Bipolar at 66: The 190-Day Psychiatric Lifetime Cap and the C-SNP Most Agents Skip

-

February 19, 2026

A bipolar diagnosis at 66 changes the Medicare conversation. Not because coverage is bad. Medicare actually covers psychiatric care, therapy, and medications more broadly than most people expect. But three specific rules sit underneath that coverage that almost nobody talks about, and they can make the difference between a plan that works for you and one that quietly fails when you need it most.

Those three rules: a hard lifetime cap on inpatient psychiatric hospital stays, a special plan type designed for chronic conditions like bipolar that you can enroll in outside the normal enrollment window, and a federal mandate that forces every Part D drug plan to cover the psychiatric medications you're most likely to need. Out of 35 licensed Medicare agents who answered a question about structuring coverage for bipolar disorder on Medicare Agents Hub, fewer than a third mentioned any of these. That gap is what this article is about.

If you are searching for whether Medicare covers bipolar disorder, the answer is yes. But the details depend on where you receive care, which plan type you choose, and how your medications are covered. Here is what matters most.

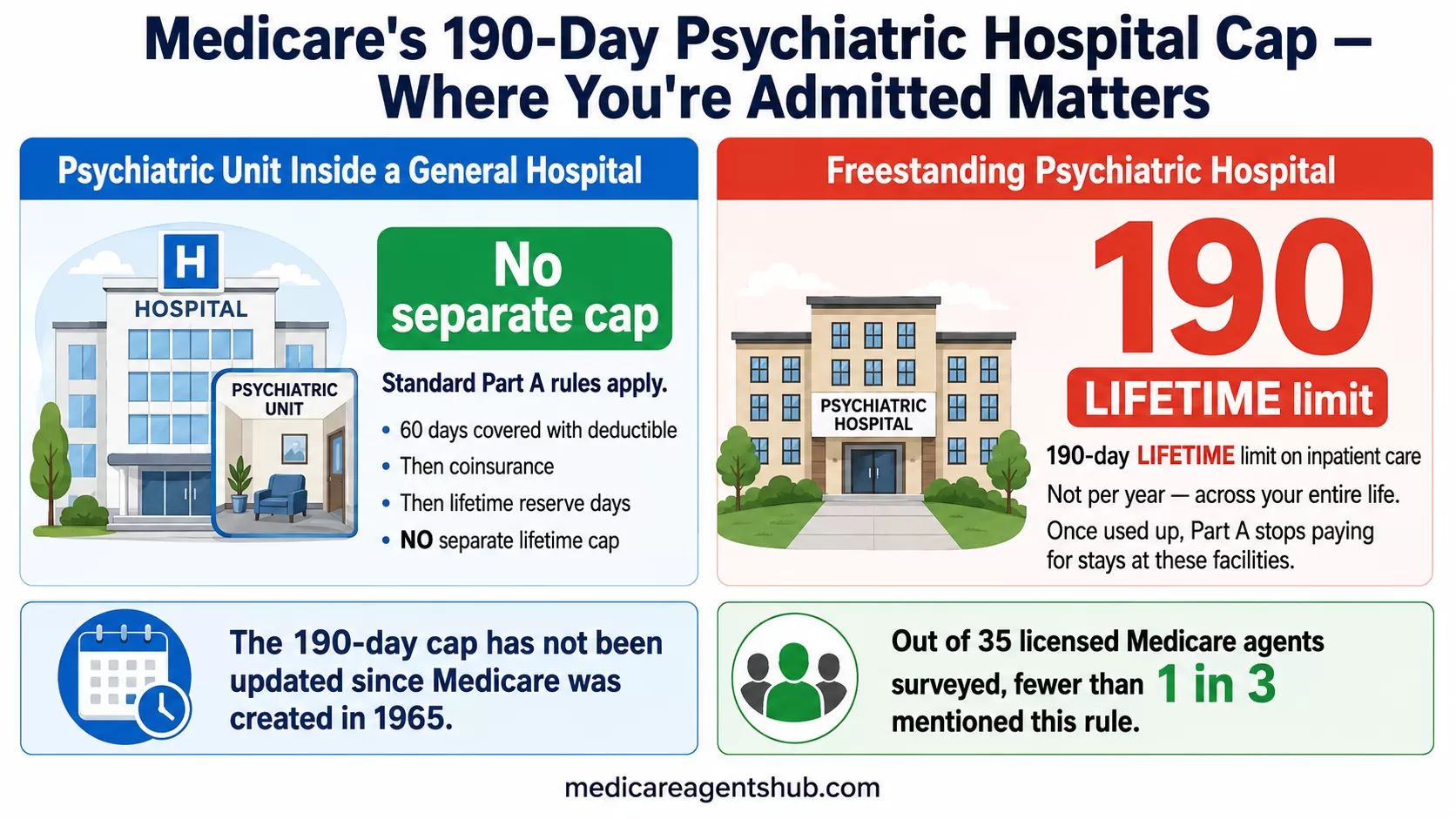

The 190-Day Lifetime Cap on Psychiatric Hospital Stays

Medicare Part A covers inpatient mental health care. That part is straightforward. What's not straightforward is the distinction between where you receive that care.

If you're admitted to a psychiatric unit inside a general hospital, Part A covers the stay the same way it covers any other inpatient admission. The standard benefit periods apply (60 days covered with a deductible, then coinsurance kicks in, then lifetime reserve days). There is no separate lifetime cap.

If you're admitted to a freestanding psychiatric hospital, a completely different rule applies. Medicare Part A imposes a 190-day lifetime limit on inpatient care in these facilities. That's not 190 days per year. It's 190 days across your entire life on Medicare. Once those days are used, they're gone.

Licensed agent Justin Fox, based in Montana, put it plainly when advising a senior with bipolar disorder: Part A covers inpatient mental health care, but "it is however limited to 190 days lifetime." Agent Cheryl Lyons in Indiana broke it down further in a separate response, noting that "Medicare caps lifetime inpatient psychiatric hospital days at 190 days" and emphasizing that "this limit does not apply to general hospitals."

