What Medicare Advantage Agents Do and How to Find One

-

December 8, 2025

If you're shopping for a Medicare Advantage plan, the difference between picking the right one and getting stuck with the wrong one often comes down to a single thing: who helped you choose it. A strong Medicare Advantage agent will check your doctors, your drugs, and your hospitals before you enroll, not after. A less thorough one will steer you toward whichever plan is easiest to sell and leave the surprises for January.

This article is written for people comparing Medicare Advantage plans for the first time (or helping a parent compare them), and for anyone who wants to understand what a good agent should actually be doing for them.

Below we cover what a Medicare Advantage agent actually does, how they get paid, the difference between independent and captive agents, and how to find one near you who's worth your time.

What Is a Medicare Advantage Agent?

A Medicare Advantage agent is a licensed insurance professional who specializes in Medicare Part C: the private plans that bundle Parts A, B, and usually D into a single policy, often with extras like dental, vision, and fitness benefits.

Technically, most Medicare Advantage agents are also brokers (there's a lot of overlap in how the terms get used). If you want the full breakdown, we cover the difference between a Medicare broker and a Medicare agent in a separate article. For a broader look at what a Medicare sales agent actually does across all plan types, that guide covers the full scope. For your purposes here, the key thing to know is this: the person helping you is licensed, regulated under CMS marketing rules, and, if they're independent, they can typically offer plans from multiple carriers, not just one.

How They Get Paid

You don't pay a Medicare Advantage agent directly. They're paid a commission by the insurance carrier when you enroll. CMS sets maximum commission amounts that apply broadly across carriers, which is specifically designed to reduce the financial incentive to push one plan over another. Commissions can vary slightly by plan type and situation, but within the same product category they're generally in line with one another.

The practical takeaway: using an agent doesn't cost you anything out of pocket, and in most cases there's little downside to having one in your corner.

Why Use an Agent for a Medicare Advantage Plan Specifically?

Medicare Advantage is a different animal from Original Medicare or a Medigap supplement. It has provider networks, prior-authorization rules, plan-specific drug formularies, and real trade-offs that don't show up in the ads. Comparing three MA plans side-by-side on a carrier's website is how people end up discovering their cardiologist is out of network, in January, after they've already enrolled.

A Medicare Advantage agent catches those problems before you sign anything. That's the whole job.

What benefits are there to working with a Medicare Agent near me vs remote/virtual?

It all comes down to the level of comfortability you have. Many people prefer having a local agent they can speak to and see for all of their questions and concerns about Medicare. Also, that agent will more than likely reach out to you yearly with any plan updates or changes for the next plan year. Not that there is anything wrong with a virtual agent but many times they may not know the local area and how plans work near you with the local physicians and pharmacies. This can be especially true when it comes to Medicare Advantage plans. When it comes to agents in general I would recommend finding a broker, no matter if that is a local or virtual agent, to assist you because they will be able to compare plans across multiple carriers. When you contact a specific carrier they will only be able to compare the specific plans they offer and you may miss out on a better plan.What a Good Medicare Advantage Agent Actually Does for You

The enrollment part takes about 20 minutes. The real value is everything that happens before that.

