Medicare Won’t Pay for the 24/7 Watch: What Families of Wandering Dementia Patients Actually Do

-

June 2, 2026

One licensed Medicare agent in Port Charlotte, Florida knows this coverage gap personally. Mary Turner watched dementia transform her stepfather, a man she describes as outstanding, gentle, someone who never raised his voice and treated her and her sister as his own. The disease turned him into someone she barely recognized. She and her sister took turns staying with him around the clock, hiring private caregivers to cover the hours they couldn't. Medicare paid for none of it.

Can Medicare help cover in-home care for dementia patients who wander or need supervision 24/7?

Having gone through helping take care of my stepfather who had dementia, I know what a daunting task it can be. He was an outstanding man who never raised his voice and treated my sister and I as if we were his very own. Dementia turned him into someone I barely recognized at times.Unfortunately, whether you have medicare and a supplement or a medicare advantage plan, neither will help because medicare does not pay for long term care whether it be in home or in a facility. My sister and I took turns staying with my stepfather "dad" and employed caretakers for the other days and nights since he required 24/7 care.

If the person already has dementia there is little you can do other than pay out of pocket until medicaid qualified. If this is a hypothetical situation, there are several ways you can protect yourself for long term care.

Her story is painfully common. Families dealing with a loved one who wanders, who needs constant supervision, who cannot safely be left alone for even an hour, eventually hit the same wall: Medicare does not pay for custodial care. Not through Original Medicare, not through a supplement, not through a Medicare Advantage plan. The coverage gap between what Medicare considers "skilled" and what a dementia patient actually needs is the single most expensive surprise in senior healthcare.

But families are not powerless. Across thousands of answers from licensed Medicare agents, a consistent set of strategies emerges. Think of it as a patchwork quilt of government programs, specialized plans, and family coordination. Here are the eight strategies that come up again and again.