This distinction matters for bipolar disorder specifically because acute manic or depressive episodes can require inpatient stabilization, sometimes more than once. If your treatment happens in a standalone psychiatric facility, each day counts against that 190-day bank. If the same treatment happens in a general hospital's psychiatric wing, it doesn't.

What Happens After Day 190

Agent Misty Bolt in Tennessee was blunt about it: "They cover 190 days lifetime. Which means there is no more coverage after you have used all 190 days." After the cap, Medicare Part A stops paying for inpatient psychiatric hospital care entirely. You would need to rely on other coverage sources, Medicaid if you qualify, a Medicare Advantage plan's additional benefits, or private resources.

The reality is that most people with bipolar disorder will never come close to 190 days. Outpatient care, medication, and periodic therapy handle the vast majority of cases. But for those with treatment-resistant episodes, co-occurring substance use disorders, or conditions requiring extended stabilization, the cap can become a real crisis point. It's a number worth knowing early, not after days have already been spent.

The following responses come from licensed Medicare insurance agents who answered real consumer questions on Medicare Agents Hub.

I've been diagnosed with bipolar disorder at age 66. How should I structure my Medicare coverage to ensure I get the mental health care I need?

Here is how to structure your 2026 coverage for maximum support:1. The Outpatient Strategy: Therapy & Psychiatry

Bipolar disorder typically requires regular visits with a psychiatrist (for medication management) and a therapist.

The Original Medicare + Medigap Route (Highly Recommended): If you choose Original Medicare with a Medigap Plan G, you pay your Part B deductible ($283 in 2026), and after that, your therapy and psychiatry visits are generally $0 out-of-pocket. This is ideal because there is no limit on the number of sessions as long as they are medically necessary.

The Medicare Advantage Route: These plans often have lower monthly premiums but require copays for every mental health visit (often $25–$50). If you see a therapist weekly, these costs can add up to more than a Medigap premium. Also, check that your preferred mental health providers are "in-network," as many therapists do not join Advantage networks.

2. The Medication Strategy: Part D

Medicare Part D (Drug Plans) must follow "protected class" rules. This means every plan is legally required to cover substantially all antipsychotic and antidepressant medications.

2026 Drug Cap: Starting this year, there is a $2,100 annual out-of-pocket cap on all Part D drugs. If you are prescribed expensive brand-name mood stabilizers, you will never pay more than $2,100 in a year for your prescriptions.

