Missed AEP? What You Can Still Change During Medicare Advantage Open Enrollment

-

February 5, 2026

If you blinked and Annual Enrollment Period came and went, you are not alone. Every year, plenty of people realize after January 1 that their Medicare Advantage plan is not quite what they expected. Maybe your doctor is suddenly out of network, your prescriptions cost more than you planned, or that zero premium plan feels a little less "zero" now that you are using it.

The good news is this: missing AEP does not always mean you are stuck. Medicare Advantage Open Enrollment (often called MA-OEP) exists for exactly this situation. It is a second chance window designed to help people who enrolled in a Medicare Advantage plan but want to make a change once real life kicks in.

If you recently went through AEP and already feel like something is off, you are not the first. Take a look at what to do when you chose the wrong Medicare plan during AEP for more on how that happens and what your options look like.

Let's break down what this period allows, what it does not, and how to use it wisely without creating more headaches down the road.

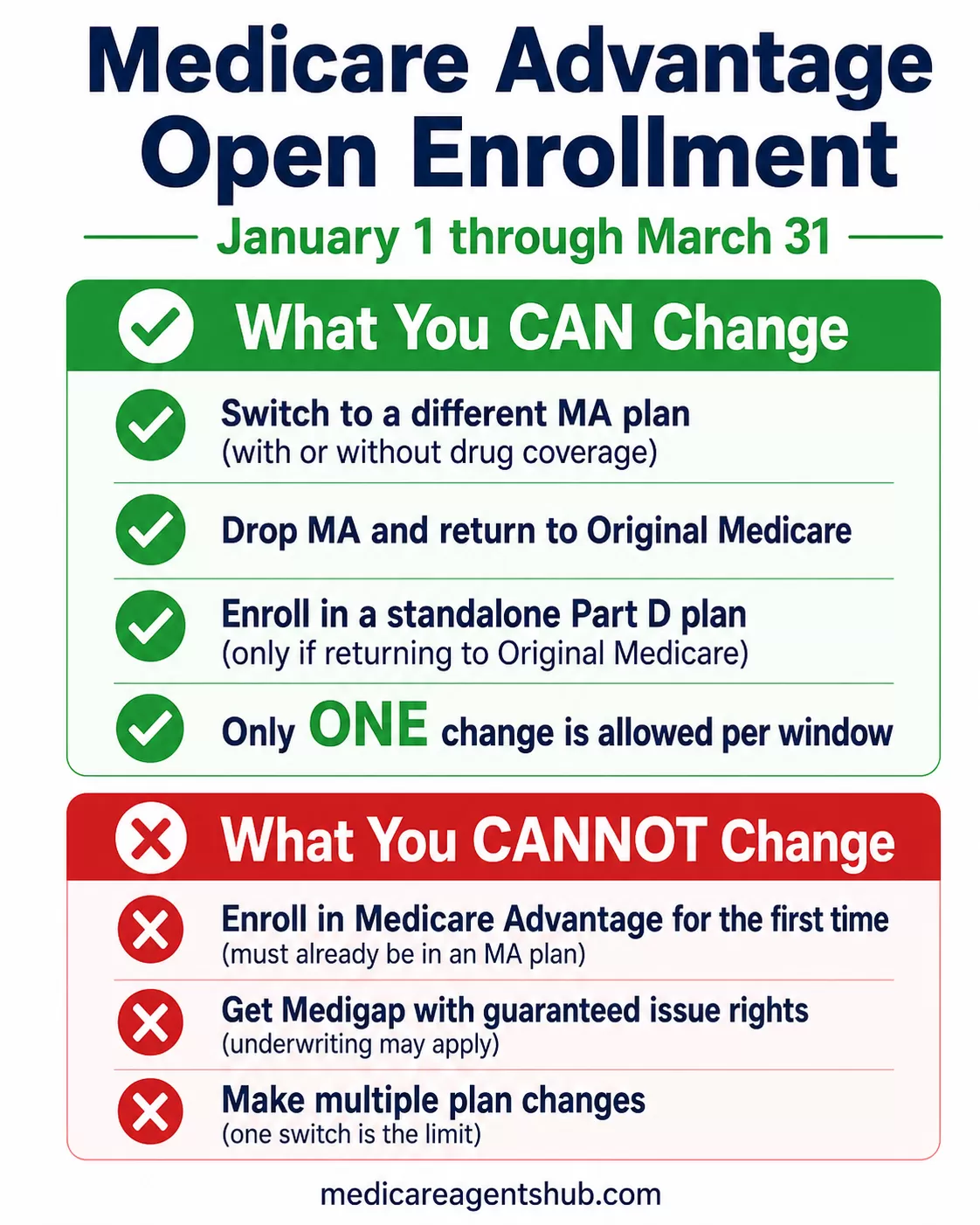

What Medicare Advantage Open Enrollment Is and When It Happens

Medicare Advantage Open Enrollment runs from January 1 through March 31 each year. This window is only available to people who are already enrolled in a Medicare Advantage plan. If you have Original Medicare without a Medicare Advantage plan, this period does not apply to you.

Think of this as a "buyer's remorse" period rather than a full enrollment season. Medicare assumes that once coverage starts, some people will realize the plan is not the right fit. This enrollment window gives you a limited opportunity to correct.

Changes made during this period typically take effect the first day of the month after the plan receives your request, which means timing matters if you want to minimize disruptions.

Medicare Advantage OEP vs AEP: Quick Comparison

People often mix these two windows up, and it costs them options. AEP (Annual Enrollment Period) is the big fall window that runs October 15 through December 7 and is open to everyone on Medicare. MA-OEP is the narrower January 1 through March 31 window, and it is only for people already on a Medicare Advantage plan.

| AEP (Annual Enrollment Period) | MA-OEP (Medicare Advantage Open Enrollment) | |

|---|---|---|

| Dates | October 15 - December 7 | January 1 - March 31 |

| Who it's for | Anyone on Medicare | Only people already in a Medicare Advantage plan |

| How many changes | Unlimited (last one submitted wins) | One change only |

| Can join Medicare Advantage from Original Medicare? | Yes | No |

| Can switch Medicare Advantage plans? | Yes | Yes |

| Can drop MA and return to Original Medicare? | Yes | Yes |

| Can enroll in a standalone Part D plan? | Yes | Only if you drop MA and return to Original Medicare |

The short version: AEP is the wide-open door, MA-OEP is the small side door for people who already made a Medicare Advantage decision and want a redo.

What You Can Change During Medicare Advantage Open Enrollment

Medicare Advantage Open Enrollment is intentionally narrow. You cannot make unlimited changes, but you do have meaningful options if your current plan is not working.

During this period, you are allowed to do the following:

- Switch from one Medicare Advantage plan to another Medicare Advantage plan, with or without drug coverage

- Drop your Medicare Advantage plan and return to Original Medicare

- Enroll in a standalone Part D prescription drug plan if you return to Original Medicare

That's it. You can make one change during this period, so it is important to be thoughtful before submitting anything.

This window is especially helpful for people who discover network issues, unexpected prescription costs, or higher out-of-pocket expenses once they start using their coverage.

I'm confused about when I can change my Medicare plan. Can you clarify the different enrollment periods for me?

Here are the enrollment periods:1. Initial Enrollment (IEP): 7 months around your 65th birthday to join Part A & B.

2. Annual Election (AEP): Oct 15–Dec 7 to join, switch, or drop Advantage or Part D plans.

3. Medicare Advantage Open Enrollment (MA OEP): Jan 1–Mar 31 to change Advantage plans or return to Original Medicare.

4. Special Enrollment (SEP): For life events like moving or losing coverage.

5. Medigap Open Enrollment: 6 months from Part B start to buy a supplement without medical underwriting.

What You Cannot Change Right Now

Just as important as knowing what you can do is understanding what is off the table. Medicare Advantage Open Enrollment is not a second Annual Enrollment Period.

Here are a few common misunderstandings to clear up:

- You cannot enroll in Medicare Advantage for the first time if you are only on Original Medicare

- You cannot switch or enroll in a Medigap policy with guaranteed issue rights just because you drop Medicare Advantage

- You cannot make multiple plan changes during this window

If you are considering returning to Original Medicare and purchasing a Medigap policy, underwriting may apply depending on your situation. This is one of the most common surprises people run into, so it is worth slowing down and reviewing your options carefully. Medicare.gov has a helpful overview of when you can buy Medigap that spells out the guaranteed issue scenarios. For a deeper look at the trade-offs that come with Medicare Advantage, that context can help frame whether leaving makes sense for you.

Can I switch from a Medicare Advantage plan to a Supplemental/Medigap plan during the Annual Enrollment Period without answering health questions?

It is important that you chose the right plan for you when you are originally going into Medicare. You can chose a Supplement or a MAPD plan and you are not underwritten at that time. During AEP you would need to first return to original Medicare then you would apply and be underwritten. This will always be the case once you chose an MA over a Supp. If you chose a Supp at the time you get your Medicare, some states have birthday rules which allows you to change around your birthday without be underwritten. Speak to an agent before turning 65 to find out all options in your state.Common Reasons People Use This Enrollment Period

Most people who take action during Medicare Advantage Open Enrollment fall into one of a few categories. These are not mistakes as much as lessons learned after coverage starts.

Some of the most common triggers include:

- A preferred doctor or hospital is not in network

- Prescription drug costs are higher than expected

- Referrals and prior authorizations feel more restrictive than anticipated

- Out-of-pocket costs add up quickly for frequent care

- The plan's service area or provider access feels too limited

None of these issues make a plan "bad." They simply mean it may not be the right fit for your health needs and lifestyle.

Should You Switch Plans or Go Back to Original Medicare?

This is where things become personal. There is no universally correct move during Medicare Advantage Open Enrollment. The right decision depends on your health, finances, and tolerance for managed care.

Switching to another Medicare Advantage plan may make sense if your primary issue is network access, drug coverage, or benefits like dental or vision. Many people simply choose a plan that better aligns with how they actually use healthcare.

Returning to Original Medicare can make sense if flexibility is your top priority. Original Medicare allows you to see any provider who accepts Medicare nationwide, which appeals to people who travel or want fewer restrictions.

Before making this decision, it helps to think about how often you use healthcare services, whether predictable costs matter more than flexibility, and if you are comfortable navigating referrals and authorizations.

Is Original Medicare or Medicare Advantage better? Why do you recommend one over the other?

It truly varies by the individual person's needs as well as their geograhic location.Original Medicare provides more freedom to choose from any provider who accepts Medicare nationwide which is about 99% of them, but Medicare Advantage plans will have a limited network of providers to choose from and often require referrals, etc.

Mistakes to Avoid Before Switching During OEP

Since you are only allowed one change during Medicare Advantage Open Enrollment, it is worth taking a little extra time before you submit anything. A quick review now can help you avoid trading one frustration for another later in the year.

Start by confirming that your doctors, specialists, and preferred hospitals are in the plan's network. Provider access is one of the most common reasons people switch plans, and it is much easier to check this upfront than to find out after appointments are scheduled.

Next, review your prescription medications carefully against the plan's drug list to see how they are covered and what your costs will be at the pharmacy.

It is also smart to look beyond the monthly premium and focus on the plan's maximum out-of-pocket limit. This number plays a major role in what you could spend during a year when healthcare needs increase.

Finally, take a moment to understand how referrals and prior authorizations work under the plan. Knowing what is required before seeing specialists or receiving certain services can help set realistic expectations and prevent delays in care.

A few extra minutes of review can make a meaningful difference in how satisfied you feel with your coverage for the rest of the year. For a full checklist of what to look at, see our guide on what to review on your Medicare plan at the start of the year.

Can you help me understand Maximum Out-of-Pocket (MOOP) limits in Medicare plans, from your experience as an agent?

In simplified terms MOOP or Max Out of Pocket cost is the most you will have to pay for COVERED healthcare services in a year under your Medicare plan. This means as your copays, coinsurance and deductibles are paid throughout the year, and they meet the MOOP amount, you will not pay out of pocket anymore throughout the year.For example, if your Medicare Advantage plan has a MOOP of 5,000.00 and you hit that amount in medical costs Copays, Coinsurance and deductibles, during the year, you will not pay anything more for covered services the rest of the year.

What if You Missed OEP Too?

If March 31 has already come and gone and you never made a move, your options narrow, but they are not gone. Outside of AEP and MA-OEP, changes to Medicare Advantage generally require a Special Enrollment Period (SEP). SEPs are triggered by specific life events like moving out of your plan's service area, losing employer coverage, qualifying for Medicaid or Extra Help, or your plan losing its Medicare contract.

If none of those apply, you will typically need to wait until the next AEP (October 15 - December 7) to make a change that takes effect the following January 1. In the meantime, it is still worth reviewing your plan's summary of benefits so you know what to expect for the rest of the year and can plan ahead for AEP.

Making Your Changes

Missing Annual Enrollment Period does not mean you are stuck with a Medicare Advantage plan that is not working for you. Medicare Advantage Open Enrollment exists to give you a limited but meaningful opportunity to make a change once coverage becomes real.

That said, this is not a window for casual experimenting. One well-informed decision now can save you months of inconvenience and unexpected costs.

If your current plan feels off, trust that instinct. Just be sure your next move is based on how you actually use healthcare, not how the plan looked on paper back in the fall.

Making the right adjustment now can set you up for a far smoother year ahead.

You do not have to sort this out alone. A local licensed Medicare agent can help you compare your options and make sure your next plan actually fits how you use healthcare. If you would rather start with free, unbiased guidance, your State Health Insurance Assistance Program (SHIP) counselor is another good place to turn.