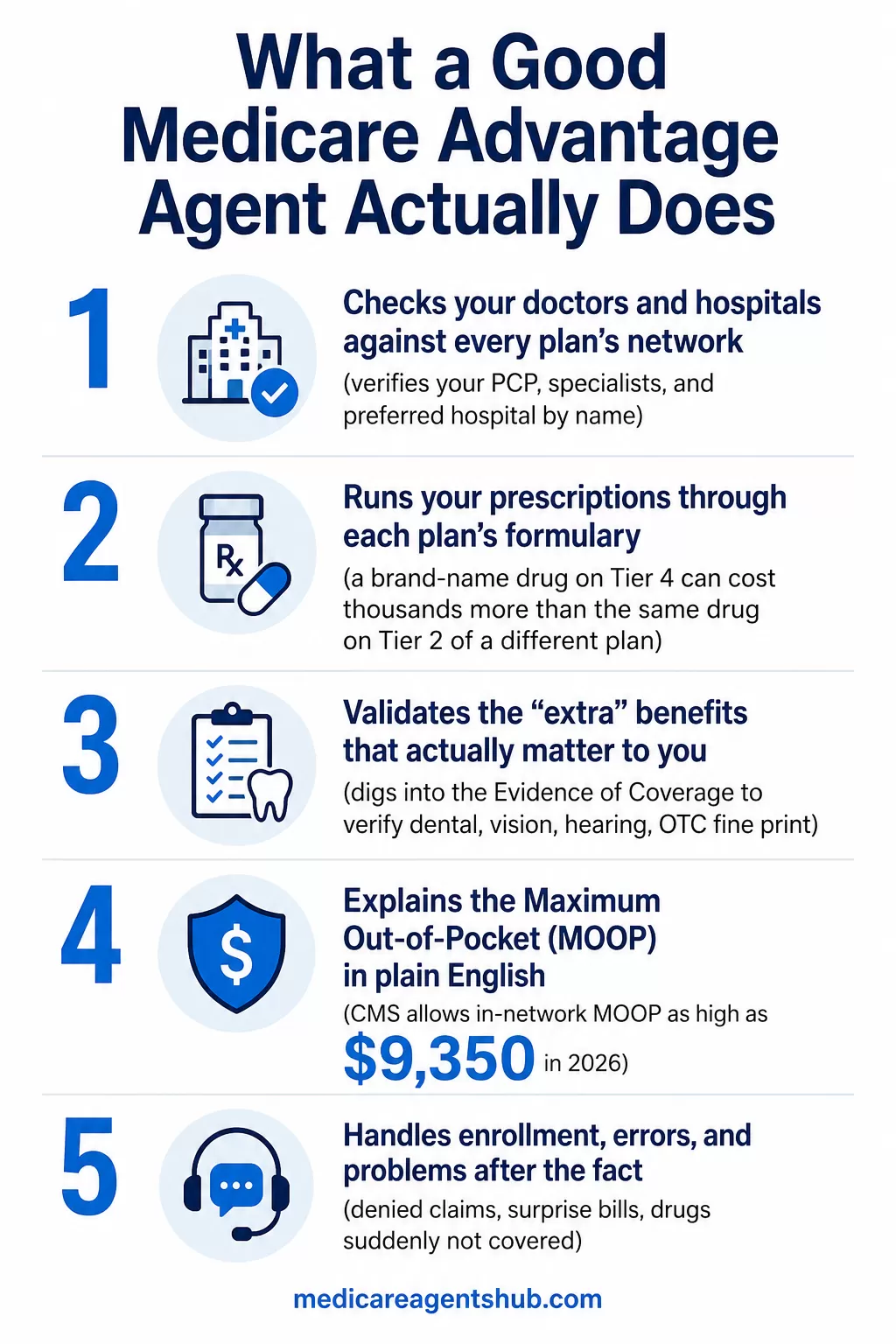

1. Checks your doctors and hospitals against every plan's network

This is the single biggest thing a good agent does. Every MA plan has its own network. Your doctor might be in-network on Plan A, out-of-network on Plan B, and not accepting new Medicare Advantage patients at all on Plan C. An agent pulls up each plan's provider directory and verifies, by name, that your primary care physician, your specialists, and your preferred hospital system are all covered.

2. Runs your prescriptions through each plan's formulary

Two MA plans with identical premiums can have wildly different drug costs. The agent enters your medications into each plan's formulary tool and compares annual out-of-pocket costs. A brand-name drug on a Tier 4 specialty tier can cost thousands more per year than the same drug on Tier 2 of a different plan.

3. Validates the "extra" benefits that actually matter to you

The dental, vision, hearing, and OTC benefits on MA plans are real, but the fine print varies a lot. A $2,500 dental allowance might only cover preventive care. A "fitness benefit" might only work at specific gym chains. A good agent digs into the Evidence of Coverage document and tells you what's actually covered, not just what the commercial promised.

How can I verify if a Medicare Advantage plan's advertised benefits are legit?

