Medicare Advantage MOOP: What Doesn't Count Toward Your Out-of-Pocket Max

-

March 2, 2026

You picked a Medicare Advantage plan with a $3,000 max out-of-pocket. You figure once you spend $3,000 on medical care, the plan picks up everything for the rest of the year. That's technically true for a narrow slice of your healthcare spending. But four entire categories of costs never touch that number, and they're the ones most likely to catch you off guard.

We asked 34 licensed Medicare agents to explain how the MOOP actually works. Their answers revealed a consistent gap between what beneficiaries assume and what the cap really protects.

2026 Medicare figures in this article are based on CMS and Medicare.gov guidance, including the 2026 Part D out-of-pocket cap and standard Part B premium.

| Cost Type | Counts Toward MOOP? |

|---|---|

| Doctor/specialist copays for covered in-network Part A & Part B services | Yes |

| Part D prescription drugs | No (separate cap) |

| Dental, vision, and hearing extras | No |

| Monthly plan premiums | No |

| Part B premium / IRMAA surcharges | No |

| Out-of-network care | Usually no (or separate limit) |

How the MOOP Actually Works: The Reverse Checking Account

Before getting into what's excluded, it helps to understand how the cap adds up in the first place. Multiple agents described it the same way, but one analogy came up repeatedly: a reverse checking account.

With a Medicare Advantage plan after I reach the max out of pocket, $3,000 or more, will I have any copays or fees the rest of the year?

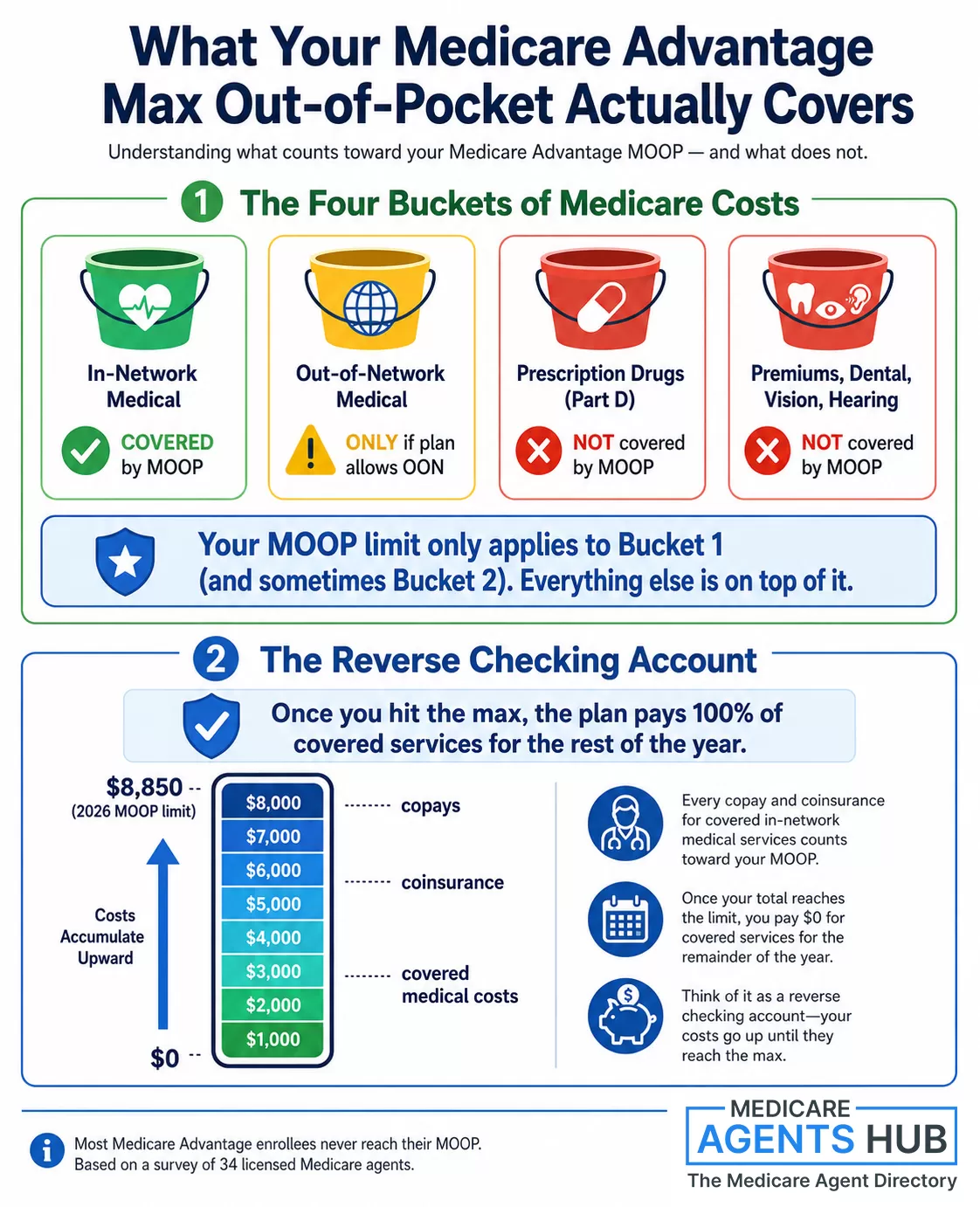

This is a great question and one that I think can be misunderstood. Most plans have different Out of Pocket Maximum values. I always explain it like a reverse Checking Account - You start with, let's use the example of $3,000 and every time you pay a Deductible-Coinsurance-Copay it gets deducted from the $3,000 (MOOP) Maximum Out Of Pocket. If you ever reach that Dollar Amount the Health Insurance Company pays remaining charges for the remainder of that Calendar Year. Remember, Medicare Advantage Plans work on a Calendar Year - January 1st to December 31st.That's the framework. You start the year with a balance equal to your plan's MOOP. Every deductible payment, every copay, every coinsurance charge for Part A and Part B services gets subtracted from that balance. When the balance hits zero, the plan covers 100% of those services through December 31. Then it resets on January 1.

What makes this confusing is the phrase "out-of-pocket maximum" itself. It sounds like a cap on everything you could possibly spend on healthcare. It isn't. It's a cap on a specific subset of costs, and the rest are on a completely separate track.

The Four Buckets That Don't Count

Across 34 agent responses, four categories came up over and over as exclusions. These are costs you will continue paying even after hitting your MOOP.

1. Part D Prescription Drugs

This is the biggest source of confusion. Most Medicare Advantage plans include Part D drug coverage bundled into the same plan. Same insurance card, same monthly bill. So beneficiaries naturally assume their drug costs count toward their out-of-pocket max. They don't.

Part D has its own completely separate spending limit. In 2026, the Part D out-of-pocket cap is $2,100. Once you spend $2,100 on covered drugs at the pharmacy, the plan pays the rest for the remainder of the year. But that $2,100 and your medical MOOP are two independent clocks running side by side.

Agent Rebecca Bilbrey in Waxahachie, TX put it plainly: "The max out-of-pocket for a Part D drug plan in 2026 is $2,100; after which you pay $0 for your covered Part D drugs for the remainder of the year." Meanwhile, agent Grant Evans in Zelienople, PA emphasized the separation: "Your medical out of pocket cost is separate from your prescription out of pocket cost."

One exception worth noting: A small number of Medicare Advantage plans use a combined medical and drug MOOP, meaning your Part D spending and medical spending draw from the same pool. This is rare, but if your plan has one, the math changes significantly. Check your Summary of Benefits or ask your agent whether your plan uses separate or combined limits.

2. Dental, Vision, and Hearing

Many Medicare Advantage plans advertise dental, vision, and hearing benefits as extras. And they are extras, in the truest sense. These benefits sit outside the standard Medicare Part A and Part B framework, which means the copays, coinsurance, and other costs you pay for dental cleanings, eye exams, glasses, hearing aids, and hearing tests don't count toward your MOOP.

With a Medicare Advantage plan after I reach the max out of pocket, $3,000 or more, will I have any copays or fees the rest of the year?

The Medicare Advantage plans cover the Part A and Part B of Medicare expenses. So, although you mostly won't have any concerns about paying more out of pocket above that, you will still have to pay for your Part D prescriptions, any dental or vision, gym costs, etc. If you have any needs that take you Out of Network, you will be responsible for those costs as well.This matters because the dental/vision/hearing benefits on MA plans often come with their own limits: a $1,000 annual dental allowance, for example, or a $200 cap on eyewear. Once you exceed those limits, you're paying full price out of pocket, and none of it moves the MOOP needle.

Agent Maureen Wark in Lexington, MI confirmed: "Prescriptions, dental, vision, hearing benefits do not apply to that maximum."

3. Monthly Premiums

This one catches fewer people off guard, but it still trips up some. If your Medicare Advantage plan has a monthly premium (and many do, especially PPOs or plans with richer benefits), those premium payments never count toward your MOOP. You could hit your $3,000 cap in March after a hospital stay, but you still owe your monthly premium every month through December.

The same applies to your Part B premium ($202.90/month for most people in 2026) and any IRMAA surcharges on top of that. None of it counts.

Agent Nancy Courser in Canadian Lakes, MI was one of the few who explicitly flagged this: "If you have a monthly premium, you are still responsible for paying the monthly premium through the rest of the year."

4. Out-of-Network Charges

If you have an HMO-type Medicare Advantage plan, out-of-network services generally aren't covered at all (except in emergencies). You're paying 100% out of pocket, and zero of it goes toward your MOOP.

PPO plans do offer some out-of-network coverage, but the rules vary by plan. Some plans have a separate out-of-network MOOP that's much higher than the in-network one. Others don't. Agent Heidi Wotton in New Harbor, ME put it simply: "Just make sure the services are in-network and medically covered by the plan."

This creates a real trap for snowbirds and travelers. If you spend winters in a different state and see providers outside your plan's network, those bills are piling up on a separate ledger that your MOOP can't touch.

Not sure what your plan's MOOP covers? A local Medicare agent can walk through your specific plan's cost-sharing, identify what counts and what doesn't, and help you compare options during enrollment.

Find a Medicare Agent in Your Area

Prefer non-commercial help? Call 1-800-MEDICARE or contact your local State Health Insurance Assistance Program (SHIP) for free, unbiased counseling.

The National MOOP Ceiling vs. What Plans Actually Charge

CMS sets a national maximum for how high a plan's in-network MOOP can be. That number changes by year, so always verify the current year's limit when comparing plans. But most plans set their actual MOOP well below the national ceiling.

When you shop during AEP, you'll see in-network MOOPs ranging from around $3,000 to $5,000 on competitive plans, with some going higher in areas with fewer options. The national ceiling exists as a consumer protection backstop, not a target.

If your plan's MOOP is near that ceiling, it's worth asking your agent whether there are better options in your area.

"I've Been Doing This 20 Years and I've Seen It Hit Once"

Here's the part that surprises people the most. For all the anxiety about hitting the max out-of-pocket, most Medicare Advantage enrollees never get close.

With a Medicare Advantage plan after I reach the max out of pocket, $3,000 or more, will I have any copays or fees the rest of the year?

So the short answer to that is no, they will not have any more co-pays. But I'll tell you something, I've been doing this for 20 years and I've seen one time where somebody met their yearly max. I mean, it could happen, but it's pretty rare because the way the Advantage plans are set up, it's a co-pay based model. It's a pay-as-you-go model.

So when you go into the hospital, there's a co-pay depending on how many days you stay. If you need an ambulance, there's a co-pay for that, and for the doctor visit, there's a co-pay too. But the co-pays are pretty low. So to reach a $3,000 or $4,000 yearly maximum, it's pretty hard to do. I mean, you have to have services and issues the entire year to even get close to that.

But to answer the question that the person's posing, once you reach that maximum, that's it. That's the ceiling for in-network benefits.

Steve Brauer's observation lines up with how these plans are structured. Medicare Advantage uses a copay-based model. A doctor visit might cost you $20. A specialist, $40. Even a hospital admission typically runs a flat daily copay rather than a percentage of the total bill. To accumulate $3,000 or more in copays and coinsurance in a single calendar year, you'd need sustained, repeated use of high-cost services.

That doesn't mean it can't happen. A serious diagnosis involving surgery, extended hospital stays, outpatient rehab, and multiple specialist visits can push costs up fast. But for the average beneficiary, the MOOP functions more as a safety net you're unlikely to need than a spending threshold you'll brush up against every year.

This is also why the cost comparison between Medicare Advantage and Medigap is more nuanced than just looking at premiums. Medigap plans charge higher premiums but eliminate most cost-sharing. MA plans charge lower premiums but expose you to copays, and those copays are what fill the MOOP bucket.

Hospital Indemnity: The Gap-Filler Agents Keep Recommending

One theme came up repeatedly in the agent answers, unprompted: hospital indemnity insurance. This isn't a Medicare product. It's a supplemental policy that pays a flat cash amount per day (or per admission) when you're hospitalized. The payment goes directly to you, not to the hospital, so you can use it however you want.

With a Medicare Advantage plan after I reach the max out of pocket, $3,000 or more, will I have any copays or fees the rest of the year?

You will always have copays for specialist and primary care if your plan has those copays as well as copays for many out patient procedures.I recommend purchasing a hospital indemnity plan to help off set those hospital copays. These plans are very reasonable in cost.

Why do agents keep recommending this alongside Medicare Advantage? Because of the copay structure. An MA plan might charge $300-$400 per day for hospital stays (with daily copay amounts varying by plan and by how many days you're admitted). A hospital indemnity plan that pays $200 or $300 per day can offset most of that, and the policies typically cost $30-$60 per month.

One thing to keep in mind: hospital indemnity plans are not regulated as Medicare supplements. They're separate fixed-benefit policies, so coverage amounts, payout triggers, and exclusions vary widely between carriers. Always compare plans carefully before buying.

The catch: hospital indemnity premiums don't count toward your MOOP either. And the plan only pays for hospital stays, not outpatient visits or specialist copays. But for the specific scenario that's most likely to push someone toward their MOOP, a multi-day hospitalization, it's a meaningful buffer.

What to Actually Check on Your Plan

Your plan's Summary of Benefits document lists the MOOP amount, and it also spells out (usually in the fine print) what counts and what doesn't. Here's a quick checklist for reviewing your own plan:

- Find your in-network MOOP. This is the number that matters. If your plan also lists an out-of-network MOOP, note how much higher it is.

- Check whether your plan has a separate drug deductible. The Part D $2,100 cap is universal in 2026, but some plans also have a drug deductible (up to $590) before your copays even kick in.

- Look at your dental, vision, and hearing benefit limits. These are separate from MOOP. A plan might offer $2,000 in dental coverage, but once you use it, additional dental work is 100% on you.

- Ask about prior authorization. Agent Mark Christiansen in Mequon, WI pointed out something often overlooked: "Be sure to get prior authorizations from your Advantage plan before taking on anything out of the ordinary such as CT scans, MRI's, surgeries, infusions." Without prior auth, a service that would normally count toward your MOOP might not be covered at all.

- Know when the clock resets. Every MOOP is a calendar-year number. A $2,800 surgery on December 15 doesn't carry over. You start from zero on January 1.

If how Medicare copays work still feels unclear after reviewing your Summary of Benefits, that's a good reason to sit down with a local Medicare agent who can walk through your specific plan's cost-sharing structure.

The Bottom Line From 34 Agents

The MOOP on your Medicare Advantage plan is real protection. Once you hit it, your plan does pay 100% for covered, in-network medical services. But that protection is narrower than most people realize. Prescription drugs, dental work, vision care, hearing services, monthly premiums, and out-of-network charges all live outside the cap. And according to at least one agent with two decades of experience, most people never hit the cap in the first place.

The takeaway isn't that the MOOP is useless. It's that treating it as a ceiling on all healthcare costs for the year leads to surprise bills in categories you assumed were included. Knowing which costs are on which track is the difference between a plan that protects you and a plan that surprises you.

Frequently Asked Questions

Do prescription drugs count toward Medicare Advantage MOOP?

No. Part D drug costs have their own separate out-of-pocket cap ($2,100 in 2026). What you spend at the pharmacy does not reduce your medical MOOP balance.

Do dental, vision, and hearing costs count toward MOOP?

Usually no. These benefits are generally classified as supplemental and sit outside the standard Part A and Part B cost-sharing that feeds the MOOP.

Do Medicare Advantage premiums count toward MOOP?

No. Monthly premiums, including your Part B premium and any IRMAA surcharges, do not count toward the max out-of-pocket.

What happens after I hit my Medicare Advantage MOOP?

The plan pays 100% of covered, in-network Part A and Part B medical services for the rest of the calendar year. You still pay premiums, Part D costs, and any dental/vision/hearing charges separately.

Does the MOOP reset every year?

Yes. Medicare Advantage MOOPs reset each calendar year on January 1. Any spending from the previous year does not carry over.