Why Working with a Local Independent Insurance Agent Can Make All the Difference with Medicare

If you’re turning 65 or becoming eligible for Medicare, you’ve probably been exposed to a barrage of information – TV commercials, online ads, a mailbox full of “junk”, phone calls, all promoting the “best” plan. While the volume of information is overwhelming, the reality is that Medicare decisions are important, personal, and often more complex than the advertising suggests.

One of the most important decisions you’ll make when transitioning to Medicare isn’t just which plan to choose, but HOW you choose it. Specifically, should you enroll on your own by calling an insurance company directly or signing up online, or should you work with an independent insurance agent (also called a broker)?

For many Americans, working with an independent insurance agent provides clarity, confidence, and long-term value, at no additional cost. Understanding why can help you make a more informed Medicare decision.

A Common Misconception about Medicare Enrollment

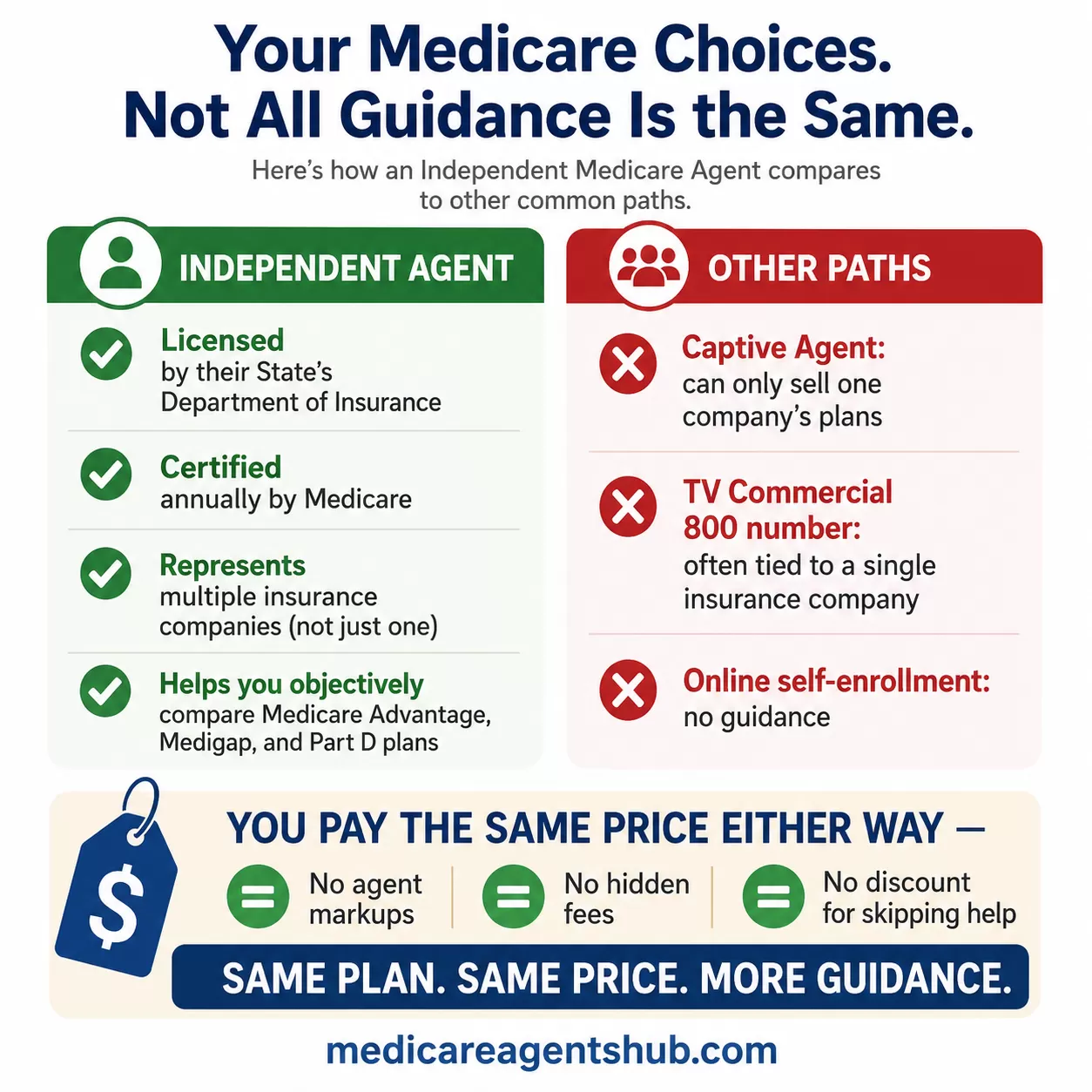

A question many people ask is: “If I can buy the same Medicare plan directly from an insurance company, why would I work with an agent?”

The simple answer is: You pay the same price either way, but you may get more guidance and support when you work with an independent agent.