Start by going directly to Medicare.gov and using their plan finder tool to look up the specific plan. Everything a Medicare Advantage plan offers has to be filed with CMS, so the official details will be there including premiums, copays, drug coverage, and extra benefits. Compare what you see on Medicare.gov with what the plan is advertising. You can also request the plan's Summary of Benefits and Evidence of Coverage documents, which spell out exactly what's covered and what's not. If something sounds too good to be true, like free groceries or extensive dental with no catches, dig into the fine print because those benefits often have limits, eligibility requirements, or only apply in certain situations. And if an agent is pushing a plan hard without answering your questions directly, that's a red flag. You can also call 1-800-MEDICARE to ask about a specific plan or report misleading advertising.4. Explains the Maximum Out-of-Pocket (MOOP) in plain English

Every MA plan has a cap on what you'll pay for covered medical services in a year. For 2026, CMS allows Medicare Advantage plans to set their in-network MOOP as high as $9,350 (and many plans set theirs well below that). A lot of people see "zero premium" and don't realize there's a potential five-figure ceiling if they get seriously sick. Your agent should walk you through what your worst-case year looks like on each plan you're considering. (Check the plan's current Summary of Benefits or Evidence of Coverage for the exact figure.)

5. Handles enrollment, errors, and problems after the fact

Once you're enrolled, the agent is still your point of contact. Denied claim? Surprise bill? Drug suddenly not covered? A good agent chases it down for you; because their commission stays tied to your policy, they have a direct reason to keep you happy.

Medicare Advantage vs. Medigap: The Conversation Your Agent Should Start With

Before an agent shows you specific Medicare Advantage plans, they should walk you through the bigger choice: Medicare Advantage vs. Medicare Supplement (Medigap). These are fundamentally different approaches to Medicare coverage, and the right pick depends on your health, your budget, how often you travel, and whether you value flexibility or predictable costs.

If an agent jumps straight to Medicare Advantage without even asking about Medigap, that's a reasonable prompt to ask why.

What's your go-to strategy for helping someone decide between Medicare Advantage and Medigap?

Don’t choose based on the premium—choose based on how you want to access care.Medicare Advantage often looks attractive because of low or $0 premiums, but it typically comes with networks, referrals, and prior authorizations. Original Medicare with a supplement costs more monthly, but gives you maximum flexibility—no networks, fewer restrictions, and predictable out-of-pocket costs.

So the real question is:

Do you want freedom to see any doctor nationwide without referrals? → Lean Original Medicare + Medigap

Or are you comfortable with a managed network to save on monthly premiums? → Medicare Advantage

If someone makes the decision purely on premium, they often regret it when they actually need care.

Independent vs. Captive Medicare Advantage Agents

Not all Medicare Advantage agents have access to the same plans. Both types can be knowledgeable and ethical; the difference is how wide their menu is.

Independent Agents

Contracted with multiple carriers. Can compare and enroll you in plans from Humana, UnitedHealthcare, Aetna, Wellcare, Blue Cross, Cigna, and others, whichever fits your situation best. Best when you want an open comparison across the whole market.

Captive Agents

Employed by (or exclusively contracted with) a single carrier. They can only sell that carrier's plans, but they often know those plans in deep detail: networks, formularies, local quirks. A good fit if you've already decided which carrier you want or if that carrier clearly dominates your area.

For most people who are still comparing, an independent agent is usually the better starting point because they can look at the whole field. If you later find out the best plan for you is the same one a captive agent would have sold you, that's a perfectly good outcome; you'll just know you got there on purpose.

How to Find a Medicare Advantage Agent Near You

There are a few legitimate ways to find one, and a lot of sketchy ones. Here's what works:

- Use a licensed agent directory. Directories like Medicare Agents Hub let you search by ZIP code, see the agent's licensing info, read their bio, and reach out directly, with no call centers in between.

- Ask your doctor's office. Billing managers at local practices often know which agents genuinely understand the local plan landscape.

- Ask friends or neighbors on Medicare. Word-of-mouth referrals from people who've been happy for a few years are gold.