The "Medicare Prescription Payment Plan": In 2026, you can opt into a program that allows you to spread that $2,100 out over the year in monthly installments rather than paying a large amount at the pharmacy counter all at once.

3. Inpatient "Lifetime Limit" Warning

It is important to be aware of a specific Medicare quirk regarding inpatient psychiatric care:

The 190-Day Limit: Medicare Part A covers inpatient mental health care, but if you are treated in a specialized psychiatric hospital (rather than a psychiatric unit within a general hospital), there is a 190-day lifetime limit.

C-SNPs for Bipolar Disorder: The Plan You Can Join Any Time of Year

Most Medicare enrollment happens during fixed windows. The Annual Enrollment Period runs October 15 through December 7. Miss it, and you're generally locked into your current plan until the next cycle.

Chronic Condition Special Needs Plans, called C-SNPs, are an exception. These are a category of Medicare Advantage plan designed specifically for people with certain chronic conditions. Bipolar disorder is one of the qualifying diagnoses. And if you qualify, you can enroll in a C-SNP at any time during the year.

Agent Jim Carroll in Florida, who specializes in Special Needs Plans, laid out the specifics: "Bipolar Disorder is one of the 15 Specific Chronic Conditions under the Centers for Medicare and Medicaid Services (CMS) Chronic Condition Special Needs Plans (C-SNP)." He emphasized that "anyone eligible for a C-SNP can enroll at any time of the year."

I've been diagnosed with bipolar disorder at age 66. How should I structure my Medicare coverage to ensure I get the mental health care I need?

Bipolar Disorder is one of the 15 Specific Chronic Conditions under the Centers for Medicare and Medicaid Services (CMS) Chronic Condition Special Needs Plans (C-SNP).A C-SNP is a Special Needs Medicare Advantage (MA) Plan. Original Medicare Part A and Part B only cover 20% of medical costs. A C-SNP MA plan is designed to provide additional benefits to meet the chronic needs of its members.

This is why it's wise to have a Nationally Licensed Health Insurance Broker who is a Medicare Special Needs expert do a Health Risk Assessment with you. They will be able to find the best C-SNP plan in your area that will meet your health and financial needs. Although January 1 through March 31 is Medicare Open Enrollment, when people can change from one MA plan to another, anyone eligible for a C-SNP can enroll at any time of the year.

Once someone is enrolled into a C-SNP, all that's needed to finalize the enrollment if for the doctor who diagnosed and is providing treatment for the chronic condition to complete a verification form of said diagnosis/treatment within 30 days of the enrollment. Otherwise, CMS will decline the enrollment.

The 30-Day Verification Form

Enrolling in a C-SNP isn't as simple as checking a box. There's a verification step that trips people up. Carroll explained it: "Once someone is enrolled into a C-SNP, all that's needed to finalize the enrollment is for the doctor who diagnosed and is providing treatment for the chronic condition to complete a verification form of said diagnosis/treatment within 30 days of the enrollment. Otherwise, CMS will decline the enrollment."

That 30-day window is firm. If your doctor doesn't complete the Chronic Condition Verification (CCV) form in time, you get disenrolled. On a related question about C-SNP disenrollment, agent Janix Barbosa-LLanos in New Mexico confirmed that being disenrolled for not submitting the CCV "triggers a Special Enrollment Period" to enroll in another plan. So you're not stranded, but you've lost time and continuity of care.

The practical move: talk to your psychiatrist or diagnosing physician before you enroll. Confirm they're willing and able to complete the form quickly. Have the conversation before you sign anything.

What C-SNPs Actually Offer

C-SNPs are structured to coordinate care for the specific condition you qualify under. For a bipolar-qualifying C-SNP, that typically means:

- A care coordinator assigned to help manage your treatment plan

- Formularies designed around the medications commonly prescribed for your condition

- Provider networks built with behavioral health access in mind

- Lower or $0 copays for condition-related services in many plans

One thing to know: not every county has a bipolar-specific C-SNP. Some areas offer broader 'chronic condition' SNPs that cover multiple qualifying diagnoses, including bipolar disorder, under a single plan. These still qualify and still provide coordinated care -- the name on the plan may just be more general than you'd expect. Check what's available in your specific county before assuming nothing exists.

Agent Sam Deter in Missouri recommended this as the starting point for anyone with bipolar disorder on Medicare: "The first step would be to determine if there is a C-SNP for bipolar disorder in your area that includes any providers you are not willing to change."

