Do Medicare Agents Charge a Fee? Here's What Agents Themselves Say

-

July 1, 2026

If you're approaching 65 or helping a parent navigate Medicare, one of the first questions that comes up is whether you'll have to pay someone to help you sort through it all. It's a fair concern. Professional advice usually comes with a price tag.

But Medicare agents are different. We put this question directly to more than 100 licensed agents and brokers listed on Medicare Agents Hub, and their answer was nearly unanimous: you generally should not pay an extra fee for their enrollment help.

Medicare Agents Do Not Charge You a Fee

Out of the dozens of agents who responded to this question, not a single one said they charge clients for enrollment help. The explanation was consistent across the board: agents are paid by insurance companies, not by you.

Multiple agents noted that charging a Medicare beneficiary for enrollment services isn't just uncommon. For Medicare Advantage and Part D plans, Medicare's marketing rules prohibit agents and plans from charging a fee to process your enrollment. Agents and brokers must also be licensed in the state where they do business and follow CMS marketing guidelines. Breaking these rules can result in loss of licensure or plan termination.

How much do agents charge to help clients to enroll

Greetings!Agents typically do not charge you a fee to help enroll in Medicare. Licensed Medicare agents and brokers are paid by the insurance company if you enroll in a plan, and their commission is regulated and built into the plan’s premium. That means you pay the same premium whether you use an agent or enroll directly with the insurance carrier. There is no additional cost for their assistance. An agent can help you compare plan options, review provider networks, check prescription drug coverage, and complete enrollment paperwork to ensure your coverage starts on time and fits your needs.

For Medicare health and drug plans, Medicare's marketing rules say agents and plans may not charge you a fee to process your enrollment, steer you into a particular plan, or give misleading information. That does not mean every agent represents every plan in your area, so it is still smart to ask which carriers they work with before you enroll.

That free service extends beyond enrollment day. Most agents provide ongoing help throughout the year with plan questions, prescription drug issues, claims problems, and annual plan reviews during the Annual Enrollment Period.

How Medicare Agents and Brokers Actually Get Paid

If agents don't charge you, where does their income come from? The answer is straightforward: insurance companies pay agents a commission when you enroll in a plan through them.

These commissions follow a standard structure. There's an initial commission paid when you first enroll, and a smaller renewal commission paid each year you stay on the plan. For Medicare Advantage and Part D, these amounts are regulated by CMS, which publishes plan-level compensation data.

How do Medicare agents and brokers get paid?

Independent Medicare agents and brokers like myself are paid commissions by the insurance companies, not by Medicare itself.There are two main types of payments:

Initial Commission- this is paid when you enroll a new client in a Medicare Advantage, Medigap, or Part D plan. It’s the largest payment an agent receives. The higher initial commission exists because that’s when the agent does the most work, takes on the most risk, and incurs the highest costs. It’s designed to compensate for that front-loaded time and effort.

Renewal Commission- this is a much smaller ongoing payment the agent receives each year the client stays on that plan. Renewals are where agents make most of their long-term income.

Why There’s Little Incentive to Push One Carrier Over Another:

Commissions are largely standardized. Medicare Advantage and Medigap commission rates are very similar across most major carriers. An agent usually makes roughly the same amount whether the client picks Carrier A or Carrier B.

CMS (the government agency that oversees Medicare) sets guidelines on commission amounts to prevent agents from steering clients toward one company just because it pays more.

While there can be small differences between carriers, they’re usually not big enough to make a meaningful impact on an agent’s income.

Some carriers occasionally offer bonuses or overrides for high sales volume, but these are based on overall production — not on pushing one specific plan over another.

What actually motivates GOOD agents?

Client retention- Recommending a poor-fitting plan just to make a slightly higher commission usually backfires when the client is unhappy and leaves.

Referrals- Satisfied clients refer friends and family.

Bottom line, most Medicare agents make similar money regardless of which carrier a client chooses. The real incentive is keeping clients happy and on a plan that actually works well for them, not steering them toward one specific

Because Medicare Advantage and Part D compensation is regulated and often similar across plans, commission differences are usually not the primary reason an agent would recommend one plan over another. Still, compensation arrangements can vary, and CMS has taken steps to address excessive bonuses that could create steering incentives. A good independent broker who represents multiple carriers should recommend the plan that fits your needs. It's always fair to ask which carriers an agent represents and why they're recommending a specific plan.