- Check your local SHIP office. State Health Insurance Assistance Programs (SHIPs) are free, unbiased counselors funded by the federal government. They don't sell plans, but they can educate you and point you toward reputable local agents.

For more options, see our full guide on how to find a local Medicare agent.

What About Agents Who Work Remotely?

Plenty of great Medicare Advantage agents work entirely over the phone and video. Medicare Advantage plans are county-specific, so your agent doesn't need to live in your city; they just need to know your county's plan options. A remote agent who specializes in Medicare Advantage often sees more plan variations in a month than a local generalist sees in a year. We cover the trade-offs in detail in our article on local vs. remote Medicare agents.

What to Ask When You Interview a Medicare Advantage Agent

Yes, you should interview them. You're about to hand someone a meaningful amount of influence over your healthcare decisions for the next year. Treat it like hiring.

- "How many Medicare Advantage carriers are you contracted with?" (Independent agents should typically be able to name several.)

- "Will you verify my doctors and prescriptions against each plan before I enroll?" (This is the core work, and the answer should be a confident yes.)

- "How do you get paid?" (Listen for a clear, comfortable explanation of carrier commissions, not a dodge.)

- "What happens if I have a problem with my plan next year?" (You want an agent who'll still answer the phone in March.)

- "Did we talk about Medigap, or did you go straight to Medicare Advantage?" (If they skipped the Medigap conversation entirely, it's fair to ask why.)

What are the red flags I should look for when interviewing agents? I want to make sure I'm not just getting sold to but genuinely advised.

Great question — and a smart approach. Red flags include an agent who pushes one plan immediately without reviewing your doctors, prescriptions, and budget. Be cautious if they focus only on “zero premium” or extra benefits without explaining deductibles, networks, prior authorization, or out-of-pocket maximums. An agent who avoids discussing Medigap vs. Medicare Advantage trade-offs or won’t explain commissions and carrier relationships may not be giving balanced advice. A good advisor should compare options objectively, explain downsides clearly, and encourage you to review plan documents before enrolling.Warning Signs and Scams to Watch For

Medicare Advantage is one of the most heavily marketed insurance products in the country, and not all of that marketing is honest. Be skeptical of:

- TV commercials with celebrities promising "extra benefits you're entitled to." These lead-gen ads often sell your info to call centers whose priorities may not match yours.

- Unsolicited phone calls pressuring you to switch plans. CMS marketing rules generally prohibit agents from cold-calling Medicare beneficiaries to pitch MA or Part D plans without prior permission, so an out-of-the-blue sales call is already a yellow flag.

- Agents who won't tell you which carriers they represent or dodge questions about their contracts.

- "Free groceries" or "free money" pitches. The Flex Card benefit is real on some plans, but the claims in those ads are usually wildly exaggerated, and the benefit is rarely usable the way the commercial implies. We go deeper on this in the truth about "free" Medicare Advantage plans.

- Pressure to enroll on the first call. A legitimate agent will give you time to compare and think.

After Enrollment: What an Agent Should Still Do for You

Your relationship with a Medicare Advantage agent shouldn't end the day you enroll. A good one will:

- Review your plan every year. MA plans change their networks, formularies, and benefits annually. What was the best plan for you this year might be the third-best next year.

- Help you read the Annual Notice of Change (ANOC). This document tells you what's changing on your current plan for the coming year. Most people throw it in a drawer; your agent should walk you through it.

- Step in when there's a billing or coverage dispute. Including helping you talk to your doctor about coverage limits if a procedure gets denied or downgraded.

- Alert you when a new plan becomes available that's meaningfully better than what you have now.

The Bottom Line

Medicare Advantage plans are not interchangeable. The difference between a good one and a poor fit for your situation can cost you thousands of dollars, or your preferred doctor, or months of chasing denied claims. An independent Medicare Advantage agent who knows your local plan landscape is one of the best tools you have for getting this right, and for most people, it costs nothing out of pocket.

Find one you trust, ask them the questions above, and hold them to it. That's the whole playbook. And if you're unsure whether now is the right time to reach out, review these key life events when you should consult a Medicare agent to see if your situation calls for professional guidance.