That last part matters. C-SNPs are Medicare Advantage plans, which means they come with provider networks. If your current psychiatrist, therapist, or prescribing physician isn't in the C-SNP's network, you may need to weigh the plan's benefits against the disruption of switching providers. Not every area has a C-SNP available for mental health conditions, either. Availability varies by county and by year.

The care coordination piece is worth emphasizing. In a standard Medicare Advantage plan, your psychiatrist, therapist, and primary care doctor may operate in silos. A C-SNP is built to connect them -- your care coordinator tracks your treatment plan across providers and can flag gaps before they become problems. For a condition like bipolar disorder where medication changes, therapy adjustments, and crisis planning all need to stay in sync, that coordination has real clinical value.

Protected Drug Classes: Why Every Part D Plan Must Cover Your Medications

Part D drug plans have significant discretion over which medications they cover. A plan can decide not to cover a particular blood pressure medication, or a specific cholesterol drug, as long as it covers at least two drugs in each therapeutic category. But there are six drug classes where that discretion goes away.

Medicare designates six "protected classes" where Part D plans must cover substantially all available medications. Three of those six are directly relevant to bipolar disorder treatment:

- Antipsychotics (used for manic episodes and mood stabilization)

- Antidepressants (used for depressive episodes)

- Anticonvulsants (many double as mood stabilizers, like valproate and lamotrigine)

The other three protected classes are immunosuppressants, anticancer drugs, and HIV/AIDS treatments.

Can a drug plan drop one of my medications during the middle of the year?

Yes, Medicare prescription drug plans ( Part D) can remove drugs from their formulary or changed their coverage rules through out the year. The plan can drop a medication or move it to a higher, more expensive tier. They must provide the consumer a 30 day notice. Plans may also add restrictions like prior authorization or quantity limited.There are protected drug classes that drug plans must cover medications, Those six protected classes are immunosuppressants, antidepressants, antipsychotics, anticancer, anticonvulsants and HIV/Aids treatments.

If a plan stops covering your medication, you can appeal the decision or request an exception through your plan's formal process.

Agent Nicholas Depke in Nebraska explained why this matters practically: antidepressants and related psychiatric medications "actually fall into a protected drug class under Medicare Part D, which means plans are required to cover substantially all medications in that category. This is good news for beneficiaries who rely on these prescriptions because it offers stronger protections compared to other drug categories where plans have more flexibility to limit coverage."

The Prior Authorization Catch

"Substantially all" doesn't mean "no questions asked." Agent Janix Barbosa-LLanos in New Mexico flagged an important nuance: even within protected classes, plans can still apply "prior authorization, step therapy, and quantity limits." In practice, this means your plan might require your doctor to submit paperwork before approving a specific antipsychotic, or it might require you to try a generic alternative before covering a brand-name mood stabilizer.

The protection is that the plan can't simply exclude the medication from its formulary the way it could with drugs in non-protected classes. But it can add hoops. If you're switching Part D plans, check whether your current medications require prior authorization on the new plan's formulary. Your pharmacist can usually tell you this before you enroll.

The $2,100 Out-of-Pocket Drug Cap

Starting in 2025, Medicare Part D includes a hard annual cap on out-of-pocket drug spending. In 2026, that cap is $2,100. Once you hit it, your plan covers the rest for the remainder of the year. For someone taking brand-name mood stabilizers, atypical antipsychotics, or newer-generation anticonvulsants, this cap can be the difference between manageable costs and financial stress.

On top of that, the Medicare Prescription Payment Plan lets you spread that $2,100 across monthly installments instead of paying large amounts at the pharmacy counter when you fill prescriptions early in the year. If your psychiatric medications put you near the cap, opting into this payment plan can smooth out the financial hit.

Extra Help for Low-Income Beneficiaries

Many people with serious mental illness qualify for Medicare's Extra Help program (also called the Low-Income Subsidy or LIS). Extra Help pays for part or all of your Part D premiums, deductibles, and copays. If you qualify, your out-of-pocket drug costs drop dramatically -- in many cases to a few dollars per prescription.

The income limits are higher than most people expect, and the application is straightforward through Social Security. If you're taking multiple psychiatric medications and the costs are adding up even with the $2,100 cap, checking your eligibility for Extra Help should be one of your first moves.