Note on Medigap: Medicare Supplement (Medigap) plans are sold by private insurers and regulated differently than Medicare Advantage and Part D. Plan letters are standardized, but premiums vary by company, location, and pricing method. Agent commissions for Medigap are set by individual insurers rather than capped by CMS in the same way. The no-fee-to-you principle still applies, but the compensation structure is its own category.

You Pay the Same Premium Whether You Use an Agent or Not

This is the part that surprises most people. The agent's commission is already built into the plan's premium structure. Your plan premium is set by the carrier and approved through the plan's pricing process. An agent should not add a separate enrollment-processing charge on top of that.

Whether you go online and enroll in a Medicare Advantage plan yourself or work with an agent, your premium doesn't change either way. The commission comes from the insurance company's end, not yours.

Do Medicare brokers charge seniors a fee, or is their help free?

Let me clear this up, because there’s a lot of misinformation out there.No—Medicare brokers do NOT charge seniors a fee for their help.

If you sit down with me, call me, text me, ask a hundred questions… you’re not getting a bill. Period.

So how does that work?

We’re paid by the insurance companies, not by you. When you enroll in a plan, the carrier pays the agent a commission that’s already built into the plan. It does not increase your premium, and it’s the same whether you use an agent or go direct.

Now here’s the part people don’t always think about…

If you go online and enroll yourself… or call a 1-800 number…

you’re still paying for that commission—you’re just not getting the guidance that comes with it.

You can do this alone…

or you can have someone walk it with you, answer your questions, fix problems, and make sure you’re actually in the right plan…for the exact same cost.

And I don’t disappear after you enroll.

When something looks off, when a bill doesn’t make sense, when you get one of those “Medicare letters” that makes your head spin… that’s when you call me.

At the end of the day, you’re not paying for a broker…

but you absolutely benefit from having one on your side.

That's what makes the value proposition so clear. You're paying the same amount regardless, but with an agent you get someone who can compare plans across carriers, verify your doctors are in-network, check your prescriptions against formularies, and handle the enrollment paperwork.