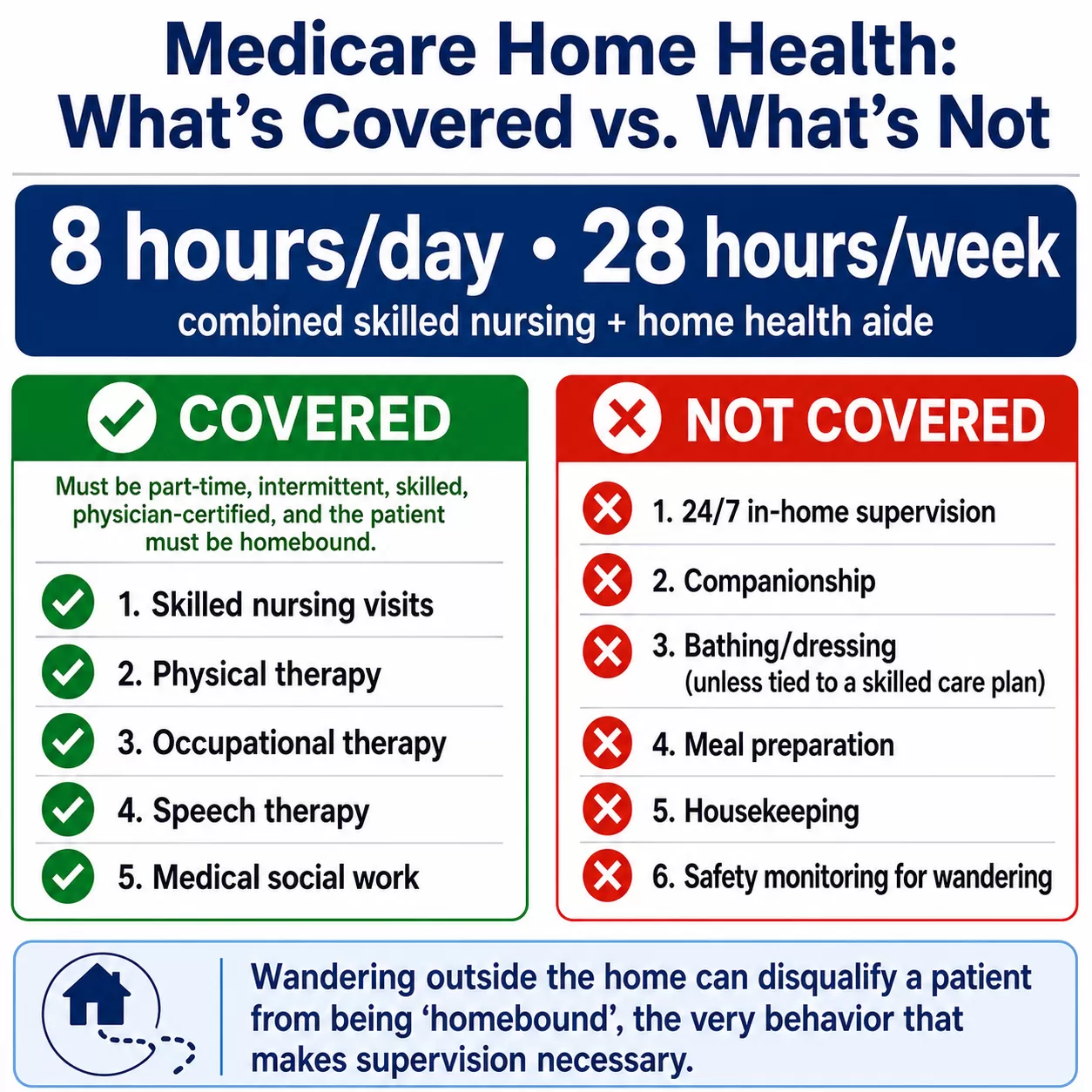

1. Understand What Medicare Will (and Won't) Cover First

Before exploring alternatives, it helps to know exactly where Medicare draws the line. Medicare covers part-time, intermittent skilled care if a physician certifies the patient is homebound and needs skilled nursing or therapy. That can include skilled nursing visits, physical therapy, occupational therapy, speech therapy, and medical social work, all provided by a Medicare-certified home health agency.

What Medicare explicitly will not cover: 24/7 in-home supervision, companionship, help with bathing and dressing (unless tied to a skilled care plan), meal preparation, housekeeping, or safety monitoring for wandering. Agents are nearly unanimous on this point.

One number comes up repeatedly in agent answers: Medicare generally limits covered home health services to 8 hours per day and 28 hours per week of combined skilled nursing and home health aide visits, though limited exceptions may allow more in certain cases. That benefit is real, but the definition of "homebound" is strict, and the care must be skilled and intermittent, not custodial.

The catch for families of wandering dementia patients: the very behavior that makes 24/7 supervision necessary (wandering outside the home) can technically disqualify a patient from being considered "homebound" under Medicare's definition. It is a frustrating paradox that agents flag frequently.

Can Medicare help cover in-home care for dementia patients who wander or need supervision 24/7?

That's a great question. In short, the answer unfortunately is no, but there are other resources that might be available for your loved one.Medicare will cover medically necessary home health care (short-term, intermittent skilled care), but there are some key requirements:

- A physician must attest that the patient is homebound and needs skilled nursing or therapy

- Care is part-time or 'intermittent' (generally 8 hours or less daily, up to 7 days per week, for 21 days or less)

- Services are provided by a Medicare-certified home health agency

Medicare does NOT cover:

- 24/7 in-home care

- Personal or custodial care (help with bathing, dressing, supervision, or companionship) unless it's part of the skilled care plan

Often times, families find themselves patching together multiple resources to help meet their loved one's care needs. Think of it as a patchwork quilt. Government programs are usually the best place to start. Medicaid (state-based health insurance), unlike Medicare, does cover long-term custodial care. But exactly what is covered can vary from state to state. Many states offer Home and Community Based Services (HCBS) Waivers that help individuals with dementia gain access to care at home instead of an institution. Keeping your loved one in a familiar environment as long as possible. Eligibility for Medicaid is based on income and assets, and because those amounts vary by state it is important to get with your local Medicaid office for those details and to apply for their services. For those who are eligible for Veterans' Benefits, VA Aid and Attendance Pension can help pay for in-home care, assisted living, or nursing home care.

For those who plan ahead, a Long-Term Care policy can help cover costs for in-home caregivers, assisted living, or nursing home. Policy costs and details vary from plan to plan, and should be purchased earlier in life. It is always wise to work with an experienced broker who is familiar with local resources.

2. Apply for Medicaid Home and Community-Based Services (HCBS) Waivers

When agents are asked what families should try first, Medicaid is almost always the answer. Unlike Medicare, Medicaid does cover long-term custodial care, including in-home supervision for dementia patients.

Many states offer Home and Community-Based Services (HCBS) waivers specifically designed to help individuals with dementia receive care at home instead of in an institution. These waivers can keep a loved one in a familiar environment as long as possible, which is often better for the patient and less expensive than facility placement.

Eligibility is income- and asset-based, and the specifics vary by state. The best starting point is your local Medicaid office or your county's Office on Aging. If a loved one has assets above Medicaid's threshold, an elder care attorney can help with legally compliant planning strategies. Multiple agents recommend consulting one early rather than waiting until assets are depleted.

3. Look Into Chronic Condition Special Needs Plans (C-SNPs)

There is a type of Medicare Advantage plan that most families never hear about: Chronic Condition Special Needs Plans, or C-SNPs. These are specifically designed for people with certain chronic conditions, and in some areas, plans may be available for people with dementia or related chronic conditions. They offer enhanced care coordination, monitoring assistance, access to caregiver resources, and supplemental benefits tailored to managing complex health needs.

C-SNPs differ from standard Medicare Advantage plans in that they can layer on extra benefits targeted at the enrollee's specific condition. For dual-eligible individuals (people who qualify for both Medicare and Medicaid), the Program of All-Inclusive Care for the Elderly (PACE) is another option worth exploring. PACE programs provide comprehensive medical and social services and are built specifically to help people remain at home.

Not every area has a dementia-focused C-SNP available, so working with a local agent who knows your county's plan landscape is the fastest way to find out what is offered near you.

4. Explore Medicare's GUIDE Program

CMS launched the Guiding an Improved Dementia Experience (GUIDE) model to address exactly the kind of gap families face. It provides comprehensive dementia care through a care navigator who coordinates medical care, connects caregivers with support services, and can arrange respite care so family members get a break.

My mom has dementia and needs in-home dementia care. What Medicare plan will cover this?

Medicare does not directly pay for long-term, non-medical in-home custodial care (bathing, dressing) for dementia, but it covers medically necessary intermittent skilled care via Part A or B, and more comprehensive support through Medicare Advantage (Part C) plans. Key options include Special Needs Plans (SNPs) for dementia, the GUIDE Model for care coordination, and hospice for advanced stages.Key Medicare Coverage for Dementia Care:

Medicare Part B (Medical Insurance): Covers doctor visits, cognitive assessments, and some outpatient therapy.

Medicare Home Health Care (Part A or B): Covers skilled nursing or therapy (Physical, Occupational, Speech) if the patient is homebound and needs part-time, intermittent care.

Medicare Advantage (Part C): These private plans often provide extra benefits, such as in-home support, respite care, and meal delivery.

Special Needs Plans (SNPs): Specialized Advantage plans designed for people with specific chronic conditions, including dementia.

GUIDE Model: A new Medicare program that provides care navigation and supports caregivers, aiming to help seniors stay in their homes longer.

Hospice Care: Covered by Part A for patients with a terminal prognosis of 6 months or less, which can include in-home care.

The GUIDE program does not replace 24/7 supervision, but it adds a layer of coordinated support that can be transformative for families trying to hold everything together. Access requires a participating provider enrolled in the GUIDE model, so it is not something every Medicare beneficiary can automatically use. The program is still expanding, and availability varies by location.

5. Understand the Hospice Option for Advanced Alzheimer's

This is the strategy most families do not expect to hear about. Alzheimer's disease is a terminal condition, and when it reaches advanced stages, Medicare Part A hospice benefits can unlock in-home care that would otherwise be unavailable.

Can Medicare help cover in-home care for dementia patients who wander or need supervision 24/7?

While Medicare does not cover nursing homes, memory care centers, or in home caregivers, there can be coverage through Part A under hospice benefits. Because Alzheimer's Disease is a terminal condition, Medicare will cover hospice care in advanced stages.Hospice under Medicare covers nursing care, aide services, medications related to the terminal diagnosis, medical equipment, and crucially, respite care for family caregivers (up to five consecutive days in an inpatient facility so the family can rest). A physician must certify a life expectancy of six months or less, but for patients in advanced stages of Alzheimer's who have lost the ability to walk, speak, or perform daily activities, this certification is often appropriate.

Hospice can add significant support, including nursing, aide services, equipment, medications, and respite, but families may still need to arrange private or Medicaid-covered supervision for hours hospice does not cover. It is not a blanket 24/7 home aide benefit.

Hospice does not mean giving up on the patient. It means shifting the focus to comfort, dignity, and family support. And unlike every other coverage option on this list, Medicare Part A covers hospice regardless of whether you have Original Medicare or a Medicare Advantage plan.

6. Check VA Aid and Attendance Benefits

For veterans and their surviving spouses, the VA Aid and Attendance pension can provide monthly payments specifically to help cover the cost of in-home caregivers, assisted living, or nursing home care. Agents who serve veteran clients flag this benefit consistently.

The benefit is income- and asset-based, and the application process can take time. Contacting your regional VA office or a Veterans Service Organization (VSO) well before the need becomes urgent gives you the best chance of having the benefit in place when you need it.

7. Buy Long-Term Care Insurance Before You Need It

Long-term care insurance comes up in nearly every dementia-related agent answer, but with one consistent caveat: you have to buy it before the diagnosis. Once someone has been diagnosed with dementia or Alzheimer's, no carrier will issue a policy. That door closes permanently.

For families already past that point, the options narrow to Medicaid, private pay, or spending down assets until Medicaid eligibility kicks in. For anyone reading this before a diagnosis hits their family, agents are clear that buying long-term care coverage while you are healthy enough to qualify is the single most impactful financial decision you can make.

Alternatives do exist for people who cannot qualify for or afford traditional long-term care coverage. Short-term care policies cover a limited benefit period (typically up to a year) and are often available with simplified underwriting. Annuities with long-term care riders are another option agents mention, combining a savings vehicle with care coverage.

Are caregivers or home health aides included for dementia care?

Now, it's not really covered by Medicare. Is home health covered? Home health aides are, but it's tied in with home health on the medical side. On the non-medical side, just caregivers coming in and helping, that's not covered. So that's usually covered by Medicaid or private pay. If you have long-term care insurance, some advantage plans have a little bit of time built in, but not a lot. Eighty hours a year is not a big chunk, not when you need help every day.

I hope that helps. Give us a call if you have any other questions.

8. Build the Family Patchwork

When the programs run out and the insurance does not cover the gap, families do what Mary Turner and her sister did: they coordinate. They take shifts. They pool resources. They hire private caregivers for the hours nobody in the family can cover. They spend down savings until Medicaid kicks in.

It is not a clean system. Agents acknowledge that openly. But there are resources that reduce the burden:

- Adult day care programs provide supervised activities during daytime hours, giving family caregivers a reliable daily break

- Area Agencies on Aging (reachable through the Eldercare Locator at 1-800-677-1116) connect families with local respite care, support groups, and caregiver training

- PACE programs offer comprehensive medical and social services for people who qualify for both Medicare and Medicaid, often allowing them to remain at home

- Caregiver training through Medicare, which covers training for family members when the type of care requires it

Each state runs its own Medicaid programs with different eligibility rules and benefit packages, and programs like PACE are not available everywhere. The specifics matter, and they change based on where you live.

Start With the Right Resources

Every strategy on this list depends on what is available where you live. C-SNP plans, HCBS waivers, PACE programs, and the GUIDE model all vary by state and county. If you are navigating this for a loved one, start with your local Medicaid office, your Area Agency on Aging (reachable at 1-800-677-1116), and your regional VA office if applicable. These agencies can connect you with programs specific to your area.

From there, a local Medicare agent who understands long-term care realities and your county's plan landscape can help map out which Medicare-side options, like C-SNPs, GUIDE, and hospice, apply to your family's situation, at no cost to you. And if you are not there yet but see it on the horizon, the time to plan is now, while options like long-term care insurance and Medicaid planning are still available.