The Weekly Therapy Math: Medigap vs. Medicare Advantage

Bipolar disorder typically requires ongoing outpatient care: regular visits with a psychiatrist for medication management, and often weekly or biweekly sessions with a therapist. The cost structure for these visits differs sharply depending on whether you're on Original Medicare with a Medigap plan or a Medicare Advantage plan.

Agent Annette Newman in California ran the comparison in her answer about structuring bipolar coverage. On the Original Medicare + Medigap Plan G route: "You pay your Part B deductible ($283 in 2026), and after that, your therapy and psychiatry visits are generally $0 out-of-pocket. This is ideal because there is no limit on the number of sessions as long as they are medically necessary."

On the Medicare Advantage route: "These plans often have lower monthly premiums but require copays for every mental health visit (often $25 to $50)." Those copays compound fast with weekly therapy.

Running the Numbers

Here's what that looks like over a year for someone seeing a therapist weekly and a psychiatrist monthly:

| Cost Category | Original Medicare + Medigap G | Medicare Advantage (Typical) |

|---|---|---|

| Part B deductible | $283/year | $0 (often waived) |

| Weekly therapy (52 visits) | $0 after deductible | $25-$50/visit = $1,300-$2,600/year |

| Monthly psychiatrist (12 visits) | $0 after deductible | $30-$50/visit = $360-$600/year |

| Medigap premium | ~$150-$250/month = $1,800-$3,000/year | N/A |

| MA plan premium | N/A | $0-$50/month = $0-$600/year |

| Estimated annual total | $2,083-$3,283 | $1,660-$3,800 |

The key difference is predictability. With Medigap, your costs are fixed after the deductible. With Medicare Advantage, they scale with usage -- and bipolar disorder means usage can spike during mood episodes.

Agent Kevin Chaikin in Virginia made a related point: "Original Medicare with a supplement is generally going to cover more mental health providers than Medicare Advantage and can reduce copays if you see a therapist regularly." Provider access is the other variable. Newman noted that "many therapists do not join Advantage networks," which can limit your choices on an MA plan.

Medigap.

Intensive Outpatient Programs: The Coverage Between Therapy and the Hospital

Bipolar disorder doesn't always fit neatly into "weekly therapy" or "inpatient stay." Sometimes the right level of care is something in between. Intensive Outpatient Programs (IOPs) fill that gap, and Medicare Part B covers them.

Agent Mark Boone in Minnesota described IOPs as covering "more than 9 hours of weekly therapeutic services, acting as a bridge between weekly therapy and inpatient care. Services, which include group/individual therapy and medication management, are covered at 80% of the Medicare-approved amount."

Agent John Becker in Wisconsin added context on when IOPs became more clearly defined in Medicare: "As of January 2024, IOPs are specifically covered under Part B as a level of care between traditional therapy and inpatient treatment."

After you meet the Part B deductible ($283 in 2026), Medicare pays 80% and you pay 20% coinsurance. A Medigap plan would cover that 20%. On a Medicare Advantage plan, you'd pay whatever copay or coinsurance the plan specifies for outpatient mental health services.

IOPs can be delivered at hospitals, Community Mental Health Centers, Federally Qualified Health Centers, and Rural Health Clinics. If you're on a Medicare Advantage plan, make sure the IOP facility is in-network before starting treatment.

It's also worth noting that Medicare covers telehealth visits for mental health care, including telepsychiatry. For medication management appointments and some therapy sessions, you may not need to travel to a provider's office. This can be especially useful during depressive episodes when leaving the house feels impossible, or if behavioral health providers are limited in your area.

Bipolar Medicare Coverage Checklist

Use this checklist when comparing Medicare plans for bipolar disorder coverage:

- Are my psychiatrist and therapist in-network?

- Are my medications covered by my Part D or MAPD plan?

- Do any of my medications require prior authorization or step therapy?

- Is there a C-SNP in my county for my condition?

- Will my doctor complete the C-SNP verification form within 30 days?

- Are local inpatient options freestanding psychiatric hospitals or general hospital psych units?

- What would weekly therapy cost under this plan?

- Have I checked the Part D formulary tiers and not just whether the drug is listed?

- Am I eligible for Extra Help / Low-Income Subsidy to reduce drug costs?

