The Medicare Donut Hole Is Gone: What Actually Happens Now When Your Drug Costs Climb

-

April 11, 2026

If you're still bracing for the donut hole every year, you can stop. The Medicare Part D coverage gap was eliminated in 2025 under the Inflation Reduction Act, and it's not coming back. What replaced it is simpler and far more protective: a hard annual cap on what you'll spend out of pocket for covered prescription drugs. In 2026, that cap is $2,100.

But "simpler" doesn't mean there's nothing to understand. The new system has its own quirks, and agents across the country are fielding questions from clients who still think the old rules apply. This article breaks down what actually happens now when your drug costs climb.

What the Donut Hole Was (and Why It's Gone)

The donut hole was a coverage gap built into Medicare Part D from the program's creation in 2006. After you and your plan spent a combined amount on drugs (the "initial coverage limit"), you entered a phase where you paid a much larger share of costs, sometimes 25% or more for both generics and brand-name medications. This continued until your out-of-pocket spending hit a catastrophic threshold, at which point near-full coverage kicked back in.

For people on expensive medications, the old structure could still mean thousands of dollars in annual drug costs, especially before the newer out-of-pocket protections took effect.

The Affordable Care Act began shrinking the donut hole over a decade, and the Inflation Reduction Act finished the job. As of January 1, 2025, the coverage gap phase no longer exists in any Part D plan.

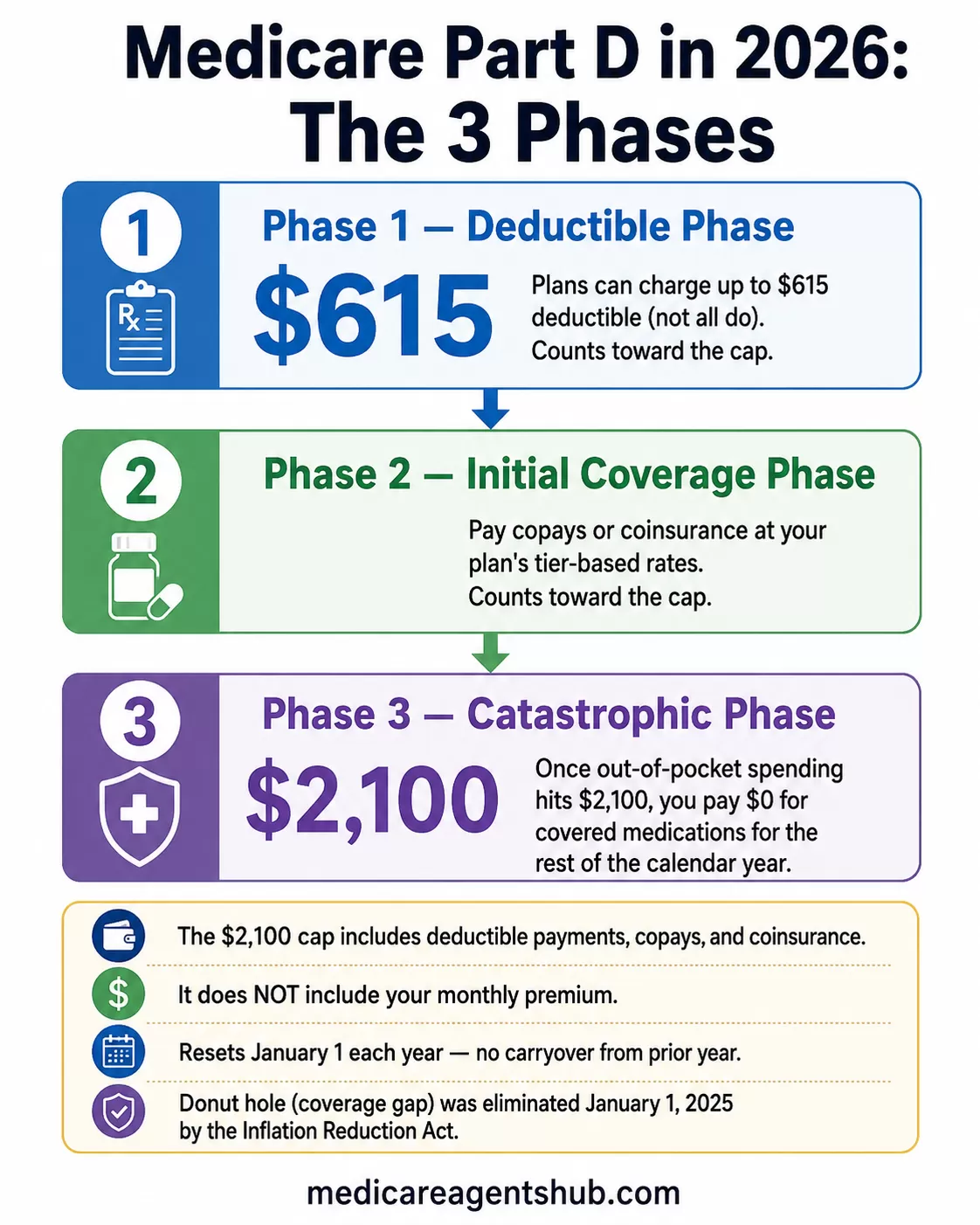

How the $2,100 Out-of-Pocket Cap Works

The new structure is straightforward. In 2026, there are three phases of Part D coverage instead of four:

- Deductible phase: Plans can charge up to a $615 deductible (not all do). What you pay here counts toward your cap.