Insurance products and pricing are:

- Regulated by Medicare and State Insurance Departments

- Standardized in many ways

- Priced the same whether you enroll online, over the phone, or through an agent

There are no agent markups, no hidden fees, and no discounts for bypassing professional help. Whether you enroll directly with an insurance company or through an independent agent, your premium and benefits remain the same.

What is an Independent Insurance Agent?

- Licensed by their State’s Department of Insurance

- Certified annually by Medicare

- Represents multiple insurance companies, not just one

- Helps consumers objectively compare Medicare Advantage, Medicare Supplement (Medigap), and Part D plans

This is different from:

- Calling a phone number from a TV commercial (often tied to a single insurance company)

- Working with a “captive” agent who can only sell one company’s plans

- Enrolling online without guidance

Independence matters, especially with Medicare, because no two people have the same health needs, prescription medications, doctors, or financial priorities.

Access to the Same Plans, Plus a Better Perspective

Independent agents have access to the same Medicare plans you see advertised on television, online, or in the mail. These are the same government-regulated plans, with the same benefits and pricing.

The difference is perspective.

An independent agent can:

- Compare multiple insurance companies side-by-side

- Explain meaningful differences beyond the marketing jargon

- Indentify any trade-offs that aren’t obvious in advertisements

- Help you avoid choosing a plan that looks attractive upfront but may not fit long-term needs

Rather than promoting one company’s product, an independent agent helps you understand how different plans work and which ones align best with your priorities.

How do you educate clients who are completely new to Medicare?

Best way to learn about Medicare is from a trusted Medicare advisor, someone who is working to educate you about all the brands and products isn the market. Too many seniors communicate with a particular insurance company which in turn gives that person a lop-sided view of what's available to them. An independent trusted Medicare Advisor can educate you on all your options.Medicare Is Not a “One-Time” Decision

A common assumption is that once you enroll in Medicare, your decision is final. In reality, Medicare is an ongoing process.

Each year:

- Provider networks can change

- Prescription drug formularies can change

- Copays and benefits may adjust

- Premiums can increase or decrease

Independent agents often provide ongoing support, including annual plan reviews to help ensure that your coverage continues to meet your needs as your health, medications, or finances change. Without that review, many people stay in plans that quietly become less suitable over time. There are several key life events when you should consult a Medicare agent, and an annual review is just one of them.

Why Working with a Local Independent Agent Matters

Beyond independence, local experience adds another important layer of value, particularly with Medicare Advantage and Part D prescription drug plans. These plans are built around provider and pharmacy networks that can vary significantly by area. A local agent understands how nearby hospital systems, primary care providers, specialists, and pharmacies participate in different plans, helping beneficiaries choose coverage that aligns with how and where they actually receive care.

Local experience also helps set proper expectations. An experienced agent familiar with the community can explain how referrals, prior authorizations, prescription tiers, and ancillary benefits like dental or vision coverage tend to work in practice, not just how they’re described in marketing materials. This insight can help beneficiaries avoid surprises and get more value from their coverage.

In addition, a local agent is often more accessible and accountable over time. When questions arise about billing, provider access, prescription changes, or annual plan updates, beneficiaries can reach someone who already understands their situation and coverage history. That continuity can be especially valuable as healthcare needs evolve and Medicare plans change from year to year.

Finally, working with a local independent agent supports small businesses and keeps dollars in the local economy. Instead of calling a national 800 number or enrolling through a distant call center, many people appreciate having a knowledgeable, accessible point of contact who understands their community and can provide ongoing support year after year.

Medicare offers many good options, but understanding the differences requires time, context, and experience. Working with an independent insurance agent (especially someone local) gives you access to objective comparisons, ongoing support, and guidance that isn’t tied to a single insurance company. Since costs and benefits are the same whether you enroll directly or with an agent, many people choose professional help to avoid costly mistakes. In the end, informed decisions lead to better coverage and greater peace of mind.

About the Author: Cody Hebden, MBA, CLU, FLMI, is a licensed independent insurance agent with Insurance of the Carolinas, with over 15 years of experience helping individuals navigate the complexities of Medicare. He provides personalized, no-cost guidance on Medicare Advantage, Medicare Supplement (Medigap), and Part D plans, comparing options across multiple carriers to find solutions that fit each person’s unique needs. Cody’s approach centers on education, advocacy, and long-term support to help clients make confident decisions about their healthcare coverage.

Disclaimer: This article was written by Cody Hebden, a licensed insurance agent in North Carolina and South Carolina, and is not affiliated with, endorsed, or authorized by the Social Security Administration, Centers for Medicare and Medicaid Services, or the Department of Health and Human Services. These agencies have not endorsed any content posted in or linked to this article. This article is for people looking for general information about Medicare and looking for information about Supplemental Medicare Insurance, Medicare Advantage plans, or Prescription Drug Plans. Please contact Medicare.gov or 1-800-MEDICARE to get information on all of your options. NOT AFFILIATED WITH OR ENDORSED BY THE GOVERNMENT OR FEDERAL MEDICARE PROGRAM.