- Does the plan offer telehealth options for psychiatry and therapy visits?

Putting This Together: A Decision Framework

If you've been diagnosed with bipolar disorder at 65 or older, here's a structured way to think through your Medicare coverage decisions:

Step 1: Check for C-SNPs in your area. Go to Medicare's plan finder or work with an agent who specializes in Special Needs Plans. If a C-SNP is available and includes your current providers, it may offer the most coordinated care. Remember, you can enroll any time of year, but your doctor must complete the verification form within 30 days.

Step 2: If no C-SNP fits, compare Medigap vs. Medicare Advantage using your actual utilization. If you're seeing a therapist weekly and a psychiatrist monthly, do the annual math with real copay numbers from plans in your area. Don't compare premiums alone. For a full breakdown of what to weigh, see our guide to Medicare mental health benefits.

Step 3: Run your medications through each Part D formulary. Check not just whether your drugs are covered, but what tier they're on and whether prior authorization is required. The protected class rules guarantee coverage, but tier placement determines what you pay.

Step 4: Understand the 190-day inpatient psychiatric cap. If there's any possibility of needing inpatient stabilization, ask your treatment team whether your local options are freestanding psychiatric hospitals or psychiatric units within general hospitals. The difference determines whether your days count against the lifetime cap.

Step 5: Review annually. Plan formularies, networks, and copay structures change every year. A plan that covers your medications well this year might shift a key drug to a higher tier next year. The Annual Enrollment Period exists for exactly this kind of review.

Need help sorting through these options? Find a licensed Medicare agent in your area who understands chronic condition coverage. Ask them to review your current providers, run your prescriptions through plan formularies, and check whether a C-SNP is available in your county. A 15-minute conversation with the right agent can save you thousands in unexpected costs and keep your treatment plan intact.

Bipolar disorder adds complexity to Medicare planning, but the tools to manage it are built into the system. The 190-day cap, C-SNP eligibility, protected drug classes, and Extra Help are the specific mechanisms that determine whether your coverage actually works for your condition. Knowing they exist is the first step. The next step is finding an agent who knows how to use them.

Frequently Asked Questions

Does Medicare cover bipolar disorder treatment?

Yes. Medicare Part A covers inpatient psychiatric care, Part B covers outpatient therapy and psychiatrist visits, and Part D covers psychiatric medications. The specifics of what you pay depend on your plan type, provider network, and drug formulary.

Does Medicare cover inpatient psychiatric care?

Medicare Part A covers inpatient mental health treatment. If you are admitted to a psychiatric unit inside a general hospital, standard Part A rules apply. If you are admitted to a freestanding psychiatric hospital, a separate 190-day lifetime limit applies.

What is Medicare's 190-day psychiatric hospital limit?

Medicare Part A limits inpatient care in freestanding psychiatric hospitals to 190 days over your lifetime. This limit does not apply to psychiatric units within general hospitals. Once the 190 days are used, Part A stops paying for freestanding psychiatric hospital stays.

Can someone with bipolar disorder qualify for a C-SNP?

Yes. Bipolar disorder is one of the 15 chronic conditions that qualifies for a Chronic Condition Special Needs Plan. C-SNPs are a type of Medicare Advantage plan designed to coordinate care for your specific condition, and you can enroll at any time of year. Your doctor must complete a verification form within 30 days of enrollment.

Do Medicare drug plans have to cover bipolar medications?

Antipsychotics, antidepressants, and anticonvulsants are all federally protected drug classes under Medicare Part D. Plans must cover substantially all medications in these categories. However, plans can still require prior authorization, step therapy, or quantity limits.

Is Medigap or Medicare Advantage better for mental health care?

It depends on how often you use mental health services. Medigap offers more predictable costs if you see a therapist weekly, since most visits are covered at $0 after the Part B deductible. Medicare Advantage may have lower premiums but charges copays per visit, which add up with frequent appointments. C-SNPs, a type of Medicare Advantage plan, may offer better coordination and lower costs for qualifying conditions like bipolar disorder.

What is Medicare Extra Help and do I qualify?

Extra Help (also called the Low-Income Subsidy) is a federal program that helps pay Part D premiums, deductibles, and copays. Many people with serious mental illness qualify. Income limits are higher than most people expect. You can apply through Social Security or check eligibility at Medicare.gov.