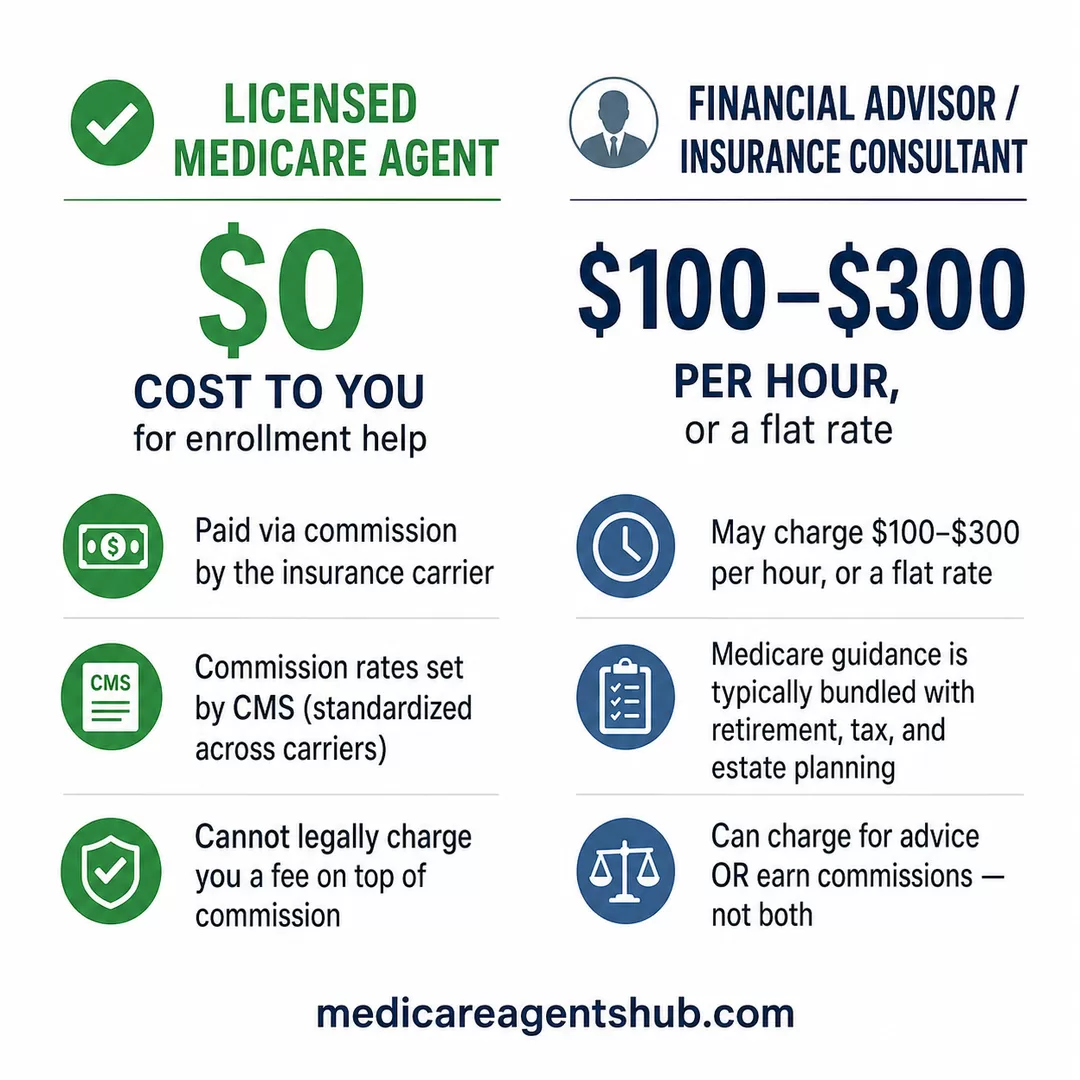

The One Exception: Financial Advisors vs. Licensed Agents

While licensed Medicare agents and brokers do not charge you for enrollment help, there is a related category of professionals who sometimes do charge fees: financial advisors and insurance consultants.

The distinction matters. Licensed Medicare agents earn commissions from insurance companies and cannot charge you on top of that for core enrollment services. Financial advisors, on the other hand, may charge $100 to $300 per hour or a flat rate for comprehensive planning that includes Medicare guidance alongside retirement, tax, and estate planning.

Some financial professionals operate under hybrid compensation models depending on licensing, disclosure requirements, and the type of products involved. If a professional charges a fee and also receives insurance commissions, ask for a clear written explanation of how they are compensated and whether they are acting as an insurance agent, a financial advisor, or both.

How much do agents charge to help clients to enroll

Medicare agents or brokers do not charge the clients a fee for reviewing your options or helping you enroll. Financial advisors or consultants typically charge $100-300/hr or a flat rate fee. Be sure to reach out to a Medicare agent as we're paid by the carriers or programs!If someone asks you to pay for help choosing a Medicare plan, ask whether they're a licensed insurance agent or a financial advisor. A licensed agent working on commission-based plans should not be charging you an additional fee. If you're unsure about someone's credentials, our guide to spotting red flags in Medicare brokers covers what to watch for.

Questions to Ask Before You Trust the Advice

Working with an agent is free, but free doesn't mean you should skip your own due diligence. Before enrolling through any agent or broker, ask these questions:

- Which insurance companies do you represent? Not all agents carry every plan in your area.

- Are you captive or independent? Captive agents represent one carrier. Independent brokers can shop across multiple companies on your behalf.

- How are you compensated? This should be a straightforward answer about commissions paid by carriers.

- Why do you recommend this plan over the alternatives? A good agent should be able to explain their reasoning based on your doctors, prescriptions, and budget.

- Can I compare this against Medicare Plan Finder or my local SHIP counselor? Any agent worth working with will encourage you to verify their recommendation.

These questions protect you and also help you identify agents who are transparent and working in your interest.

Free Help Is Still Worth Using Carefully

Given that working with an agent costs you nothing extra, agent help is a resource worth considering, especially when Medicare has dozens of plan options in most areas. Between Medicare Advantage, Medigap supplements, and standalone Part D drug plans, the combinations add up fast. An agent who works in your local market knows which plans have the strongest provider networks in your area, which carriers have a track record of stability, and which plan features actually matter for your situation.

Do I have to pay extra to use a local Medicare Licensed Insurance agent?

No—you don’t pay anything extra to work with a local Medicare agent.The insurance companies pay agents, whether you go through an agent or enroll directly yourself. So you’re getting guidance, help comparing plans, and ongoing support at no additional cost.

That’s why I always tell people—take advantage of it. It’s a lot easier to have someone walk you through your options and be there if questions come up later.

If you choose to work with an agent, look for someone licensed in your state, transparent about compensation, and willing to explain which plans they can and cannot show you. You can search our directory to find licensed agents near you. Every agent listed represents multiple carriers, so you'll get guidance focused on your needs rather than a single company's products.

Related Questions from Seniors

These are some of the most common questions Medicare beneficiaries ask about working with agents. You can read answers from dozens of licensed agents on each one: