Grandma Should Not Have To Be a Pharmacist: Where Did the Part D Help Go?

Every year during Medicare enrollment season, I sit across from and spend hours on the phone with seniors who are overwhelmed, confused, and honestly scared about making the wrong decision with their prescription drug coverage. I have had seniors tell me that agents won't return their phone call when they find out they want to speak about Part D. And lately, I've been seeing a dangerous trend grow inside the Medicare industry. Medicare Advantage companies are increasingly choosing not to compensate agents for helping beneficiaries and to be honest it was nominal to begin with but It did at least cover the cost of the couple hours it takes to compare and enroll in standalone Medicare Part D prescription drug plans.

To most people, that may sound like an industry issue and that it's not a big deal. But for seniors, it has very real consequences. Because when companies stop paying agents to help people navigate Part D plans, one of three things usually happens:

- Agents stop helping with Part D altogether because they simply cannot afford to spend hours doing unpaid work, and I personally know of several who simply tell them to go to Medicare.gov and figure it out. Or,

- Beneficiaries get steered toward plans that do pay compensation, even if those plans are more expensive or not the best fit.

- They set them in a plan and forget it. Meaning each year as the formulary changes they do not review their drugs or plan and leave them to roll over into the same plan year after year.

None of these outcomes serve the senior.

What's the biggest mistake seniors make when choosing a Medicare Part D plan?

The Biggest mistake that people make with part D is not reviewing it annually.Cost per company and Formulary teirs change every year.

You may be paying for more than you need to without an annual review.

How Big of a Problem Is Medicare Part D?

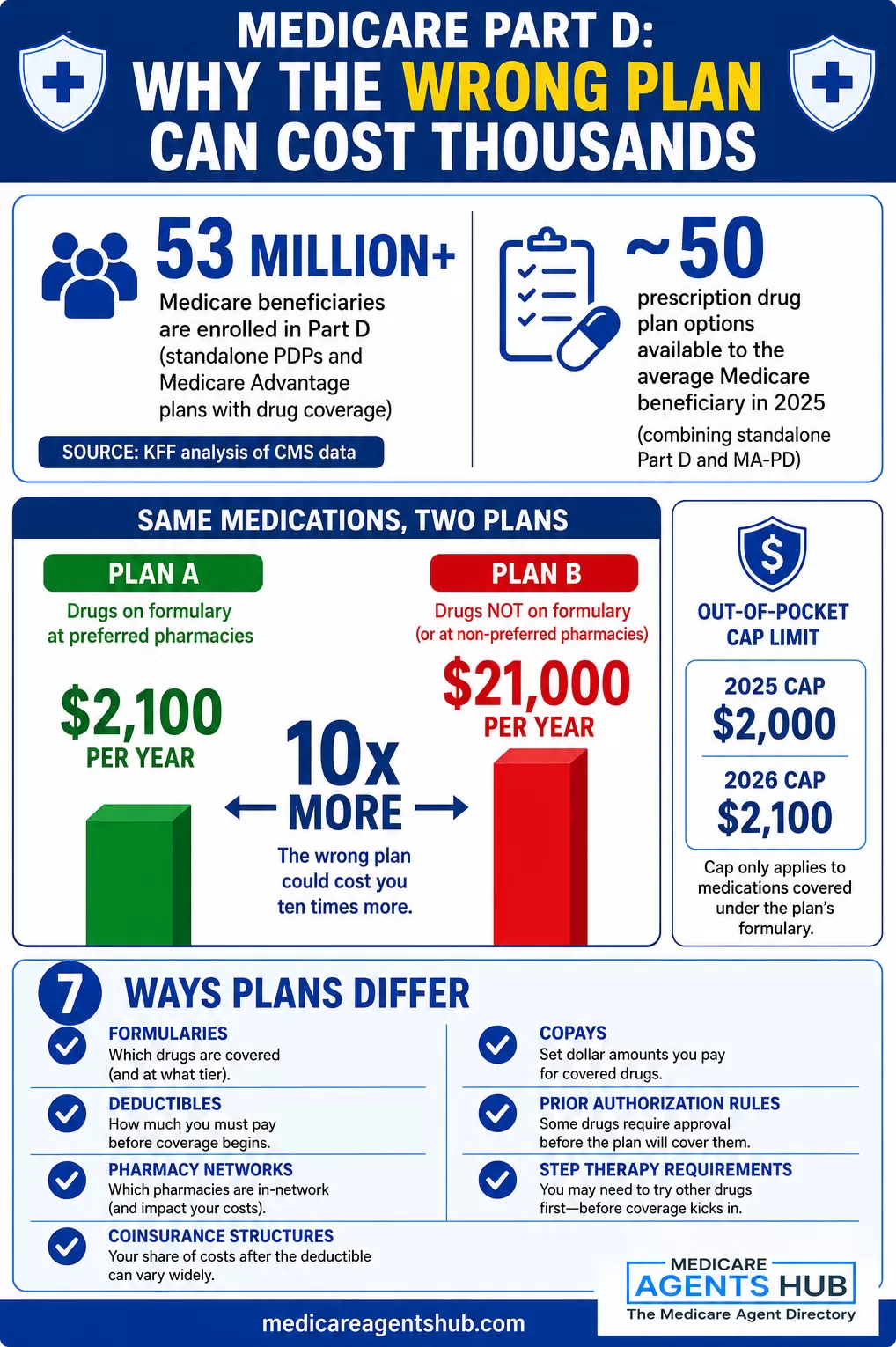

According to KFF (The Kaiser Family Foundation) analysis of CMS data, more than 53 million Medicare beneficiaries are enrolled in Medicare Part D plans, including both standalone prescription drug plans and Medicare Advantage plans with prescription coverage.

In 2025, the average Medicare beneficiary has access to nearly 50 prescription drug plan options when combining standalone Part D and Medicare Advantage drug coverage.

Every one of those plans has different:

- Formularies

- Deductibles

- Pharmacy networks

- Copays

- Coinsurance structures

- Prior authorization rules

- Step therapy requirements

These details matter. One of these mistakes could cost thousands of dollars a year, two could be life threatening.

One Wrong Decision Can Cost Thousands

Very often I see situations where two plans covering the exact same medications can differ by thousands of dollars annually in estimated drug costs. In fact, one plan could have a cost of $2,100 a year and the same medications could end up costing $21,000 a year if not in formulary.

CMS implemented major changes to Medicare Part D under the Inflation Reduction Act, including an annual out-of-pocket cap on covered prescription drugs:

- 2025 cap: $2,000

- 2026 cap: $2,100

While this is a meaningful protection for seniors, it only applies to medications that are properly covered under the plan's formulary or approved through exceptions and coverage rules. Many seniors are just not aware of these differences and only find out after they are locked in for the year. Like with Medicare advantage after March 31st in most cases seniors are not able to change their plan until January 1st of the following year.

If a drug is excluded, not covered, or denied without successful appeal, beneficiaries can still face significant out-of-pocket exposure outside of that protection. Most seniors are not equipped to navigate those rules alone. One client told me "I am so thankful you were able to help us we have been trying to figure this out for weeks", Incidentally she had called me at 8pm on December 7th and I worked with her for over an hour to straiten out her coverage.

That is why proper Part D guidance matters.

There Is a Human Cost to Making a Poor Choice

This is not just about insurance paperwork. It affects people's health every day.

I have personally seen seniors:

- Skip doses to make medications last longer

- Split pills because they cannot afford refills

- Stop taking medications entirely

- Switch to cheaper drugs that are less effective

- Delay treatment because coverage was denied

Research consistently shows that higher prescription drug costs are associated with medication non-adherence, especially among patients with chronic or complex conditions. When seniors stop taking medications properly, their health declines. Blood pressure rises. Diabetes becomes uncontrolled. COPD worsens. Heart conditions become unstable. Hospitalizations increase.

Many of these situations could have been avoided with better plan guidance during enrollment.

When should my plan be reviewed?

It is a good practice to review your plan yearly. Many things change from the drugs you take, the formulary, the doctor networks, and even the hospitals that accept your coverage.That is, if you have Medicare Advantage, it is equally important to look at the costs of premium increases on Medicare supplement insurance policies. All policies are equal; they are standardized.

So the premium is the only real difference.

Agents and Brokers Are the Specialists Seniors Depend On

A good Medicare agent or broker does much more than simply process an enrollment form.

We:

- Compare formularies

- Estimate annual drug costs

- Check pharmacy pricing

- Review provider networks

- Analyze deductibles and coinsurance

- Explain prior authorization requirements

- Help file exceptions and appeals

- Educate beneficiaries on Medicare rules

- Act as an advocate for their patient / client

In many cases, we are the only people taking the time to review the beneficiary's entire healthcare picture before they enroll.

As a Medicare professional, I want to make something very clear: I still provide free, unbiased education and help with Part D plans whether I get paid for it or not.

I believe seniors deserve honest guidance, and I refuse to let compensation determine whether someone gets the help they need. But in reality, is that not everyone in this industry operates that way. And in many cases the agent cannot. After many years in business, I am blessed to have a successful business and can take the time to help people without being paid. Many new agents are struggling to keep the lights on. And simply cannot spend the time needed without being properly compensated.

Some agents simply cannot justify spending hours on unpaid consultations during the busiest enrollment periods of the year. Others may feel pressure to focus on plans that do provide compensation. That leaves seniors vulnerable in a system that is already incredibly difficult to navigate.

The Industry Is Quietly Removing Specialists From the Process

Imagine telling someone to prepare complicated taxes without an accountant, defend themselves in court without an attorney, or purchase a home without a realtor.

Yet increasingly, Medicare beneficiaries are expected to navigate one of the most complex prescription drug systems in the country completely on their own.

The irony is that poor Part D decisions often lead to:

- Higher drug spending

- More medication non-adherence

- Increased medical complications

- More hospital admissions

- Higher long-term healthcare costs

The specialist exists for a reason.

And when you remove trained Medicare professionals from the process, the people hurt most are seniors already struggling with chronic illnesses, fixed incomes, and overwhelming healthcare decisions.

The Pressure to Favor Plans That Pay

There's another uncomfortable truth the industry rarely discusses openly.

When certain products compensate agents and others do not, the system itself creates financial pressure that can influence recommendations.

Most agents genuinely want to help people. I believe that.

But when an agent spends hours helping with a Part D enrollment that pays nothing while another product offers compensation, the industry creates a conflict that should never exist in senior healthcare decisions.

Beneficiaries deserve recommendations based on:

- Their medications

- Their pharmacies

- Their doctors

- Their health conditions

- Their financial situation

Not based on whether the insurance company decided to compensate the professional helping them.

Seniors Deserve Better

CMS data shows that Medicare Advantage enrollment continues to grow rapidly, with more than half of Medicare beneficiaries now enrolled in private Medicare Advantage plans. Even as we speak a large carrier is pulling plans in rural areas as a cost saving effort. Leaving seniors I the middle of the year with yet another choice of what coverage to get.

At the same time, standalone Part D plan availability has been shrinking, with fewer firms offering PDPs and more consolidation in the market.

The Medicare landscape is becoming more complicated, not less.

That means beneficiaries need qualified guidance now more than ever.

As a Medicare agent, I believe seniors deserve:

- Transparent education

- Honest recommendations

- Access to specialists

- Help understanding formularies

- Assistance navigating drug costs

- Advocacy when coverage problems arise

Because when seniors make the wrong Part D decision, they are often the ones who pay the price: physically, emotionally, and financially.

And that is something our industry cannot afford to ignore.

Sources

"Medicare Part D in 2025: A First Look at Prescription Drug Plan Availability, Premiums, and Cost Sharing." KFF, Kaiser Family Foundation, 2025, https://www.kff.org/medicare/issue-brief/medicare-part-d-in-2025-a-first-look-at-prescription-drug-plan-availability-premiums-and-cost-sharing/. Accessed 10 May 2026.

"Key Facts About Medicare Part D Enrollment, Premiums, and Cost Sharing." KFF, Kaiser Family Foundation, 2025, https://www.kff.org/medicare/issue-brief/key-facts-about-medicare-part-d-enrollment-premiums-and-cost-sharing-in-2025/. Accessed 10 May 2026.

"Medicare Prescription Drug Inflation Reduction Act Implementation." Centers for Medicare & Medicaid Services, CMS.gov, https://www.cms.gov/. Accessed 10 May 2026.

"Medicare Advantage and Medicare Prescription Drug Programs Remain Stable as CMS Implements Improvements for 2025." Centers for Medicare & Medicaid Services, CMS.gov, 27 Sept. 2024, https://www.cms.gov/newsroom/press-releases/medicare-advantage-medicare-prescription-drug-programs-remain-stable-cms-implements-improvements. Accessed 10 May 2026.

Wingrove, Josh. "US Medicare Says Part D, Advantage Premiums Will Fall in 2025." Reuters, 27 Sept. 2024, https://www.reuters.com/business/healthcare-pharmaceuticals/us-medicare-says-part-d-advantage-premiums-will-fall-2025-2024-09-27/. Accessed 10 May 2026.

About the Author: William Gray, also known as "The Medicare Dude," is a Medicare insurance professional, educator, and advocate specializing in Medicare Advantage, Medicare Supplement, and Medicare Part D prescription drug coverage. He is recognized for helping Medicare beneficiaries understand complex healthcare decisions through clear, unbiased education and hands-on guidance. William works directly with seniors to compare Medicare options, analyze prescription drug costs, and avoid costly enrollment mistakes. His focus is on transparency, education, and protecting beneficiaries from unnecessary financial and medical risk.