- Initial coverage phase: You pay copays or coinsurance for your medications at your plan's tier-based rates. These payments also count toward the cap.

- Catastrophic phase: Once your out-of-pocket spending hits $2,100, you pay $0 for covered medications for the rest of the calendar year.

That $2,100 includes your deductible payments, copays, and coinsurance. It does not include your monthly premium.

My pharmacist mentioned the Medicare "donut hole" is going away in 2025. What does that actually mean for me?

Your pharmacist is referring to changes in Medicare Part D. The “donut hole” (coverage gap) hasn’t exactly disappeared in name, but starting in 2025 it’s been simplified so you no longer face that confusing phase where your costs suddenly changed. Instead, there’s now a $2,100 annual cap on out-of-pocket prescription drug costs, which means once you hit that limit, you won’t pay anything more for covered medications for the rest of the year. In practical terms, this makes your drug costs more predictable and protects you from very high expenses, especially if you take expensive medications.Why January and February Can Still Hit Hard

One surprise that catches people off guard: even though the annual cap is much lower, the first few months of the year can feel expensive. Agents describe this as a "reverse donut hole" because the cost pressure comes at the beginning of the year rather than the middle.

If you take a brand-name specialty drug that costs $800 per fill, you could burn through most of your $2,100 cap in January and February alone. You'll pay nothing after that, but those initial pharmacy bills can be a shock if you're not expecting them.

This front-loading happens because your plan resets on January 1 each year. There's no carryover from the previous year's spending, so everyone starts at $0 and works toward the cap fresh.

I've been dreading hitting the donut hole each year. How will its elimination in 2025 change what I pay throughout the year?

The good news is that you won't be paying more than $2000 for all your covered medications for the year (not including the monthly premium). The bad news is that you might have to pay higher copays at the beginning of the year - almost like a reverse donut hole where you're hitting the donut hole immediately rather than towards the middle or latter end of the year. You do have the option to break up your out-of-pocket drug costs into monthly payments, so it lessens the amount you have to pay initially.The Medicare Prescription Payment Plan (M3P)

CMS introduced the Medicare Prescription Payment Plan specifically to address this front-loading problem. Instead of paying full copays at the pharmacy counter each month, you can opt into a plan that spreads your out-of-pocket drug costs into predictable monthly installments over the remainder of the year.

How it works in practice:

- You can enroll at any time during the plan year by contacting your Part D plan or Medicare Advantage plan directly.

- Your monthly bill is calculated using the Part D costs you would have paid at the pharmacy, plus any remaining balance, spread over the months left in the year. Your bill can change if you fill new prescriptions or refill expensive medications later in the year.

- This payment option can help smooth out cash flow, but it does not lower your total drug costs.

- There is no interest on these payments.

- When you pick up your medications, you pay $0 at the pharmacy. Your monthly bill comes separately.

The M3P is most useful for people on expensive specialty drugs or those who take multiple brand-name medications. If your total annual drug costs are modest (say, a few generic prescriptions totaling $300 for the year), the payment plan doesn't add much value.

I'm in the donut hole and can't afford my medications. What are my options right now before the 2025 changes?

If you're having a challenge paying for your medications you can apply for extra help via the site Medicare.gov. Additionally, you can contact your drug plan carrier and ask for the prescription payment plan options which spreads the medication costs over the course of the year. Another option would be to contact your senior center and ask if they have a prescription coverage program.Formulary Fine Print: The Cap Only Counts for Covered Drugs

This is the piece that trips people up most often. The $2,100 cap applies only to drugs that are on your plan's formulary. If you fill a prescription that isn't covered by your plan (unless your plan approves a formulary exception or provides a transition fill), every dollar you spend on it is invisible to the cap. It doesn't count toward your $2,100, and your plan won't reimburse you.

This matters because formularies change every year. A drug that was covered in 2025 might be dropped or moved to a higher tier in 2026. Some plans have also restructured their formularies in response to the new cap rules, adding Part D deductibles or shifting drugs between tiers.

Before the start of each plan year, check that every medication you take is still on your plan's formulary at an acceptable tier. If something got dropped, that's a strong reason to switch plans during the Annual Enrollment Period.

I'm worried about the 'donut hole' in my Part D plan. How do I manage my medication costs once I enter it?

Hello, the "donut hole" ended in 2025. There is currently a maximum out of pocket, for covered medications, of $ 2100.00. Once you reach that maximum the prescription costs are zero. This will not apply to a drug that is not on the insurance carriers formulary. If it is not on their formulary you will pay the full cost of the drug each time you fill the prescription. This is why you should evaluate your plan yearly, so you know you still have your expenses covered.What You Should Do Now

The donut hole is gone, and for most people, the new system is a significant improvement. But it works best when you're proactive about a few things:

- Verify your formulary. Every medication you take should be on your plan's covered drug list. If it's not, your spending doesn't count toward the cap.

- Price out January. If you take expensive medications, estimate what you'll owe in the first couple months. This helps you decide whether M3P makes sense.

- Review during AEP. Plans change their formularies, tier structures, and premiums every year. A plan that was ideal in 2025 might not be the best fit in 2026.

- Ask about manufacturer patient assistance programs. Some drugmakers still offer discount programs that can reduce your costs further, especially for brand-name medications.

If you're unsure whether your current plan is still the right fit, a licensed Medicare agent can run your medications through multiple plan comparisons and show you exactly what you'd pay under each option.