually need is real, but it does not have to be a surprise.